January 2024

Investment Conditions & Outlook

Executive Summary

We started 2023 with low and declining expectations for global growth as we navigated through the most extensive interest rate hike in decades, major geopolitical issues, and a regional banking crisis. However, China’s reopening and the strength of the U.S. consumer helped to stabilize growth. As the year proceeded and a buoyant economy kept equity markets afloat, investors could only hope for the elusive Santa Claus rally to end the year. Santa delivered the goods this Christmas, with the markets ending the year on a new recovery high and sitting within striking distance of the all-time high the S&P set in January of 2022. At the same time, most of the year can be characterized by narrow leadership in a handful of expensive mega-cap stocks. We remained disciplined in our approach to better valuations and stronger companies, resulting in portfolios being rewarded with strong returns over the year’s final quarter. We believe 2024 will be less about the artificial intelligence (AI) creators and more about the AI adopters across all sectors as companies focus on productivity-enhancing AI investments.

November marked the turning point when investors began to gain confidence that the Fed had finished hiking rates, and the economic backdrop began to look like the Fed could move to a less restrictive policy at some point in 2024. With inflation steadily improving from the June 2022 peak, the Fed should be able to give back some of the hikes and be less restrictive moving forward. On paper, it makes sense, but we do not know the speed or timing at which these cuts will happen. With earnings contractions mainly behind us, it would look like the bull market has legs to continue in 2024, with a broader range of stocks able to continue their advance.

While investor confidence remains strong, 2024 presents a variety of macro crosscurrents that could move markets in different directions. The first half of the year could see higher volatility as the ability for a recession continues to linger and we head into an uncertain election. We continue to monitor two main issues as we proceed in the new year. The first is the continued pressure from higher rates on credit cards, auto delinquencies, and commercial real estate. Until the Fed begins relieving the stress, the strain on GDP could continue. While rate cuts make sense, a hawkish surprise could cause further stress on the economy. The second is that markets have already priced in a soft landing supported by strong asset class returns in Q4. This could leave little room for further gains come the new year. We did not see stocks get any cheaper in 2023 and strong fundamental analysis continues to be imperative.

While any market outlook is just that, an outlook, we will remain steadfast in owning a balanced mix of stocks and bonds, plus a few alternatives. We know the consensus on Wall Street is often wrong and evidence from 2023 does little to dispel that notion. What we know in the year ahead is markets will be somewhere in between the mother of all rallies or a selloff for the ages. While we do not expect to see the same returns experienced in 2023, we remain optimistic that the broader market sectors can continue to add positive attribution to portfolios in the new year.

The Janiczek Team

Economic Conditions and Key Takeaways

On the back of a strong 2023, the U.S. economy remains in positive growth territory, but will this continue into 2024?

- Slowing job growth and declining inflation show that the economy continues to cool and supports a less restrictive view from the Fed moving forward.

- However, we are entering heightened uncertainty as investors debate whether a recession will be avoided or if we will stay on a path to a mild recession later in the year.

- Economic growth looks to further decline as the weight of higher rates continues to take their toll with expectation of future rate cuts to begin a steady expansion thereafter.

- The U.S. dollar could weaken early in the year on soft landing hopes (tailwind for international equities); however, it could strengthen later in the year if recession fears materialize.

- Investors piled into cash in 2023, taking advantage of decade-high yields, resulting in significant cash sitting on the sidelines that can be deployed back to markets.

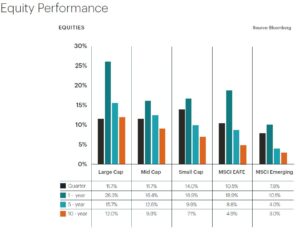

Equity Performance and Key Takeaways

The historic performance of the Magnificent Seven covered up the more muted returns across the investment landscape.

- Small cap stocks continue to trade at significant discounts to both large and mid-cap stocks making them an attractive portfolio holding heading into 2024.

- Within U.S. equities we are tilted towards small cap, dividend payers and companies with lower valuation multiples.

- Outside of the U.S., the outlook for developed markets is optimistic, given significant valuation support and favorable sector compositions.

- Total returns could be range-bound due to expensive valuations (mainly in U.S. markets).

- The widening of earnings per share gains should continue to support a broadening of equity performance in 2024.

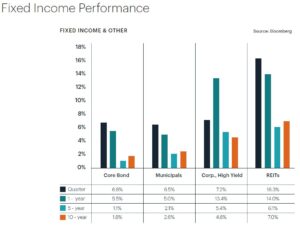

Fixed Income Performance & Key Takeaways

- Fixed income markets will have to adjust for the reality of higher for longer in rates and the potential widening of credit spreads if a recession does become a reality.

- Regardless of a soft landing or a recession, rates will come down in the future resulting in positive performance from duration management.

- Continue to favor a higher quality and lower duration portfolio as one additional rate hike is expected later this year.

- A looming recession could be a headwind to below investment grade debt, a sector we continue to leave out of our core fixed income portfolio.

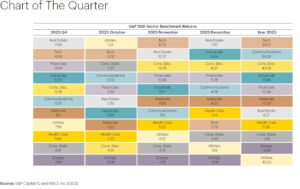

Chart of The Quarter

Leadership broadened in U.S. markets in the fourth quarter with real estate and value sectors outperforming. We saw higher than average return dispersion with technology up over 50% and utilities and energy both declining. The gap between the top performing and the worst performing sector was 69%, the eighth highest since 1973. This sets up 2024 nicely for a leadership change

and lower valued sectors continuing their resurgence.

Wealth & Tax Management Key Takeaways

As we embark on a New Year, it’s a healthy exercise to take a step back from the technical aspects of prudent financial management to evaluate “what is the purpose of my wealth?” Far too many well-intentioned affluent individuals spend a lifetime working hard, saving, living under their means, worrying about doing all the right things, only to die with more money in their accounts than they’ve ever had in their lifetime. Had they known this, they may have done things differently along the way, like:

• working less

• retiring earlier

• spending more

• worrying less

• gifting more to family and/or friends

• gifting more to charity

Lacking the clarity, confidence, and systems to take such actions during their lifetime, they may have unknowingly missed an opportunity to maximize their wealth’s full potential and thus, missed an opportunity to enrich their life and truly flourish with their wealth.

As your trusted partner on this journey, we’re here to help you maximize your wealth’s full potential, as defined by you, both during your life and at your death. We aim to integrate the thought-provoking question above with objective lifestyle protection and financial planning standards of excellence, keeping you safe, while helping you unlock your wealth’s full potential. We’ll be addressing this rich topic in upcoming client Clarity Sessions as appropriate.

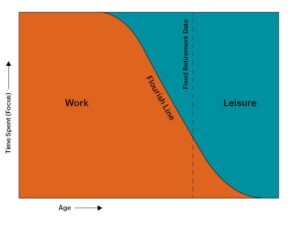

Wealth and Tax Management Chart of the Quarter

Keeping with the theme above, this quarter’s chart depicts the typical journey through work and life, challenging common ideas around “retiring.” Traditionally, a retirement date is seen as some fixed date/target (the dashed line), and we spend the great majority of our time working (orange shaded area) until we reach this date/target, and then we shift to a majority of our time not working (leisure time, blue shaded area) after the dashed line. Unfortunately, most of us have no idea how much time we have remaining after the dashed line. Thus, we propose a more dynamic vision of “retirement,” the “Flourish Line,” with the aim being to give clients the clarity and confidence to modify their work pace and find more of a work/leisure balance sooner rather than later.

The Janiczek Story

To learn more about Janiczek Wealth Management, click here.

Find Important Disclosures here.