July 2021

Investment Conditions & Outlook

Executive Summary

The global healing process continued and has progressed into a genuine economic recovery. Equity markets have hit new all-time highs, earnings are surging, and bond

yields are on the rise. As of mid-June, vaccination rates were close to 50% in the United States and Europe, and over 60% in the United Kingdom.

Global reopening should continue across developed economies through the second half of this year. Emerging economies have been laggards since the vaccine rollout, but we expect this to reverse as the year goes on as growth stabilizes and vaccines become more available across these countries.

The retracement in the U.S. markets have caused other issues to come into focus. Mainly the implications of inflation and the timing of the central bank to taper asset purchase and eventually raise interest rates. We continue to be in the transitory inflation camp believing inflation is a result of falling CPI last year and global supply bottlenecks. We expect it will take until mid to late 2022 for the U.S. to recover fully from lost output and inflation pressures are likely until then. We also expect the Fed to remain dovish for the remainder of this year, commencing tapering in 2022 and holding rates steady until 2023.

Our views on asset allocation are largely unchanged from last quarter and we continue to favor equities over bonds. Although global equities remain expensive, we still believe the return profile is favorable when compared to fixed income. Investor sentiment is trending in overbought territory and trending closer to market Euphoria. We continue to favor the value factor relative growth and expect non-U.S. equities to start to close the year-to-date performance gap.

The Janiczek Team

Economic Conditions and Key Takeaways

Key points

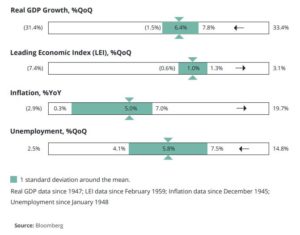

- The U.S. economy charged on through the second quarter fueled by increased spending and corporate balance sheets that had been cut to the bone.

- The reopening theme can be seen in a continued drop in the unemployment rate as workers continue to move back to fulltime positions.

- The leading economic indicators index continues to carry positive momentum remaining in line with the reopening theme.

- Inflation came in higher than we anticipated from a combination of supercharged demand from stimulus checks and disrupted supply chains, but we expect inflation to move back towards Fed’s target of 2%.

- We expect continued strong economic growth for the remainder of the year with a GDP of around 7% for 2021 (strongest since 1984).

- While consumers are quickly transitioning back to pre-pandemic activities, many businesses are sorting out a variety of HR and operational related challenges and opportunities. Signs of certain businesses not having the employees to fill vacant roles and/or not having the supply of product/inventory to meet elevated demand is at least a transitory issue. Also, lessons learned and new preferences and trends about 100% in-office versus partial, permanent, or flexible remote work policies is the rage. In short, from a creative destruction economic and investment standpoint, there are and will be new winners and new losers as this all sorts out over the next decade. Organizations that meet our “SAFE” standards of Strength, Agility, Flexibility and Endurance will likely prevail. So will entrepreneurial organizations who spot and pursue trends, efficiencies, and opportunities early-on and maintain the focus and drive to prevail.

Equity Performance and Top Takeaways

Key points

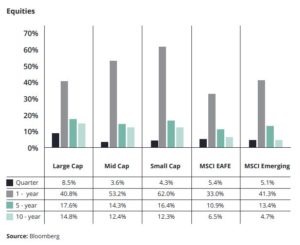

- Another strong quarter for global equities led by domestic large cap stocks (we currently are overweight this asset class).

- Value stocks continue to outperform and are reporting stronger earnings upgrades than tech heavy growth stocks (this is also in line with our factor tilts).

- International equities are overweight value stocks relative U.S. tech heavy exposure, and this dynamic should help drive relative performance for international equities for the remainder of year.

- Emerging markets have been laggards since vaccine announcement, but this trend should start to reverse later this year with vaccine rollouts across emerging markets. We have been underweight emerging markets and may increase our target for this asset class, but transactions could have a significant capital gain tax consequence in many cases, diminishing our interest in making the trade in taxable accounts and/or in accounts that do not have the “benefit” of capital loss carryforwards from other activities.

- Consumer confidence is nearly back to pre-recession level supporting positive economic outlook for second half of year and positive outlook on equities.

- Persistent inflation could lead to more hawkish Fed tone that could challenge equity markets when compared to current low level of interest rates.

- Indicators are still positive for equities and should remain that way until Fed increases interest rates to the point of slowing economic activity

Fixed Income Performance and Top Takeaways

Key Points

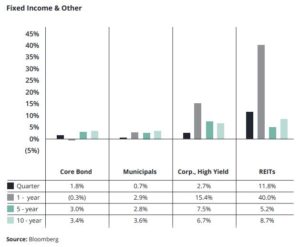

- Interest rates retraced from highs this quarter and resulted in positive returns across core, municipals, and high yield bonds.

- High yield bonds and credit remain expensive on a spread basis but could benefit from corporate profit growth and low default rates.

- Long duration bond yields should come under continued pressure as banks look to taper back asset purchase, supporting our low duration positioning.

- International dollar denominated bonds have had a rough year but should benefit from U.S. dollar weakness through economic recovery.

Wealth & Tax Management Key Takeaways

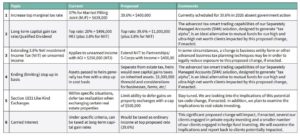

- On May 28th, the U.S. Treasury Department released the “Green Book”, which was a 114-page explanation of the tax reform proposals from the Biden Administration, including details of “The American Families Plan”, which is directed at individual level taxation. Numerous proposals to substantially increase income taxation are on the table and warrant the serious attention of our clients.

- The table on the following page summarizes six of the proposed changes to illustrate the significance of these potential tax increases. Depending upon what changes actually become law, advanced tax planning tactics to legally minimize such taxation exposure will be more prudent and important than ever.

- Anticipating this possibility, for the last 24-months we have engaged in adding a variety of advanced tax planning and management capabilities to our already strong line-up. All are designed to help us and our clients navigate the more challenging tax code landscape ahead.

- For instance, adding Separately Managed Accounts (SMA’s) that employ our desired factor tilts and potentially provide significant tax alpha benefits, via sophisticated tax-sensitive trading techniques, is a strategy we have proactively implemented with our clients with the highest taxation exposure.

- Depending on which changes become law, a variety of portfolio management, retirement planning, estate planning and tax planning adjustments may be in order.

- As always, upcoming Semi-Annual Clarity Sessions with clients will include discussions related to additional tactic we think you should consider implementing and we encourage you also to be in touch with your estate planning counsel, business legal counsel, tax lawyer and CPA.

- Given political negotiations, pundits, and press conferences, all covered by cable news 24/7, it is always a bit challenging avoiding overreacting or underreacting to such alerts. We are engaged with numerous advanced sources of intelligence and analysis on the matter and are happy to conduct a consultation with you. Simply email or call us and we will set up a time to specifically discuss these matters with you.

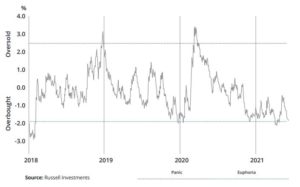

Chart of The Month

We are Keeping Our Eye on Investor Sentiment

The above chart is a contrarian indicator that measures investor sentiment. As you can see, sentiment is near overbought levels but not yet signaling dangerous levels of euphoria like we experienced in 2018. Margin debt is at record highs and up 58% from 15 months ago, supporting the excess optimism currently in the markets. This is an indicator we will continue to monitor and supports our portfolios being underweight risk (beta) in certain asset classes.

Janiczek Wealth Management – At a Glance

To learn more about Janiczek Wealth Management, click here.

Important Disclosures

The content herein is to be used for informational purposes only. Neither Janiczek Wealth Management or its owners and employees represent or warrant the accuracy or completeness of the information contained in this report. In no event will Janiczek Wealth Management or its owners or employees be liable for any damages that may result from the use of or reliance

on these materials.

Past performance may not be indicative of future results. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy (including the investments and/or investment strategies recommended and/or undertaken by Janiczek® Wealth Management (“Janiczek®”), or any non-investment related services, will be profitable, equal any historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Janiczek® is neither a law firm nor accounting firm, and no portion of its services should be construed as legal or accounting advice. Moreover, you should not assume that any discussion or information contained in this document serves as the receipt of, or as a substitute for, personalized investment advice from Janiczek®. Please remember that it remains your responsibility to advise Janiczek®, in writing,

if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/ evaluating/ revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. A copy of our current written disclosure Brochure discussing our advisory services and fees is available upon request. The scope of the services to be provided depends upon the needs of the client and the terms of the engagement.

TM & Copyright Janiczek Wealth Management. All rights reserved. Do not reproduce or redistribute in any form without prior written permission. Strength Based Wealth Management® 35 Essential Strengths®, The Stages of Financial Freedom®, Wealth Optimization Plan™, Wealth Optimization Dashboard™, Lifestyle Protection Analysis™, Elastic Limit Wealth Threshold™, Flourish! Activators™, FLOURISH!™ and Flourish! Based Retirement Planning™ are all trademarks of Wealth with Ease, LLC. For details, call 303-721-7000.