Understanding the context behind the Federal Open Market Committee’s (FOMC or simply Fed) announcement

The Federal Open Market Committee (FOMC/Fed) swiftly dropped short-term interest rates to zero in reaction to the economic shock of the COVID 19 pandemic in March 2020. It announced large-scale purchases of government, municipal, corporate, and mortgage bond securities. These policies attempted to increase liquidity, maintain price stability, and cut long-term interest rates.

In 2008, for example, the same type of “Quantitative Easing” was applied (QE1, QE2, and QE3). Then, in 2013, tapering was planned and conducted again, this time with a “tapering tantrum” that had a more significant influence on long-term interest rates than expected.

To avoid such a surprise, the FOMC declares its intentions early on. When the Fed believes the market can handle it, it follows a precisely planned procedure, interpreted as a strong show of economic strength.

The recent “tapering” announcement by the FOMC refers to the process of no longer making these purchases owing to better economic circumstances and the equilibrium of sellers and buyers of such assets in open markets.

Analyzing the FOMC’s announcement

Two words may summarize the FOMC’s statement: largely unchanged. These are the four key takeaways from the FOMC meeting in November.

- No Change to IOER / Discount Rate

- Formal Taper Announced

- Composition and Pace of Taper Announced

- Inflation Still Transitory

Markets rose due to what transpired at the FOMC meeting in November, which should not be surprising given that the tapering announcement was well anticipated. Markets do not respond well to surprises. The Fed’s message remained virtually intact, with two exceptions concentrating on tapering and inflation.

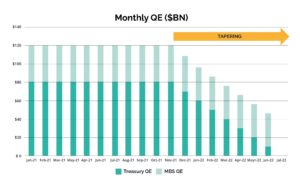

The FOMC said, as expected, that it will begin tapering its $120 billion in asset purchases in mid-November 2021, cutting purchases by $15 billion each month ($10 billion in Treasury’s and $5 billion in MBS). The Fed projects the program’s completion in mid-June 2022, pending any necessary revisions depending on the economic forecast.

In terms of inflation, the Fed indicated that it remains elevated, owing primarily to reasons projected to be transitory, most notably supply and demand imbalances in some sectors.

Furthermore, Jay Powell and the committee restated their intention to remain patient concerning interest rates. The Fed must first see maximum employment, which might occur in the second part of next year. Two rate rises are possible in 2022, consistent with market expectations, and nothing the Fed stated should cause substantial changes in market expectations.

Janiczek Wealth Management stays up to date on the newest news and developments, so our clients don’t have to worry about how these elements may affect their portfolio management. As always, for clients who want more than the CliffsNotes version, our investment team can discuss FOMC announcements and their ramifications in-depth during your next Clarity Session.