January

2022 Investment Conditions & Outlook

Executive Summary

With the backdrop of continued global reopening and consumer resiliency, 2021 did not disappoint from an equity returns standpoint. Is another big gain in store for 2022? Although we foresee 2022 being positive for the equity markets, the forecast looks significantly different than the year we had in 2021. New risks have emerged that investors are not accustomed to. We see 2022 being more of a transition year where growth rates continue to move back towards long-term averages and interest rates inch up as the Fed increases their hawkish tone to help control inflation.

After a year of COVID variants and uncertainty, the American economy seems to be healthy again and on track for solid growth in the new year. The impact of the global pandemic has remained with us in small and large ways, especially over the past month with the surge in Omicron variant. COVID and COVID-related rules should have much less influence on our lives (and the markets) as we move through 2022.

Though solid, we expect economic growth to slow from the pace experienced in 2021 to a range of 3-4%. As things return to the new normal, the economy could still face headwinds from COVID mutations and diminishing fiscal and monetary support. We foresee strength coming from a continued economic reopening that drives consumer spending, led by travel, entertainment, and other services. Household net worth has hit new all-time highs thanks to higher savings rates and rising asset prices, and the trillions now sitting in sidelined cash should continue to fuel spending growth in 2022.

A bigger question is inflation and the term “transitory”. How much higher can inflation go and how long will heightened levels last? The Fed has maintained the transitory nature of inflation, but as time goes on it looks like inflation could remain elevated throughout 2022 as we wait for supply and demand to come back into balance. By the end of the year, however, inflation in the 3 to 3.5% range should subside more problematic inflation concerns.

Looking into 2022 we expect another year of positive equity returns with increased periods of volatility. Asset class positioning and being prepared to rebalance at potentially opportunistic times is recommended. We expect interest rates to continue to rise modestly in 2022, posing a headwind for fixed income investors. We continue to look outside of traditional bonds for higher yielding fixed income alternatives while keeping some of the superior risk mitigation characteristics of traditional high-quality holdings. See further details and commentary inside this report. As always, call with any questions.

The Janiczek Team

Economic Conditions and Key Takeaways

- Continued economic growth above long-term average, a still elevated inflation target of 4%+, and lower fourth quarter unemployment all favor risk assets.

- Supporting the continued economic expansion is high cash savings, accumulated wealth, and continued room to make up for COVID losses in certain sectors.

- Slower economic growth and lower, but still elevated, inflation will be contributors to year-end economic targets as the economy continues to grapple with supply and demand mismatches.

- The Build Back Better Act’s plan to increase entitlements is facing headwinds and at this point the outcome looks like a much smaller spending bill or nothing at all.

- A firmer dollar should keep pressure on developed and emerging currencies.

Equity Performance and Key Takeaways

- Stocks are poised to deliver positive returns in 2022, albeit lower than 2021 as earnings growth slows and Fed tightens monetary policy.

- Growth stocks and value stocks took turns of outperformance during 2021 and this trend could continue in the new year: growth on top if interest rates remain low, value if rates continue to rise and inflation stays elevated.

- Prolonged performance of U.S. equities has been mainly supported by a small subset of companies and as global growth broadens, we could see new global leaders emerge (we look to international markets for long-term diversification).

- U.S. equity markets enter the year at elevated valuations relative to history, but still well below dot-com era extremes.

- A combination of low relative valuations, ongoing monetary support and upward trending earnings bodes well for non-U.S. developed markets moving forward to “catch up” to domestic equity markets.

- Emerging markets struggled to keep pace in 2021 and we expect EM opening and mobility to rise as vaccinations rates catch up with developed markets, but the regulatory overhang from China remains a dark cloud.

- A firm U.S. dollar could be a headwind for international equity performance in 2022 (we remain underweight international equities)

Pandemic Conditions & Key Takeaways

- Emergence of Omicron variant has highlighted influence of COVID on sector leadership.

- Value sectors tend to outperform when COVID cases are falling, and growth sectors when cases are rising.

- Back and forth leadership between growth and value during different periods of COVID reported cases has resulted in the S&P becoming resilient to COVID uncertainty and kept correlations between sectors low.

- A normalization of correlations in 2022 would suggest COVID is no longer a top concern of equity investors.

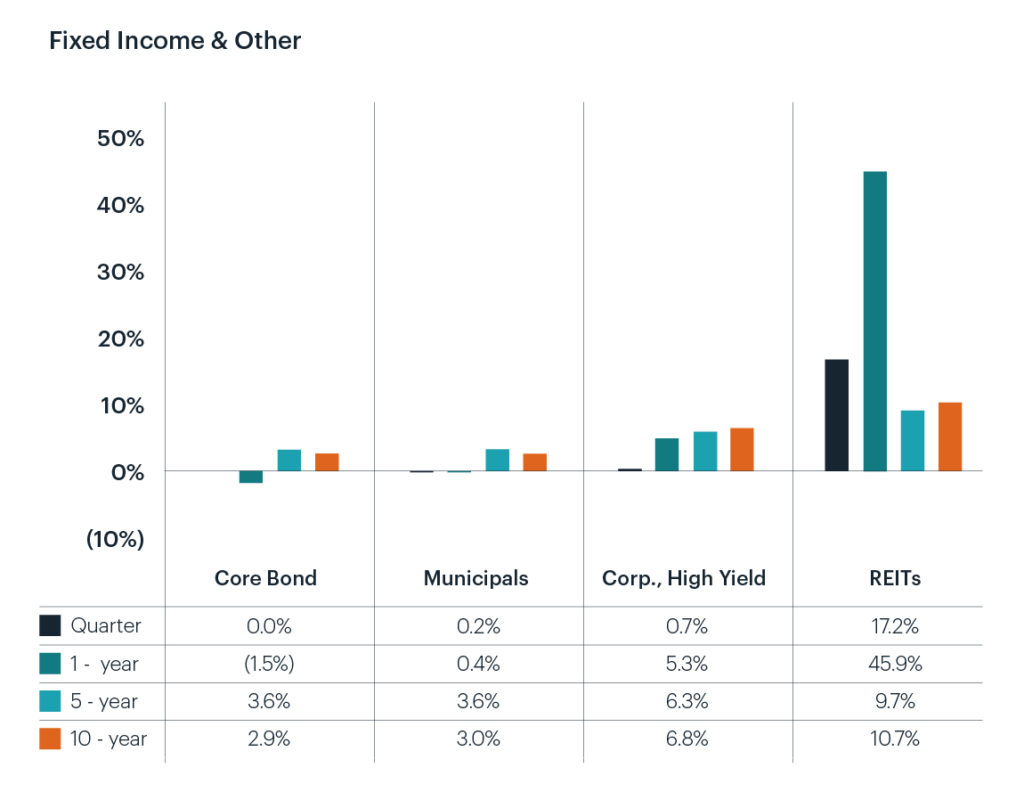

Fixed Income Performance & Key Takeaways

- Low bond yields and tightening Fed policies set the stage for low bond returns and potential for higher volatility in 2022.

- While yields are expected to remain low for bonds, the diversification effect bonds offer a portfolio to protect against drawdowns in stocks remains proven.

- While our actions to underweight bond exposure, reduce duration and pursue less liquid alternatives are prudent, maintaining a high quality fixed income portfolio helps to control risk and offers dry powder in the event of a market correction to facilitate a rebalance into lower priced equites.

- Real estate performance remained strong in Q4 rounding out the year for top overall performance and continues to exhibit strong fundamentals and higher yield potential in 2022.

- Municipal bond space benefited from stronger than expected tax revenues and bodes well for the asset class looking forward in an environment of increased taxes and constrained supply.

- In rising rate environments, we favor allocations to short and intermediate term fixed income and will continue to explore allocations to nontraditional bond alternatives.

- We prefer U.S. issues over bonds in developed and emerging markets.

- Given a difficult forecast in fixed income markets, we will continue to explore and expand our allocation to the higher yielding private markets.

Wealth & Tax Management Key Takeaways

While proactive tax planning is crucial, we cannot with absolute certainty predict what, if anything, will come out of Washington D.C. Because of this uncertainty, we’d like to share some key information that we feel our clients should be reminded of as we enter 2022:

- Stay Disciplined to the 35 Essential Strengths® of our Wealth Optimization Plan. Janiczek will assess your balance sheet to key ratios, along with your cash flow statement, your insurance, asset, and estate protections to help you maintain solid strength, agility, flexibility, and endurance (SAFE™) measurements.

- Stay disciplined to our Evidence-Based Investing (EBI) process. The news, politics, and talking heads can all get in the way of long-term investing success. Casual tax talk and/or cocktail talk can cause a faulty assessment of the situation or lead to rash emotional decisions. Rather than delving too deeply, it is best to maintain a balanced risk/reward profile by utilizing Janiczek’s guidance, tools, and expertise.

- Stay disciplined to our semi-annual Clarity Session routine. Our average Clarity Session Rating from clients is 9.86 out of 10! Our team creates these agendas to keep you on track with all our best practices for wealth, portfolio, tax, and retirement planning.

- Stay disciplined to our Lifestyle Protection Analysis (LPA). This robust analysis stress tests your finances to assist you in making rational decisions across all wealth management disciplines.

- Enjoy your freedom of time, money, purpose, and relationships in all aspects of your life. Having the financial freedom to Flourish 360™ is a wonderful opportunity.

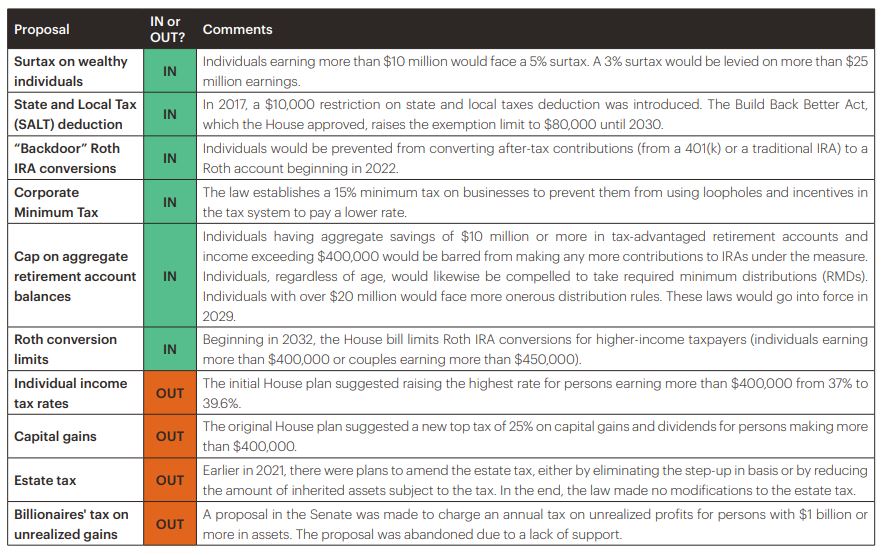

Legislative Environment and Key Takeaways

- As is often the case when Congress and the Presidency change hands, there were numerous government-issued press releases about potential tax code changes in 2021. Janiczek Wealth Management has assessed these bills and presented potential tax planning strategies through their various iterations (beginning with the Treasury’s “Green Book” and ending with the House-approved Build Back Better Act on November 19, 2021). It is critical to remember that nothing is final until the House, Senate, and President Biden sign the final legislation. That being said, acting on proposed legislation entails its own set of risks; thus, you should consult with Janiczek Wealth Management as well as your CPA, estate attorney, or other qualified experts to analyze and assess the benefits and downsides of each action and inaction.

- As of the publication date of this report, the Senate had stalled the BBB legislation, and it appears more likely that it will not pass the Senate in its current form. Being that as it may, the table below provides an IN/OUT summary of the House-approved Build Back Better Act; some, none, or all these changes may be reflected in the newly revised 2022 legislation.