January 2021

Investment Conditions & Outlook

Executive Summary

2020 was a year replete with change, challenge, threat and opportunity as all of us needed to quickly respond to the implications of a worldwide pandemic. Our thoughts and prayers go out to everyone, especially those who experienced the most severe levels of hardship, loss or isolation.

As strange as it was, 2020 revealed the strength, resilience and resolve of the human race and the highly functioning infrastructures, resources and systems there to help us all adapt as well as we could. Economically the world witnessed the shortest recession on record followed by the fastest economic recovery on record.

Our longstanding themes of investing from a position of strength, expect the unexpected, focus on quality and value opportunities, and lever collaborative talent and technology helped us, and our clients navigate the year extremely well.

In the pages ahead, you’ll see our list of both headwinds and tailwinds that will likely be influencing the financial markets in the year ahead. While we have plenty of concerns, compelling signs of continued economic recovery, pent up demand, cash on the sidelines, additional stimulus and, most important of all, the promise of vaccine success can fuel robust economic growth worldwide in 2021.

We provide clarity and insight into the current investment landscape – strengths, weaknesses, opportunities, and threats – and encourage clients to continue to maximize the benefit gained from all six integrated components of our Complete Wealth Solution.

The Janiczek Team

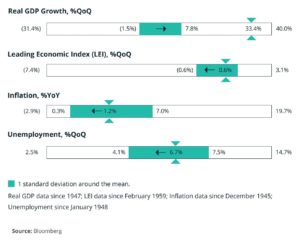

Economic Conditions and Key Takeaways

Key points

- Global macroeconomic conditions continued to improve for the quarter while the Fed and fiscal policy support resulted in further recovery of asset prices, some to new all-time highs.

- We saw record monetary policy relief from the Fed in response to the pandemic fueled recession. Our investment rule of “don’t fight the Fed” helped us stay the course and avoid poor market timing decisions.

- The Federal Government followed suit with the CARES act, injecting trillions of dollars into the U.S. economy, helping to further reduce unemployment levels.

- We have not seen all the liquidity flow through to the capital markets yet. This is a continued positive sign for the private sector and stocks.

- Current debt loads and older demographics should result in minimal inflationary pressure.

- Worldwide GDP growth of 5.8% and 4.6% GDP growth in the U.S. is a good possibility for 2021.

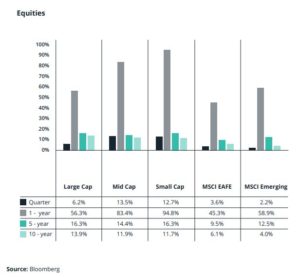

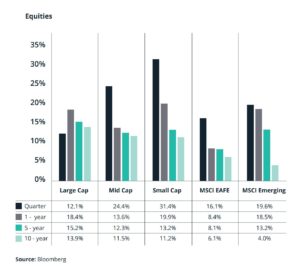

Equity Performance and Top Takeaways

Key points

- Strong quarter for global equity markets posting positive performance and strong rolling one-year returns.

- International markets underperformed U.S. markets during the first quarter with returns facing translation headwinds due to stronger U.S. dollar.

- With increased expectation for a strong economic resurgence for remainder of year, U.S. equity markets look fair to slightly overvalued.

- Value stocks outperformed in the first quarter and remain undervalued relative growth stocks.

- Cyclicals, mainly energy, surged in the first quarter and still look attractively valued.

- We give cyclical stocks the advantage for the moment, while remaining watchful for signs of a cycle transition as recovery moves forward.

- Emerging markets, mainly China, had an early exit from lockdowns and stimulus measures should benefit EM more broadly, as will recovery in global demand.

- Global equity recession indicators show minimal risk of recession.

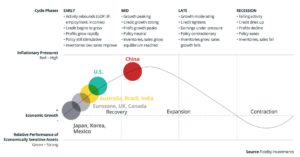

Business Cycle Framework and Top Takeaways

Key Points

- Most developed economies have exited brief but sharp recessions and have generally made improvements since peak of global pandemic.

- China is ahead of most other economies due to quicker emergence from lockdowns and recovery in global manufacturing.

- U.S. is still in early-cycle recovery phase, with room to progress to mid-cycle.

- Although economic activity remains below 2019 levels, the prospect of vaccine related successes (economic openings) over the second half of the year and beyond, keeps us bullish on the continued economic expansion in 2021.

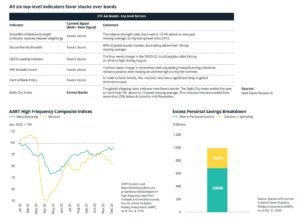

Rally Watch Indicators are Bullish (favor stocks)

Key Points

- All six of our top-level indicators favor stocks over bonds.

- Any new U.S. restrictions should be on the lighter end, like those taken in Europe, resulting in stalling rather than severe reversal of economic momentum.

- Service activity has slowed with new expanding virus fears, but manufacturing remains strong.

- U.S. consumer is better positioned to weather near-term economic lull due to approximate $1 trillion of excess savings built up over past few months.

- The aggregate savings cushion is the result of reduced spending and massive government stimulus during peak pandemic.

- This sidelined cash represents pent up demand that should help to drive equity prices during 2021.

Equity Performance and Top Takeaways

Key Points

- The final quarter of the year saw continued strength in global equity markets with cyclical stocks, like small caps, leading the charge.

- As a result of the pandemic, households are holding record levels of cash, and money is ready to be spent. A post pandemic economy could feel the wave of pent-up consumption spending that would be positive for stocks.

- 2020 saw rapid adoption of many new technology services. Some of these technological trends were already underway, but the pandemic served as a catalyst propelling them into the mainstream and we expect this momentum to continue in the new year.

- International equites continue to remain favorable with 20-30% lower valuations when compared to domestic counterparts.

- Given lower range bound yield expectations, global equities should continue to outperform bonds and cash.

- Accommodative monetary policy leading to dollar weakness could continue to benefit international stocks.

- Reopening economies should continue to benefit our allocations to cyclical value and small caps stocks as fundamentals continue to improve.

- Mid-cycle recovery phase historically has been positive for stocks but carries more frequent equity corrections and heightened volatility. Be mentally and financially prepared for ups and downs.

- FactSet, a data and financial solutions provider, expects year over year earnings growth in all 11 S&P sectors, helping to reduce current inflated valuation metrics.

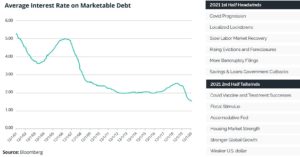

Fixed Income Performance and Top Takeaways

Key points

- Rallying global stocks and improving economic conditions resulted in yield curves moving up during the quarter keeping core bond performance range bound, but remaining strong for the last year.

- Credit continued its impressive run from the March lows as default risk continues to decline.

- We expect to continue the reality of lower rates for a longer period, not great news for savers (and/or conservative investors), but good for equity investors.

- Interest rates anchored at historic lows tend to push investors further out on the yield curve in search of yield (an investment mistake for many), something our portfolios avoid.

- Rebounding global equity markets should cause yields across the curve to rise making TIPS (inflation protected) a likely addition to our fixed income allocation in Q1 or Q2.

- The continued economic recovery should support lower quality credit, a potential positive for those looking to maximize yields without elevating credit default risks.

- We will continue to own fixed income – not as a source of outsized returns – but as a vehicle to reduce overall portfolio volatility (our fixed income holdings performed very well during pandemic selloff in March and all year long). We will continue to remain positioned under benchmark duration and overweight investment grade corporates and municipal bonds. This said, underweighting fixed income and/or utilizing alternatives is also on the table.

Headwinds and Tailwinds that Balance-out Our Thinking

Key Points

- Another factor that could continue to weigh on the markets is current and continued deficit funding.

- Thus far demand remains strong for U.S. Treasury supply being quickly purchased, but this might not always be the case.

- Buyers may require higher yields to absorb the massive debt supply, increasing the cost for the Government to finance the large and growing deficit.

- The longer the Fed can keep rates at depressed levels, the greater the benefit for the Government to absorb the cost of deficit spending.

- For the better part of 2021, the U.S. economy will remain under the cloud of the Covid-19 virus. Amid greater than normal economic and political uncertainty, our base case scenario calls for first-half headwinds and second-half tailwinds. Add it all up and a 4.6% real GDP growth case is quite possible. While certain highly impacted industries and individuals remain vulnerable, the resilience and improved leanness and profitability of others is a powerful force.

- Increases in tax rates, regulations or other political oriented changes can influence market valuation metrics. Similarly, economic stimulus items can also influence markets and industries. Given recent election results, we have or will add more infrastructure holdings to some portfolios.

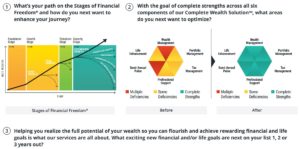

Wealth & Tax Management Upgrades to Consider in 2021

- We regularly upgrade all six components of our Complete Wealth Solution. Helping you realize the full potential of your wealth so you can flourish and achieve rewarding financial and life goals is what our services are all about. Transformed 1) wealth management, 2) investment management, 3) tax management, 4) professional support, 5) semi-annual pulsing and 6) life enhancement – all in a fraction of the time otherwise required – is the “impact goal” of our unique client experience and patented system. We encourage all clients to fully engage the everexpanding features of this robust system in 2021.

- Mortgage rates remain at historic low levels. We continue to assist and encourage our clients to refinance real estate debt, effectively locking in better terms and a lower interest rate (in many cases a reduction of 1% or more) compared to previous low loan rates. This is allowing us to help clients save thousands of dollars in interest costs over the life of the loan, while improving non-discretionary expense ratios and debt to equity ratios to well within our standards. Now is a great time to review your existing debts to see if a better option exists before interest rates head higher.

- Advanced Tax Planning and Tax Alpha Portfolio Management continues to be an expanding value-added part of our Complete Wealth Solution. We have invested significant sums in the latest technologies and techniques for reducing taxation. Savings of tens and even hundreds of thousands of dollars a year are possible. Be sure to discuss these services and techniques with us in your next Semi-annual Clarity session.

- Required Minimum Distributions (RMDs) have been reinstated for 2021. We have received several inquiries about whether the Federal Government will extend this CARES Act law into 2021, allowing individuals to forego taking RMDs for a second consecutive year if they do not need the distribution. As of now, there are no concrete indications of this happening again, but we will be monitoring closely and will act quickly should this become an opportunity to take advantage of for our clients. In 2020, we helped many clients reduce their tax liability by utilizing this special tax code.

- Consider creative estate and wealth transfer strategies in 2021. There are concerns regarding future legislative changes having a negative impact on one’s wealth, which could include lowering the gift and estate tax exemption limits (currently set at $11.7 million per taxpayer in 2021). A thoughtful strategy being implemented considering this concern is known as a Swap Power for Basis Management. This technique relates to a donor who has gifted or transferred assets such as property or investment accounts into an irrevocable trust (which does not receive a step-up in income tax basis at the donor’s death). Exercising the swap power allows the donor to exchange low-basis assets in an existing irrevocable trust for high-basis assets held in the donor’s estate for estate tax purposes. At the donor’s death, the low basis assets are positioned outside of the irrevocable trust and receive a “step-up” in basis to ultimately reduce or eliminate capital gains taxes that would have been triggered. Just one of many creative techniques at your and our disposal. Our team will continue to work proactively and collaboratively with you and your other trusted advisors to identify and implement the best possible strategies.

Janiczek Wealth Management – At a Glance

To learn more about Janiczek Wealth Management, click here.

Important Disclosures

The content herein is to be used for informational purposes only. Neither Janiczek Wealth Management or its owners and employees represent or warrant the accuracy or completeness of the information contained in this report. In no event will Janiczek Wealth Management or its owners or employees be liable for any damages that may result from the use of or reliance

on these materials.

Past performance may not be indicative of future results. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy (including the investments and/or investment strategies recommended and/or undertaken by Janiczek® Wealth Management (“Janiczek®”), or any non-investment related services, will be profitable, equal any historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Janiczek® is neither a law firm nor accounting firm, and no portion of its services should be construed as legal or accounting advice. Moreover, you should not assume that any discussion or information contained in this document serves as the receipt of, or as a substitute for, personalized investment advice from Janiczek®. Please remember that it remains your responsibility to advise Janiczek®, in writing,

if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/ evaluating/ revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. A copy of our current written disclosure Brochure discussing our advisory services and fees is available upon request. The scope of the services to be provided depends upon the needs of the client and the terms of the engagement.

TM & Copyright Janiczek Wealth Management. All rights reserved. Do not reproduce or redistribute in any form without prior written permission. Strength Based Wealth Management® 35 Essential Strengths®, The Stages of Financial Freedom®, Wealth Optimization Plan™, Wealth Optimization Dashboard™, Lifestyle Protection Analysis™, Elastic Limit Wealth Threshold™, Flourish! Activators™, FLOURISH!™ and Flourish! Based Retirement Planning™ are all trademarks of Wealth with Ease, LLC. For details, call 303-721-7000.