October 2023

Investment Conditions & Outlook

Executive Summary

The third quarter of 2023 commenced with strength but swiftly recalibrated expectations. Long-term rates surged, which undoubtedly defied projections and challenged the expected yield decline. Many assumed rates would be lower by this point, but economic resiliency remained. Simultaneously, the rapid rise in oil prices, a result of the delicate balance between OPEC supply constraints and escalating demand, underscored the market’s sensitivity to global economic shifts and kept inflation above the Fed’s long term target.

Stocks and bonds traded lower for August and September. Coming off a strong, tech-driven first half of the year, stocks experienced a lesser drawdown relative to other asset classes. A significant factor that aided equities in weathering the rise of long-term rates has been the flat to slightly higher level in earnings expectations. A lot is riding on corporate earnings due to the fact lofty valuations and multiple expansion are unlikely to further buoy markets. As uncertainty lingers, defensive sectors continue to offer attractive opportunities. As we show in the chart below, historically defensive sectors have underperformed the technology heavy sectors. As more evidence builds that the economy is slowing, investors should be less willing to embrace more

volatile stock exposure. This doesn’t imply a worst-case scenario; rather, increased volatility could lead to dispersion in equity returns moving forward. Hence, our focus on companies that provide robust profit margins and upward earnings revisions remains prudent in our approach amid market and economic challenges.

Recent fund flows signal a cautious consensus, with U.S. investors favoring bonds and cash over equities. This shift aligns with markets trading well off their relative highs. As the economy slows, we prefer more stable companies with predictable earnings. Further, favorable yields in cash and short-term government debt support our differentiated position, enabling patient investment opportunity exploration.

Two pressing questions have emerged about the current economic environment. First, while the “higher for longer” rate stance gains acceptance, doubts linger about sustainability of high rates. Corporate interest earnings surpass payments (corporate debt maturities pick up after 2024), but the government is also paying more, seen in the interest payments as a percentage of GDP. This poses concerns and will likely become a political focal point during the upcoming elections.

Second, amidst market negativity and uncertainty, the soft-landing narrative emerges. Can the Fed orchestrate a soft landing without harming the labor market significantly? Contemporaneously declining inflation and cooling labor markets are the Federal Reserve goals, but it remains to be seen if cooling labor markets impact the historically low unemployment rate.

Like the past years and decades, the world is uncertain. Accepting depressed market prices as discounts and compensation for owning equities and bonds in less optimistic times allow investors to formulate a long-term strategy. This acceptance fosters confidence when navigating the turbulent waters of the market. We remain focused on owning assets with low correlation and characteristics we believe will be advantageous looking forward. If the third quarter reaffirmed anything, it is stability that counts when growth slows.

The Janiczek Team

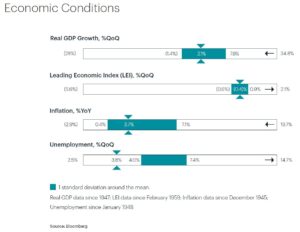

Economic Conditions and Key Takeaways

- Inflation has been falling from post COVID highs, but energy continues to be a wildcard as the price of Brent Crude Oil trades above $90 per barrel.

- Central banks will likely keep policy restrictive for longer than the market anticipates, with one more hike expected this year. The Federal Reserve remains steadfast on getting closer to the goal of 2% inflation.

- As clues emerge on the path for Fed Funds Rate, we will look for the markets to broaden and given the level of cash on the sidelines, the move back into the markets could be robust.

- Student loan payments are set to restart in October, but we do not expect this to materially slow consumption.

Equity Performance and Key Takeaways

- We continue to be an advocate of equal weight rather than market cap weight portfolios as it results in more attractively priced allocation.

- Markets have seen solid gains in 2023, but the rebound has not been evenly distributed resulting in some asset classes looking more attractive than others.

- In disrupted markets, active management shines resulting in portfolios that look less like passive benchmarks with a focus on fundamentals and valuations.

- From a valuation standpoint, international equities continue to trade at a historical discount which could drive long-term returns.

- Small cap stocks continue to offer compelling valuations and should benefit from an eventual easing of interest rate stress as the burden of floating rate

debt decreases.

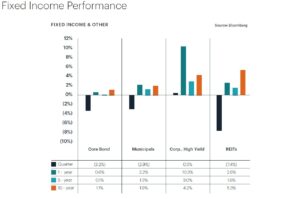

Fixed Income Performance & Key Takeaways

- Fixed income markets will have to adjust for the reality of higher for longer in rates and the potential widening of credit spreads if a recession does become a reality.

- Regardless of a soft landing or a recession, rates will come down in the future resulting in positive performance from duration management.

- Continue to favor a higher quality and lower duration portfolio as one additional rate hike is expected later this year.

- A looming recession could be a headwind to below investment grade debt, a sector we continue to leave out of our core fixed income portfolio.

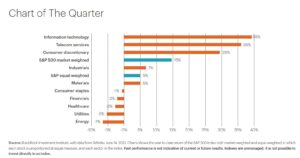

Chart of The Quarter

In many ways calendar year 2023 looks a lot like that of 2022. The most volatile assets in 2022 are some of the best performers this year. And we know the technology sector took the brunt of the market selloff last year. Growing evidence that the economy is slowing warrants allocations to the historically lower volatility sectors that have underperformed so far this year (although these sectors outperformed the past quarter). Not only do the lower volatility sectors offer the prospect of strong relative performance, these companies also trade at more attractive valuations given year to dat performance. Lower volatility stocks are currently trading at 17x earnings where global stocks are trading at 20x. As investors historically pay more for higher quality, the current discount is worth noting.

Wealth & Tax Management Key Takeaways

The last quarter of the year is an important time for our clients to capture any end-of-year tax planning opportunities.

Four simple strategies to consider:

- Maximize Company Retirement Plans. Maximize your 401(k) contributions as an annual discipline ($22,500 for plan year 2023; an additional $7,500 for ages 50+). If in a 24% or lower marginal tax bracket this year and expect to be in a higher bracket in the future, consider making Roth contributions if your plan allows.

- Utilize a Back-Door Roth IRA Contribution to Build Tax-Free Investments. As a high-earner not eligible for Roth contributions, utilize the “back-door” strategy by making an after-tax contribution into your traditional IRA, and immediately converting to your Roth IRA ($6,500 annual limit for 2023; $7,500 for ages 50+).

- Convert All or a Portion of Your Traditional IRA to a Roth IRA. For clients who have retired and find themselves in a much lower tax bracket (before starting Social Security benefits and reaching RMD age of 73), consider converting all or a portion of your traditional IRA into your Roth IRA.

- Optimize Your Charitable Giving. If age 70 ½ or older with a significant IRA balance, utilize Qualified Charitable Distributions (QCDs) to give directly from your IRA to charities tax-free. If younger than 70 ½ in a higher-than-normal taxable income year, consider bundling multiple years’ worth of charitable giving amounts into a Donor Advised Fund (DAF). This strategy maximizes itemized deductions, removes unrealized capital gains from your taxable portfolio, and offers you control around when to give to your chosen charities (now or in future years). We will continue to proactively address these and other strategies with our clients who might benefit by acting before year-end.

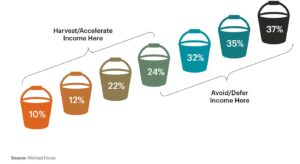

Wealth and Tax Management Chart of the Quarter

Many end-of-year tax optimization strategies revolve around assessing your marginal income tax bracket now versus the future. If you are in the 22% or 24% buckets now, and expect to be in the 32% – 37% buckets later, you likely want to accelerate income this year and pay taxes at lower rates. Similarly, if you are in the 32% – 37% buckets now and expect to be in the 10% – 24% buckets later, you should avoid and defer income if possible until later years. Minimizing our clients’ lifetime tax liability via year-over-year proactive tax bracket/bucket management is a key component of our ongoing wealth optimization process.

Janiczek Wealth Management – At a Glance

To learn more about Janiczek Wealth Management, click here.

Find Important Disclosures here.