“Since the profits that companies can earn are finite, the price that investors should be willing to pay for stocks must also be finite.”

-Benjamin Graham, The Intelligent Investor

As various vulnerabilities lurk over the economy (inflationary pressures and the Fed’s reaction to such pressures, predictions of a recession, and continued geopolitical tensions), investors are experiencing what can be significant daily price fluctuations in the stock market. Under challenging markets like these, valuation metrics can serve as a silver lining as we look forward to the following years and decades. What do current valuations tell us about the long-run return expectations?

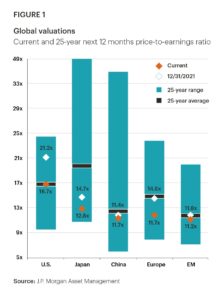

Before 2022, equities were widely viewed as overpriced across the board. With the declines in equity prices year-to-date, we have now reached a level where expected future returns are becoming more compelling. As seen in Figure 1, global valuations are at or below their 25-year average as measured by the next twelve-month (NTM) price-to-earnings (P/E) ratio.

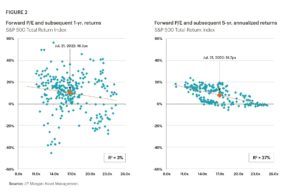

It is important to understand why valuations are relevant. In short, valuation metrics are a powerful instrument available to investors for assessing the attractiveness of the stock market at any given point in time. They help us predict what returns we may expect in the future if we buy a stock or stocks now at a given price. This prediction of expected future returns over longer time periods (5+ years) is much more accurate than over shorter time periods (1 year or less). See the wide dispersion of return dots in the graph on the left in Figure 2, versus the tight correlation of dots on the right graph. Using the right graph, we see that the S&P 500 had a forward looking P/E ratio of 16.7 on July 21, 2022, meaning we could predict annualized returns of approximately 8% in the five years ahead. The lower the forward looking P/E ratio, the higher the expected returns in the years ahead over a longer time period. So the fact that U.S P/E ratios have dropped rather significantly in the first half of 2022 is good news for us as long term investors deploying cash in our portfolios.

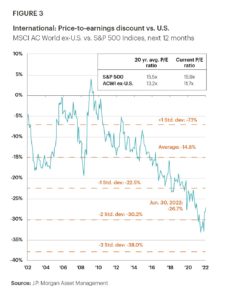

While P/E ratios in the U.S. are important, as globally diversified allocators, we must also look at valuations internationally, especially how they compare to the US markets. Figure 3 indicates that the rest of the world, excluding the US, is trading at a significant discount to US markets. Of course, this discount adequately reflects the looming risks overseas such as the war in Ukraine and its impact on rising energy and food prices.

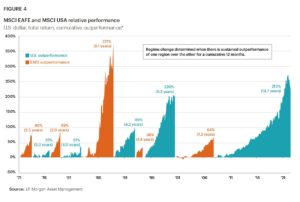

Looking ahead, these discounts appear attractive and may provide new opportunities. Home country bias (an investor’s preference for companies based in their home country over those abroad) has benefited U.S. investors in recent years. This hasn’t always been true. Figure 4 illustrates the time periods when international equities have outperformed U.S. equities.

What does all of this mean for investors? Global equities are starting to look more attractive from a valuation standpoint, with equities outside the U.S. selling at a significant discount relative to U.S. equities. This doesn’t mean investors should make huge tactical bets based on these valuations, especially given some of the worldwide risks that have caused the year-to-date sell off in global equity markets. However, investors can use this valuation evidence to adjust their asset allocation targets accordingly given their personalized risk tolerance to take advantage of potential opportunities that may exist today.

It is more important than ever for investors to maintain a long-term view for their portfolio, and employ a systematic, disciplined approach to portfolio construction and maintenance, centered around valuation metrics and evidence, not a sporadic approach based on hunches, headlines, or emotions. At Janiczek Wealth Management, we are guided by such a disciplined and systematic approach, as well as a belief in global diversification with tilts toward companies with attractive valuations, and stable fundamentals such as robust free cashflow and strong balance sheets.

If you are interested in escaping the headline noise, hype, and complexity of navigating today’s equity markets, we are happy to help you. If you are interested in a second opinion on your portfolio and overall financial picture, please contact Cathy Wegner, Director of New Client Engagements, 303-339-4480 or cwegner@janiczek.com.