The Setting Every Community Up for Retirement Enhancement (SECURE) Act passed in December 2019, making a wide array of changes to the retirement planning landscape. Almost 3 years later to the day, in the waning hours of 2022, Congress passed the SECURE Act 2.0 as part of the end-of-year 2023 Omnibus Spending Bill. While the SECURE Act 2.0 changes and adds more than 90 retirement related provisions, 6 are most relevant to our clients and other high net worth and high-income individuals:

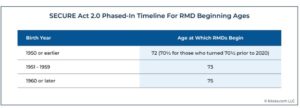

- The age when Required Minimum Distributions (RMDs) must begin from qualified retirement accounts increases from 72 to 73 starting in 2023, increasing again to 75 in 2033. This delay in the RMD age will create additional Roth IRA conversion opportunities for many of our clients in the coming years. In addition, beginning in 2023, the penalty for failing to take required distributions is reduced from 50% of the undistributed amount to 25%, with a further reduction to 10% if corrected in a timely manner.

- Starting in 2024, RMDs will no longer be required from Roth accounts in employer retirement plans.

- The annual limit of $100,000 for Qualified Charitable Distributions (QCDs) from retirement plans will now be increased annually for inflation, and the type of charities that can receive a one-time QCD is expanded to include charitable remainder unitrusts (CRUTs) charitable remainder annuity trusts (CRATs), and charitable gift annuities (CGAs), with certain limitations. Specifically, beginning in 2023, individuals have a one-time opportunity, limited to $50,000 (indexed for inflation), to use a QCD to fund a CRUT, CRAT, or a CGA. If a distribution is directed to a CRUT or CRAT, it must be the only form of funding for that trust.

- Employers will be able to provide employees the option of receiving vested matching contributions to Roth accounts within an employer plan, previously all matching contributions were made on a pre-tax basis.

- Starting January 1, 2025, individuals ages 60 to 63 will be able to make higher catch-up contributions (up to $10,000 indexed for inflation) to their employer retirement plan, however, if they earn more than $145,000 in the prior calendar year, all catch-up contributions at age 50 or older will need to be made to a Roth account in after-tax dollars – this is a significant change for high income savers.

- 529 plan assets held in a 529 plan that has been open for at least 15 years can now be rolled over into a Roth IRA in the name of the same beneficiary, subject to annual Roth contribution limits/requirements and an aggregate lifetime limit of $35,000.

It is important to note what is not in the SECURE Act 2.0 pertaining to high net worth and high-income individuals:

- Elimination or limitations on the use of the backdoor Roth or mega-backdoor Roth contributions

- Limits or restrictions on who can make Roth conversions

- Changing the age at which QCDs can be made to align with the new delayed RMD age of 73 (the QCD start age continues to be age 70 ½)

- Creation of non-age based RMDs such as potentially requiring balances in excess of a specified amount to be distributed regardless of age

- Implementing new restrictions on Qualified Small Business Stock (QSBS)

- Eliminating new types of investments like privately held investments from being eligible to be purchased with IRA money

- Clarifying the rules in which the 10-Year Rule created by the original SECURE Act should be implemented for Non-Eligible Designated Beneficiaries

Given these significant changes to the retirement planning landscape, and the complexities of multiple implementation timelines, it is more important than ever to review your retirement plan and tax strategies with a trusted advisor to ensure you are maximizing the opportunities these changes create. If you would like a second opinion from one of our advisors, please complete our contact form or reach out to Cathy Wegner at 303-339-4480 or cwegner@janiczek.com.