Until March of this year, there was not much chatter around inflation. It has been over 20 years since the U.S. has seen sustained inflation. However, the combination of massive stimulus package, supply chain disruption from COVID and pent-up consumer demand, inflation should not come as a surprise.

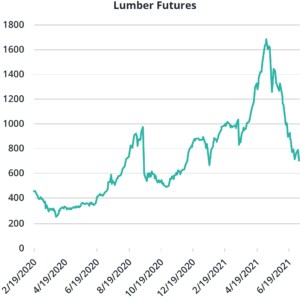

Everything from lumber to used cars have increased significantly this year (lumber futures currently experiencing steep declines in price). If you take a step back and look at why this is happening, one should conclude that these price increases are transitory and not sustainable for a long period of time. Lumber prices exploded with consumers upgrading their homes and lumber mills having to close during COVID. The shortage in semiconductor chips threw a wrench into many supply chains, causing a shortage of new vehicles and a rush to buy used cars.

Transitory inflation is not a huge threat to stocks or bonds. If you look at the bond market, it seems to agree. If inflation was going to be a going concern, yields should continue to push higher. Yes, we saw yields increase significantly, but they have dropped back to a more palatable range.

If we continue to take cues from the Fed, central bankers have made it clear that they will not be raising interest rates in response to temporary inflation. They will wait until unemployment comes down further before rate hikes that could slow the economy.

In conclusion, we feel supply chains will fully open at some point once consumers deplete stimulus checks and pent-up demand to spend. The current prices for most products and services are being compared to very low prices last year during the pandemic and prices should increase. We continue to remain diversified across asset classes and geographies. We own positions in TIPs (inflation protected securities) and short duration bonds, both will act as hedges to inflation.