October 2021

Investment Conditions & Outlook

Executive Summary

The world’s economic response to the COVID recession has been vastly successful. Countries responded quickly when faced with sharp declines in economic activity and unknowns. The result of massive monetary and fiscal stimulus was a V-shaped recovery in equities. But as global growth begins to slow, what comes next?

The third quarter saw the post pandemic recovery significantly slow its pace resulting in an increase of equity market volatility. We have seen an up-tick in inflation due to continued concerns of a more hawkish Fed and inevitable tapering of asset purchases. The spike in inflation has been larger than expected, but we still believe it’s transitory, caused by base effects from last year and continued supply chain bottlenecks. Inflation could remain inflated for the remainder of the year, but we expect a decline in early 2022.

Another concern worth noting is the highly contagious COVID-19 delta variant. Evidence shows vaccines are effective in preventing serious illness and the spread of infections. We continue to see vaccine rates increase globally and emerging economies catching up to their developed peers. As of now, infection rates look to have peaked globally, and the reopening of economies should continue over the remainder of the year.

Our investment positioning is broadly unchanged from last quarter. U.S. equities remain expensive, with better valuations existing globally. The difference in valuations reinforces our globally diversified equity allocation. The expectation of a continued strong economic cycle delivers a preference for equities over bonds even with increased periods of volatility. We remain bullish for now and realize we have been in a pristine environment for stocks coming off bottoms of last year. This will continue to be monitored and equity overweight could be reduced if cycle begins to slow during the quarter.

The Janiczek Team

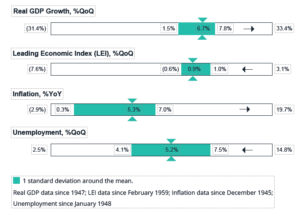

Economic Conditions and Key Takeaways

Key points

- Near term health of U.S. economy continues to support strong quarter and year end GDP forecast.

- Stimulus driven surge in demand resulted in inflation running at breakneck speed.

- We feel inflation peaked in the second quarter and expect it to soften for the remainder of the year into 2022.

- Slight slowdown in Leading Economic Indicators as recovery matures.

- Continued economic recovery evident in further drop of unemployment rate as workers continue to move back to fulltime positions.

Equity Performance and Key Takeaways

Key points

- Difficult quarter in the equity markets as the summer saw reversals of reflation trade as fears centered on Delta variant, but we retain a favorable outlook with subdued returns compared to what has been experienced so far in 2021.

- The reopening trade should resume in coming months, and we would expect to see cyclical value stocks report stronger earnings and upgrades than tech heavy growth stocks.

- Financial stocks should benefit from continued yield curve steepening which increases profitability.

- Emerging market stocks have been poor performers, but we see encouraging signs as vaccine rollouts continue to accelerate.

- Developed market equities retain catch-up return potential due to relatively high exposures to economically sensitive sectors.

- New cycle of economic expansion could bring new leadership by international stocks relative U.S. stocks supported by increased growth and better valuations.

- Starting points matter, so we would not expect a blowout return quarter at this stage in the recovery but remain constructive on U.S. stocks with strong fundamentals.

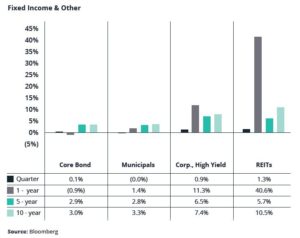

Fixed Income Performance and Key Takeaways

Key Points

- A slight uptick in yields for the quarter resulted in flat core bond returns.

- Core bonds continued their role as portfolio stabilizer as equity market volatility increased.

- Assuming labor market remains strong, Fed should begin tapering asset purchases, but does not mean

they will rush to raise short term rates. - Longer term treasury yields will likely continue to rise as economic growth continues.

- As rates continue to increase, we will be running diligence on nontraditional fixed income investments and

vehicles to help augment a more challenging fixed income market. - We continue to be underweight duration (interest rate sensitivity) in fixed income allocation.

Wealth & Tax Management Talking Points

- The debate in Washington, D.C. has kept the wealth and tax planners at Janiczek on their toes for the previous

six months. The discussion began with the Biden Administration’s Tax Plan via the Treasury’s Green Book, which

proposed significant changes to present taxation law, effectively increasing taxes on the wealthy and putting key

tax and financial planning techniques in jeopardy. - Beyond the proposed substantial increase in tax rates applicable to many of our clients, the Treasury’s Green

Book presented two additional modifications for consideration: restricting the efficacy of 1031 exchanges and

removing the step-up in basis for the beneficiaries of the deceased. Fortunately, as of this writing, these additional

amendments have not been incorporated into the active Senate bill, which is in the process of being drafted for an

eventual final vote. We discussed these initial proposals in the Q2 commentary (click here to review our July 2021

Wealth & Tax Management Talking Points). - While these noteworthy amendments do not appear to have made the cut, Congress does not appear to be failing

in keeping the tax code ever-changing, complex, and challenging. Until such legislation makes it through the

House, Senate, and Executive branches, there is no certainty about what will become law and when it will become

effective. Nevertheless, the parties’ and politicians’ spending, taxation, and regulation postures are somewhat

transparent and point to a very likely increase in taxation given the stated party line and reported positions of

moderate politicians within each party.

Below, we outline the key components of the current plan, and we will continue to monitor developments. In the quarter

ahead, we will be working closely with clients who elect to act on specific tax planning tactics before year-end.

TAX AND INVESTMENT PLANNING

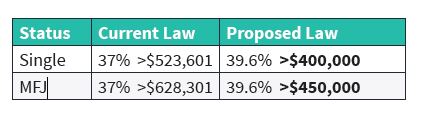

- Ordinary Rates: The current proposal would reverse the Tax Cuts and Jobs Act of 2017 and restore the top marginal income-tax rate to 39.6%. The new rate would be enforceable at a much lower threshold of $400,000 taxable income for single filers and $450,000 taxable income for married filing jointly. If passed, this is effective for taxable years after December 31, 2021.

- Long-Term Cap Gains: The proposed bill raises the highest capital gains rate from 20% to 25%. This rate would also apply to qualified dividends. This capital gains rate hike would begin at $400,000 for single taxpayers and $450,000 for joint filers, following the increase in federal tax rates and lower thresholds. This new rate is a compromise compared to the original proposal of a 39.6% capital gain rate. The effective date of this new rate might be as early as September 13, 2021 (when the Act was introduced), the actual date the tax law is enacted, or it could be altered in last-minute negotiations to be effective January 1, 2022. Stay tuned.

- Net Investment Income Tax: The 3.8% net investment income (NIIT) surtax would apply to company income earned in the ordinary course of business. By including a business’s active income that is not subject to self-employment tax, this extension would raise the overall tax. This revision would include profits from the sale of business assets in nonpassive enterprises and any gains from the sale of S corporations and partnerships. If enacted, this would impact individuals having a Modified Adjusted Gross Income (MAGI) of more than $400,000 and married couples with a MAGI of more than $500,000.

RETIREMENT PLANNING

- Backdoor Roth IRA Elimination for High Earners: The plan eliminates the so-called “backdoor” Roth IRA approach for single filers with taxable income of more than $400,000 and joint filers with taxable income of more than $450,000. The effective date specifies that this will apply in the years following December 31, 2031. While it is a non-issue, for now, clients should work in coordination with Janiczek Wealth Management and their CPA to determine if Roth conversion strategies could improve your overall wealth accumulation and preservation results.

- Elimination of Mega Backdoor Roth: The Mega Backdoor Roth allows taxpayers to put up to $38,500 of after-tax dollars in a Roth IRA or Roth 401(k) in 2021. To perform a mega backdoor Roth, your 401(k) plan needs to allow for “after-tax” contributions and either allow for in-service withdrawals to a Roth IRA or allow you to move money to a Roth 401(k) plan.

- Under this proposal, all employee after-tax contributions to qualified plans are prohibited.

- Furthermore, the proposed bill prevents the conversion of after-tax IRA contributions to Roth IRAs regardless of income level, effective after December 31, 2021.

- Limiting Contributions and Enforcing Minimum Required Distributions Based on Combined Value of IRAs and Defined Contribution Retirement Plans: These revisions are two separate sections in the proposal, but they focus on the same taxpayer.

- First, if a taxpayer is in the highest marginal tax rate (39.6%, under proposed law) AND the aggregate value of their IRAs and defined contribution retirement plans exceeds $10,000,000, then this legislation prohibits further contributions to a Roth or Traditional IRA for that given taxable year. As emphasized above, taxpayers must meet both criteria for this rule to apply.

- Second, if a taxpayer is in the highest marginal tax rate (39.6%, under proposed law) AND the aggregate value of their IRAs and defined contribution retirement plans exceeds $10,000,000, then a minimum distribution is required to be taken. This minimum distribution is 50 percent of the amount by which the individual’s prior year aggregate traditional IRA, Roth IRA, and defined contribution account balance exceeds the $10 million limit.

- Furthermore, if the total balance in traditional IRAs, Roth IRAs, and defined contribution plans exceeds $20 million, the excess must be distributed from Roth IRAs and Roth designated accounts in defined contribution plans up to the lesser of (1) the amount required to bring the total balance in all accounts down to $20 million or (2) the aggregate balance in all accounts. If Roth accounts are depleted, the taxpayer is allowed to take from traditional retirement accounts.

- Restriction on IRA Investments: The bill prohibits an IRA from holding any security if the security issuer requires the IRA owner to meet the accredited investor definition.

ESTATE PLANNING

- Grantor Trust Changes: The proposal makes several modifications to grantor trusts.

- First, it enables the grantor trust to be included in the taxable estate of a decedent where the decedent is the deemed owner of the trust. Previously, the legislation allowed taxpayers to transfer assets from their estate into a grantor trust while closely controlling the trust.

- Second, a gift tax would be triggered on most distributions from a grantor trust to a trust beneficiary.

- Third, sales between grantor trusts and their deemed owner are similar to sales between the owner and a third party. Federal income tax would be levied on sales to the grantor trust. Because the sale would be considered as a realization event, with the grantor realizing taxable gain, this law renders a grantor trust unworkable for gift planning purposes.

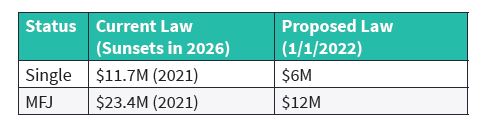

- Gift/Estate Tax Exemption: The gift/estate tax exemption currently is $10 million, adjusted for inflation ($11.7 million in 2021). The exemption reverts to $5 million, plus

inflation, in 2026. Instead, the proposed law would make this change effective January 1, 2022, resulting in an exemption of about $6 million in 2022. These numbers are per individual, each amount is doubled for married taxpayers. See table.

EXPANDED TAX PLANNING COLLABORATION OPPORTUNITIES

Janiczek Wealth Management can uncover collaborative tax planning possibilities to assist you in effectively navigating these complex situations. This has and continues to be a growing component of our Complete Wealth Solution. Here are a few things to think about now:

Tax and Investment Planning: It is essential to look at your income from a variety of angles. We recommend collaborating with your Janiczek Team, CPA, and Tax Attorney to project multiple years of income to identify the best timing to realize capital gains. Once you’ve discovered timing possibilities, it’ll be critical to be able to capitalize on tax-loss opportunities and examine deduction timing. The current proposed plan suggests that the higher capital gains tax may be in effect as of the introduction of the draft law on September 13, 2021. A prior binding written contract would allow a taxpayer to waive the effective date.

To support this process, we continue to create and acquire advanced tax planning software solutions. In fact, if we get a PDF copy of your tax return each year, you will begin seeing some additional reports in your next Clarity Session (Best Practice Tip: using our secure portal, be sure to send us a copy of your tax return each year after it is filed).

Retirement Planning: Allow your Janiczek Team, CPA, and Tax Attorney to calculate the impact of Roth conversions on your retirement plan. Consideration of Roth conversions will also allow you to take advantage of the proposed 10-year period under the proposed bill.

If your aggregate retirement plan balances exceed $10,000,000, closely monitoring your taxable income will be necessary. Remember, as of the proposal, the minimum distribution requires both criteria to be met: high taxable income and a large retirement plan balance.

Furthermore, find out whether your business enables “after-tax” contributions, as well as in-service withdrawals to a Roth IRA or money flowing into a Roth 401(k). If this is the case, you should consider the Mega Backdoor Roth conversion. Elimination of the Mega Backdoor Roth conversion will almost certainly pass without a hitch.

Finally, screen and monitor your IRA for prohibited investments. Owners of IRAs have until January 1, 2024 to extract these investments and comply completely. It is in our client’s best interests to explore a solution as soon as the new tax code is adopted.

Estate Planning: Examine your present estate plan to ensure optimal planning in 2021 and beyond. Consider accelerating gifting strategies by year-end if you intend to make substantial gifts to take advantage of the temporarily greater exemptions.

Because trust modifications are complicated, clients should consult with Janiczek Wealth Management and their estate attorney to decide the best course of action. The effective date of grantor trust taxation is likely the date of the bill’s enactment, and its application would be to any grantor trust created on or after that date, as well as to any contribution to an existing trust on or after that date. The following estate planning strategies would be impacted: grantor retained annuity trust (GRAT), spousal lifetime access trust (SLAT), irrevocable life insurance trust (ILIT), and qualified personal residence trust (QPRT).

ENDING NOTES

While the wealth and tax planners at Janiczek expect these substantial tax reforms to be enacted in some form, there is yet to be an actual vote on the active Senate bill. Furthermore, we have no certainty about when such modifications will take effect (last minute negotiations can quickly change the actual tax code and effective dates actually passed by Congress). Acting on proposed legislation carries its own set of risks; therefore, it is critical that you consult with Janiczek Wealth Management as well as your CPA, estate attorney, or other qualified professional to strategize and assess the benefits and drawbacks of each action and inaction.

Chart of the Month – September 2021

10-year treasury yields increase, headwind to tech

The growth scare that prompted investors to seek safety in technology companies is overdone as the economic drag on the economy from the Delta variant should be short lived. The chart shows the correlation between 10-year treasury yields and the technology heavy S&P 500 Growth Index. As yields increase, we would expect the index to underperform as investors move to higher yielding bonds. We saw this trend earlier in the year and with yields rising again, we would expect a similar outcome. We will continue to be underweight growth in our allocation and favor more sensitive companies and sectors as the global reopening marches on.

Janiczek Wealth Management – At a Glance

To learn more about Janiczek Wealth Management, click here.

Important Disclosures

The content herein is to be used for informational purposes only. Neither Janiczek Wealth Management or its owners and employees represent or warrant the accuracy or completeness of the information contained in this report. In no event will Janiczek Wealth Management or its owners or employees be liable for any damages that may result from the use of or reliance on these materials.

Past performance may not be indicative of future results. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy (including the investments and/or investment strategies recommended and/or undertaken by Janiczek® Wealth Management (“Janiczek®”), or any non-investment related services, will be profitable, equal any historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Janiczek® is neither a law firm nor accounting firm, and no portion of its services should be construed as legal or accounting advice. Moreover, you should not assume that any discussion or information contained in this document serves as the receipt of, or as a substitute for, personalized investment advice from Janiczek®. Please remember that it remains your responsibility to advise Janiczek®, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/ evaluating/ revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. A copy of our current written disclosure Brochure discussing our advisory services and fees is available upon request. The scope of the services to be provided depends upon the needs of the client and the terms of the engagement.

TM & Copyright Janiczek Wealth Management. All rights reserved. Do not reproduce or redistribute in any form without prior written permission. Strength Based Wealth Management® 35 Essential Strengths®, The Stages of Financial Freedom®, Wealth Optimization Plan™, Wealth Optimization Dashboard™, Lifestyle Protection Analysis™, Elastic Limit Wealth Threshold™, Flourish! Activators™, FLOURISH!™ and Flourish! Based Retirement Planning™ are all trademarks of Wealth with Ease, LLC. For details, call 303-721-7000.