Asset Allocation

No single input is more important to a portfolio’s success than asset allocation, or determining how much to allocate to various asset classes.

In 1986, authors Gary Brinson, Gilbert Beebower, and Randolph Hood conducted an in-depth study of the various sources of investment returns. Specifically, they analyzed quarterly returns from 1974-1983 for the 91 largest pension funds, and determined that 93.6% of the returns generated were a result of asset allocation.

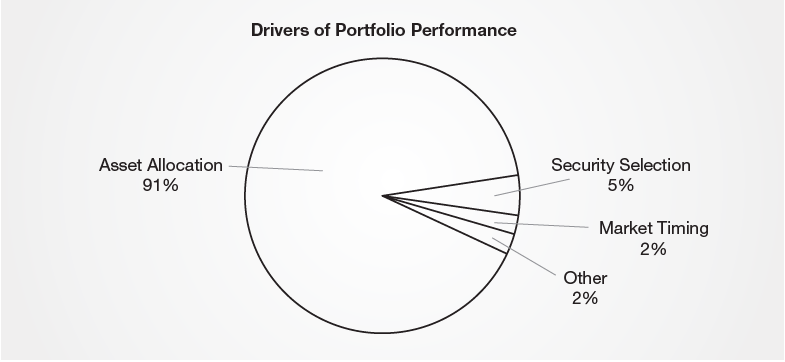

In a follow-on study in 1991, the authors concluded that 91% of portfolio returns are determined by asset allocation.

Source: 1991 Beebower Brinson and Singer

Modern Portfolio Theory

This was not the first time that the research highlighted the importance of asset classes in determining investment performance. Decades earlier, Harry Markowitz’s 1952 journal article, “Portfolio Selection,” introduced Modern Portfolio Theory (MPT) to the financial community. MPT provided investors with a methodology for building portfolios that would maximize expected returns though proper diversification. Markowitz showed that combining different assets, whose expected returns are not correlated (such as stocks and bonds), achieved a higher overall return for the portfolio.

The benefit of balancing diversified assets within a portfolio is a result of the interaction between the two asset classes. Stocks and bonds are negatively correlated, in that their returns tend to move in opposing directions. Stocks have greater returns but greater risks. Bonds rarely generate negative returns, but they will lag stocks when stocks are experiencing strong returns. When stocks decline, bonds benefit the portfolio by providing positive returns while simultaneously reducing portfolio volatility.

The chart below shows how an all-stock allocation has historically produced a rolling 3-year return of 12.7%, which diminishes to 10.7% when bonds are added, a 14% reduction. More importantly, this diversified stock/bond portfolio results in volatility declining 33% (from 9.4% to 6.3%). The risk reduction gained in the portfolio is more than twice the performance lost, an attractive trade-off compared to the original all-stock portfolio. (Source: Janiczek & Company Ltd., analysis of Bloomberg data, 2014)

The rise of alternative investments

In recent years, a third asset class has become more commonly added to the traditional portfolio containing stocks, bonds and cash. Alternative investments are those that exhibit risk and returns that do not behave like a stock or a bond. Examples include assets (commodities, real estate, private equity, fine art) or strategies (long/short, short-selling, event-driven, leveraged.) By adding this third leg to the asset allocation stool, an investor can further improve the risk-reward trade-off.

The impact of alternatives at various allocations can affect a portfolio’s risk and return, as illustrated by the graph below:

Source: BlackRock

KEY INSIGHT #1: A properly constructed and managed asset allocation is proven to enhance the risk/reward characteristics of a portfolio and is far more influential on performance than security selection and market timing by a factor of 9 to 1.

This article is adapted from “Evidence Based Investing for High & Ultra-High Net Worth Investors,” a white paper published by Janiczek & Company, Ltd. The full paper is available here.