April 2021

Investment Conditions & Outlook

Executive Summary

It has been wonderful to see the green shoots of spring begin over the past few weeks. It is equally exciting to see glimpses of normalcy in our lives as well. As vaccines continue to roll out, we expect to see the restrictions lift and life go on post pandemic in some hybrid (part past normal, part new normal) ways.

There are two main themes for the continued momentum in the stock market: stimulus and vaccines.

The larger than expected stimulus packages ($900B and $1.9T) equate to nearly 14% of GDP. This fiscal spending has been unprecedented and larger than what the markets had priced in at the beginning of the year. Combine this with faster than expected progress with vaccine roll-outs and it sets the tone for a faster and better recovery. The largest vaccine rollout in history is underway and almost 600M doses have been administered worldwide. This has provided the public with the confidence to begin getting back to their normal lives, which is benefiting the economy. Americans are increasing spending on in-person services, such as restaurants, gyms and hotels, sectors heavily battered by trends and restrictions during the pandemic.

As policymaker’s attention shifts from the pandemic to long-term priorities, we will likely see tax legislation to increase government revenue. We expect to see the corporate tax rate increase to 28% as well as proposals to increase taxes on high and ultra-high net worth taxpayers. We will continue to monitor these developments and our proactive efforts to pursue tax smart tactics and strategies continues to add value to clients.

We are honored to be of service to you and look forward to seeing more of you in person in the weeks and months ahead.

The Janiczek Team

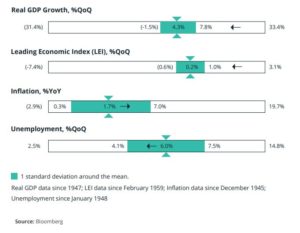

Economic Conditions and Key Takeaways

Key points

- The recovery from the COVID shock has been faster than expected, with consumer confidence holding up well aided by massive fiscal support.

- Real GDP growth will get a further boost from the continued strength in the housing market supported by low inventories and borrowing costs.

- Higher employment and labor market participation translated into broad-based declines in unemployment rates, but labor market remains far from Fed’s goal of full employment.

- We expect core inflation to trend downwards over the course of the year, as inflation lags GDP growth by a few quarters, but we introduced TIPs to our portfolios to hedge against uptick.

- The U.S. looks primed for growth as economy reopens with pent up demand driving a bounce in service sectors and real GDP growth of around 7%.

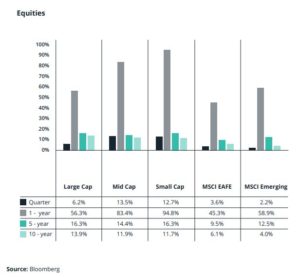

Equity Performance and Top Takeaways

Key points

- Strong quarter for global equity markets posting positive performance and strong rolling one-year returns.

- International markets underperformed U.S. markets during the first quarter with returns facing translation headwinds due to stronger U.S. dollar.

- With increased expectation for a strong economic resurgence for remainder of year, U.S. equity markets look fair to slightly overvalued.

- Value stocks outperformed in the first quarter and remain undervalued relative growth stocks.

- Cyclicals, mainly energy, surged in the first quarter and still look attractively valued.

- We give cyclical stocks the advantage for the moment, while remaining watchful for signs of a cycle transition as recovery moves forward.

- Emerging markets, mainly China, had an early exit from lockdowns and stimulus measures should benefit EM more broadly, as will recovery in global demand.

- Global equity recession indicators show minimal risk of recession.

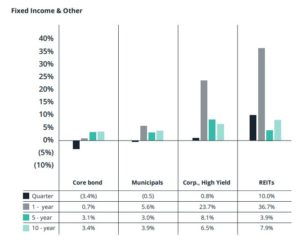

Fixed Income Performance and Key Takeaways

Key Points

- Bond markets greeted the vaccine rollout with higher bond yields, anticipating a move by the fed to tighten monetary policy.

- This resulted in a tough quarter for bonds as it experienced price volatility due to steepening yield curve.

- Longer duration core bonds lagged while municipals fared better, and credit led the way.

- We believe the rise of rates is premature and see Fed holding rates until at least 2023.

- Expanded Fed support for credit markets has reduced tail risk, but higher and rising debt loads could lead to sweeping defaults and downgrades.

- With Fed set to stay course at lower rates, treasury yields at the front and belly of yield curve will remain low.

- Stocks will react to interest rate increases as it impacts valuations, but the low yields on bonds have us continuing to favor equities.

Wealth & Tax Management Talking Points

- Our Semi-annual Clarity Sessions with clients, a very important part of our wealth, tax and portfolio management services, are going strong and keeping clients aligned with best practices, time-sensitive tweaks and the proprietary standards of excellence of our patented system. Our 2021 Clarity Session Agenda is receiving rave reviews (average rating of 9.86 out of 10 from clients). We look forward to our next clarity session with you and have a number of items on our checklist to keep you confident, optimal and on track.

- Be sure to update us on any/all trusted advisors on your team. We regularly coordinate tax, estate, asset protection, employee benefit, stock option and private investment strategies with additional trusted advisors on a client’s team. Your CPA, estate attorney, insurance agent(s), mortgage broker, banker and, in some cases, business CFO, business manager, and employee benefit department are all specialists we are equipped to collaborate with, on your behalf, to maximize your results. Let’s discuss this next time we meet.

- We are carefully monitoring tax code legislation and the best tax planning strategies and tactics to employ to legally minimize income and estate taxation. “Tax Alpha” is an important outcome to pursue and recent developments and efficiencies in portfolio management and wealth management are allowing more individuals to benefit by such advanced techniques. We will discuss this the next time we meet.

- Janiczek Wealth Management is named to Barron’s Top Advisor list for 2021, 2020, 2019, 2018, 2017, 2016, 2015 and 2014. That’s 8-years in a row! We love what we do and are honored to be recognized in this way. Yes, we are accepting new clients – and introductions from clients is our number one source of new clients. When you introduce us to a colleague, friend or family member, simply include us in the email and Cathy Wegner, our Director of New Client Engagements (cathy@janiczek.com), will confidentially begin the conversation to see if/how we can be of service to them. Thank you all for your kind support and thoughtful introductions!

Evidence Based Investing Chart of the Month

Value Stocks Are Outperforming Growth Stocks Thusfar in 2021

Growth stocks, which have been the hot trade for the last 10 years, have started to lose some steam. During the first quarter of 2021we have seen some rotation into value sectors with value outperforming growth across all size categories. We see continued opportunities for value stocks as the economy continues to rebound. We were overweight growth for most of 2020 and have since removed the overweight to redeploy assets into value sectors.

Janiczek Wealth Management – At a Glance

To learn more about Janiczek Wealth Management, click here.

Important Disclosures

The content herein is to be used for informational purposes only. Neither Janiczek Wealth Management or its owners and employees represent or warrant the accuracy or completeness of the information contained in this report. In no event will Janiczek Wealth Management or its owners or employees be liable for any damages that may result from the use of or reliance

on these materials.

Past performance may not be indicative of future results. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy (including the investments and/or investment strategies recommended and/or undertaken by Janiczek® Wealth Management (“Janiczek®”), or any non-investment related services, will be profitable, equal any historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Janiczek® is neither a law firm nor accounting firm, and no portion of its services should be construed as legal or accounting advice. Moreover, you should not assume that any discussion or information contained in this document serves as the receipt of, or as a substitute for, personalized investment advice from Janiczek®. Please remember that it remains your responsibility to advise Janiczek®, in writing,

if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/ evaluating/ revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. A copy of our current written disclosure Brochure discussing our advisory services and fees is available upon request. The scope of the services to be provided depends upon the needs of the client and the terms of the engagement.

TM & Copyright Janiczek Wealth Management. All rights reserved. Do not reproduce or redistribute in any form without prior written permission. Strength Based Wealth Management® 35 Essential Strengths®, The Stages of Financial Freedom®, Wealth Optimization Plan™, Wealth Optimization Dashboard™, Lifestyle Protection Analysis™, Elastic Limit Wealth Threshold™, Flourish! Activators™, FLOURISH!™ and Flourish! Based Retirement Planning™ are all trademarks of Wealth with Ease, LLC. For details, call 303-721-7000.