April 2024

Investment Conditions & Outlook

Executive Summary

Spring has sprung with the U.S. stock market not missing a beat from where we ended last year. Optimism over the economy and interest rate cuts combined with the exuberance around opportunities in artificial intelligence resulted in indexes hitting new all-time highs.

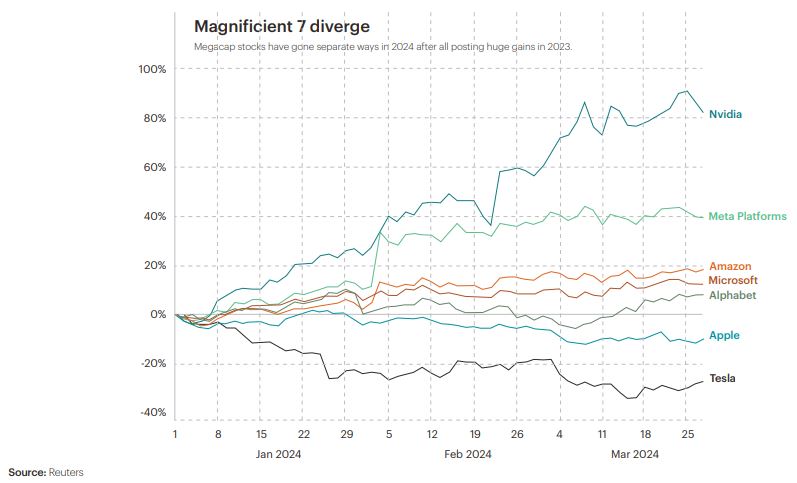

The stock market continues to be propelled by some of the megacap companies that carried the markets in 2023. The “Magnificent Seven” posted huge gains in 2023, but this year we have seen them go their separate ways (see chart of the quarter) with broader equity market participation. This year’s performance has reaffirmed early signs investors are beginning to rotate portfolios to look for opportunities outside of big tech and in anticipation of lower rates later this year.

Much of the market euphoria is in anticipation of the Fed turning dovish and cutting interest rates. The Fed’s dilemma is that delaying rate cuts and easing too slowly could result in a recession, while easing too quickly could trigger a rebound in inflation. We believe the Fed will stay the course until later this year before we see any rate cuts. Our main concern is the Fed’s caution regarding stagflation (as we continue to run above the long-term goal of 2%). It does not look feasible for rates to come down in Q2 as the Fed remains data dependent wanting to see a continued decline in core inflation. Realistically we see the Fed starting to ease in Q3 of this year at the earliest.

It looks like we will see a rematch between President Biden and former President Trump. Concerns over Biden’s age and Trump’s legal issues left the door open for other party replacements that could not capitalize on the opportunity. We can look at technical market analysis to give us clues on what we could expect for this presidential cycle:

- The strongest period of the cycle is from the middle of the election year to the middle of the post-election year with small caps and value outperforming.

- The weakest period has been from the middle of the post-election year to the end of the mid-term year.

- On average, the first half of election years are weak and the second half strong with the timing of the election rally varying greatly and often dependent upon when the winner is widely accepted.

Regardless of what history has given us, this looks to be a rematch that few Americans want later this year. It is unprecedented to see a rematch in modern U.S. presidential elections. Our portfolios remain well positioned regardless of the outcome. We continue to focus on strong fundamentals in the run-up to the election to help combat an inevitably volatile time period.

We entered this year with cautious optimism and the idea markets could continue to rally and the hope the rally would spread to sectors other than technology. There continues to be a wide dispersion between the best performing and worst performing sectors. The expectation of the economy achieving a soft landing and the Fed turning dovish could result in this discrepancy gap closing and strong relative performance for portfolios. While hints of speculative behaviors are emerging, driving stock valuations higher, this does not look like the extremes experienced in 2000. Even so, we continue to focus on quality fundamentals at an attractive price to avoid falling victim to the “this time is different” trap.

The Janiczek Team

Economic Conditions & Key Takeaways

- The global economy is expected to slow in 2024 but the shift to a more dovish stance in central banks lessens the chance for a meaningful recession to materialize.

- The path for a soft landing continues to look viable with recession risk easing, but we are not out of the woods as earlier policy tightening still works its way through the system.

- Uncertainty remains and we will continue to monitor diminishing household savings, a slowing labor market and a yield curve that remains inverted.

- Geopolitical events continue to linger with multiple flashpoints around the world with a pending election cycle later this year.

- With the U.S. being in an election year, drama and volatility are almost certain as fiscal issues are poised to be focal points for both campaigns.

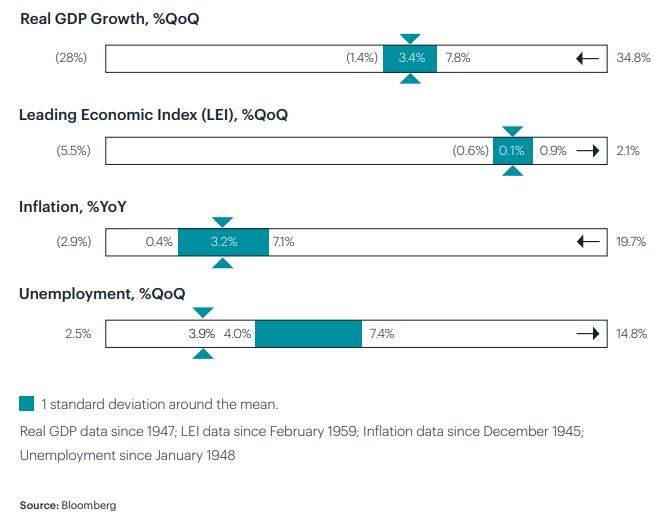

Economic Conditions

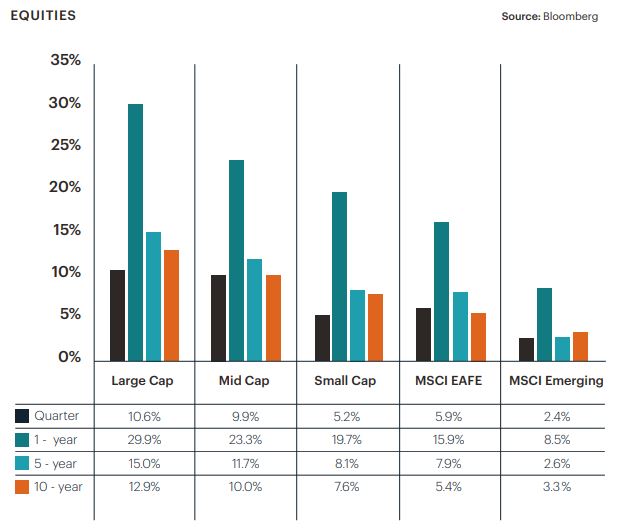

Equity Performance & Key Takeaways

- We continue to see a broader market rally beyond just tech, with consumer discretionary and industrial sectors moving higher.

- A weaker dollar and lower interest rates should offer a tailwind for developed and emerging markets stocks.

- Small caps hit their lowest valuation in years due to economic and interest rate sensitivities making them attractive buys for the long-term investor as the economy continues to expand.

- China’s economic performance has been challenged but the underlying growth performance has remained strong.

- Equity markets (mainly U.S. large) remain constrained by expensive valuations, excessive optimism, and overbought sentiment.

Equity Performance

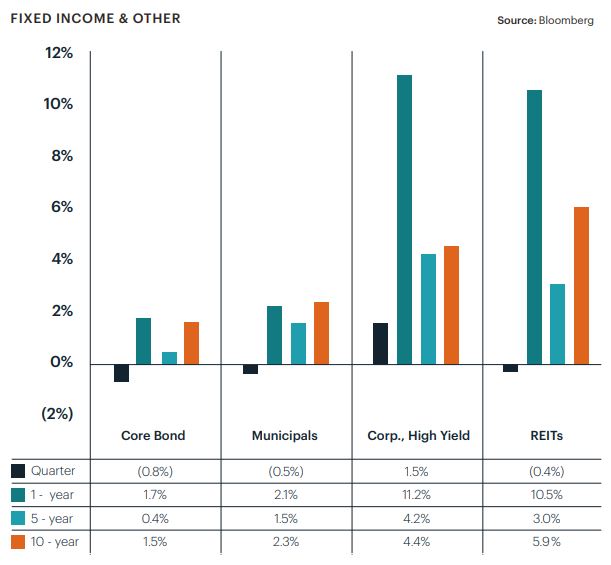

Fixed Income Performance & Key Takeaways

- A relatively lackluster start to the year for bonds because of an over-enthused market at the end of last year pricing in early 2024 rate cuts.

- It looks like the readjustment of bond yields higher to a normalized level is largely behind us with the outlook of rate cuts looking more likely.

- Bonds continue to act as the safety net in portfolios to offset equity market volatility and economic weakness.

- Fundamentals for fixed income continue to look attractive as economic growth remains healthy and the outlook for lower short-term rates looks promising.

- Money markets and government paper continue to look attractive with yields meaningfully higher than inflation.

Fixed Income Performance

Chart of the Quarter

So far this year we have continued to see the markets being propelled by some of the megacap companies that led last year. As you can see in the above chart, others have not faired as well. As valuations continue to surge, investors are looking for better prices and rotating their portfolios away from last year’s winners. This continues to bode well for our portfolios and the tilt to better valued companies.

Wealth & Tax Management Key Takeaways

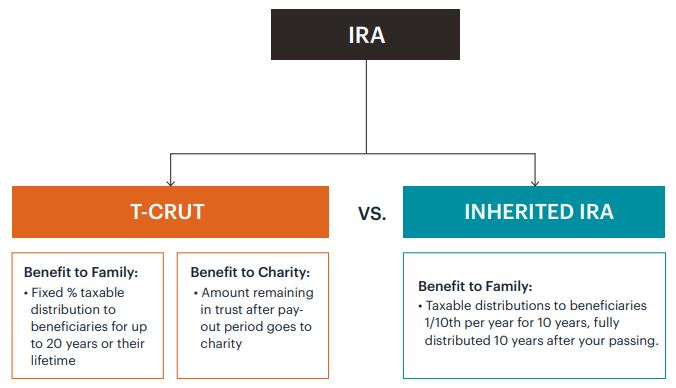

The SECURE Act passed by Congress at the end of 2019 did away with the “stretch inherited IRA”, now requiring non-spouse beneficiaries (with few exceptions) to withdraw the entirety of an inherited IRA within 10 years of the account owner’s death instead of over their lifetime. This has created tax planning challenges especially for those clients with significant IRA balances with non-spouse individuals as designated beneficiaries, who would need or benefit from smaller annual distributions for an extended period beyond 10 years.

One strategy that can be extremely effective in these instances is the utilization of a Testamentary Charitable Remainder UniTrust (TCRUT), especially for those who want to provide for their family first, and then leave money to charitable organizations as part of their legacy.

A T-CRUT is a trust that is funded by an IRA via beneficiary designation at one’s death. Because a T-CRUT is not subject to the 10-YearRule, it has the ability to make ongoing fixed percentage taxable distributions out of the trust to one or more beneficiaries for up to 20 years (or the life of the beneficiary). At the end of the payment term, the trust terminates and sends whatever is left (the remainder interest) to a chosen qualified charity.

Not only does a T-CRUT stretch taxable payments to income beneficiaries, but it also results in no income taxes being owed when the IRA is paid out to the T-CRUT and the end charities, plus it reduces one’s taxable estate by the value of the remainder interest going to charity.

This strategy is an example of a legacy solution we will explore with our clients during financial planning meetings and Clarity Sessions.

Wealth & Tax Management Chart of the Quarter

A T-CRUT can be an attractive strategy if you want to benefit individuals/family and charity with your qualified retirement plan assets, essentially “Giving It Twice.”

If you would like to learn more about Janiczek Wealth Management and our investment and wealth management services, please contact Cathy Wegner, Director of New Client Engagements, at 303-339-4480 or cwegner@janiczek.com.

The Janiczek Story

To learn more about Janiczek Wealth Management, click here.

Find Important Disclosures here.