July 2022

Investment Conditions & Outlook

Executive Summary

The global economy and stock market struggled in the first half of 2022. Facing multi-decade high inflation and aggressive monetary policy tightening by the Fed, investors across equity and bond positions felt the effects. The tides of investor concerns are shifting from inflation and the response by the Fed to the U.S. falling into a recession.

So far this year, we have seen record sell side volume and year-to-date returns that rank among historic lows. Markets seem to be trading on headlines and have dislocated from the underlying fundamentals. No question that economic growth is slowing from pandemic era stimulus, but a return to pre-Covid norms should be expected. The selloff has resulted in markets being extremely oversold, and history would suggest a rebound could be forthcoming. Overall, conditions could remain volatile, but we are cautiously optimistic investors could experience less pain and more gain for remainder of year.

The Fed has the not so simple task of taming inflation; at 40-year highs, they might have lost some credibility in the short term while engineering a “soft” economic landing. The Fed is forced to keep raising short-term interest rates to reduce overall demand and slow inflation. It sounds simple enough but finding the right balance between higher rates and keeping positive economic growth has historically been very challenging. If the Fed is too aggressive in combating inflation, the outcome could be a recession.

We regularly analyze a myriad of economic indicators to get a sense of where the economy could land in the coming months. We do not try to pretend we have a crystal ball but feel the risk of a recession in the short term is unlikely, but a mild recession is not out of the question. There are two primary reasons for this: the labor market remains strong, and a well-capitalized consumer with historically low debt-to-income ratios.

This is not a market that will reward lackadaisical “dip buying” or excessive risk-taking (look at the demise of cryptocurrencies). We will continue favoring companies with higher free cash flows, healthy balance sheets, and lower volatility. We still believe one’s circumstances and risk tolerance should determine your mix of investments, not media headlines. Being experienced investors involves having the fortitude and skill set to navigate such periods with poise, and this report is designed to help you maintain a preferred stance.

The Janiczek Team

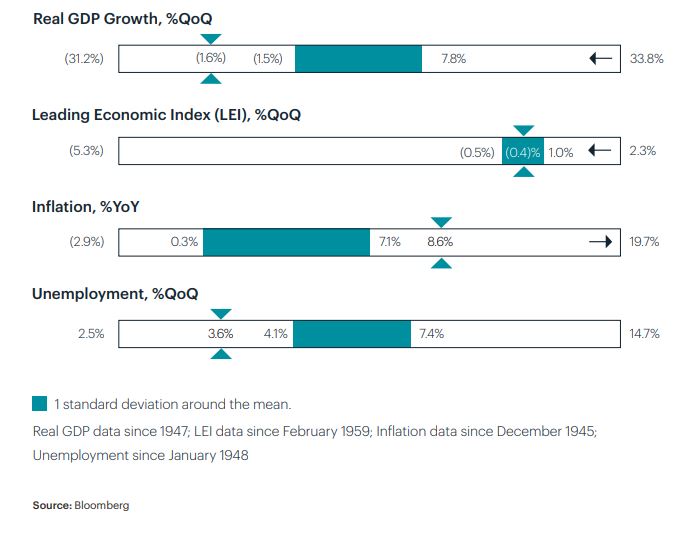

Economic Conditions and Key Takeaways

- Looking ahead, we see the ability for inflation to ease amid continued central bank tightening and slowing growth.

- Limited inventories of energy and a supply chain that is still working out the kinks will result in inflation remaining above average for the foreseeable future, but should start to retreat from record levels.

- Consumer spending remains strong, and with low unemployment and high job security, it can keep up with the current bout of higher inflation.

- Historically, with any Fed tightening cycles, the risk of a recession could increase, but markets and investors should anticipate changes by the Fed, eliminating the surprise factor.

- Corporate earnings remain a bright spot, but potential profit margin pressure exists with higher input costs and could lead to earnings downgrades.

- Unemployment remains low.

Economic Conditions

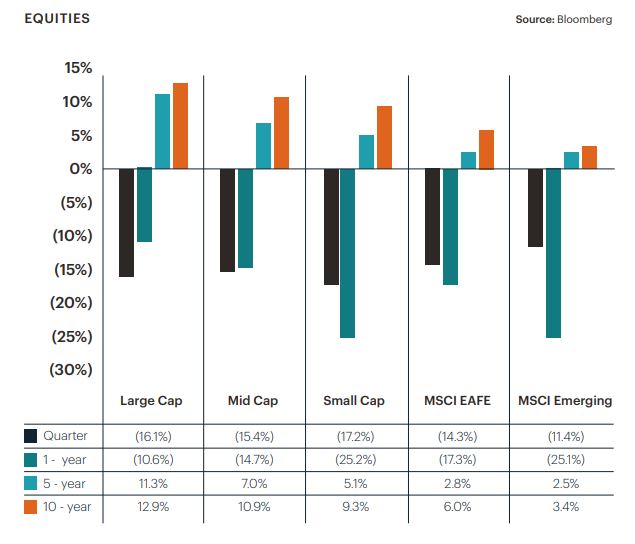

Equity Performance and Key Takeaways

- First half of the year was painful, with nearly all asset classes suffering losses and few places to hide.

- U.S. equities across the market capitalization spectrum are in correction or near bear market territory but moved modestly higher last week of May.

- Diversification remains key as correlations between equity asset classes sit at historic lows.

- A glimmer of hope is the reset in valuations and forward return opportunities, especially within small-cap stocks now trading at a significant price to book discount compared to large-cap peers.

- Focusing on shorter duration stocks (dividend payers) has been additive from an attribution standpoint relative to non-dividend paying stocks.

- Historically, international stocks have outperformed during higher inflationary periods, but we will remain underweight relative to U.S. equities to remain more defensive

Equity Performance

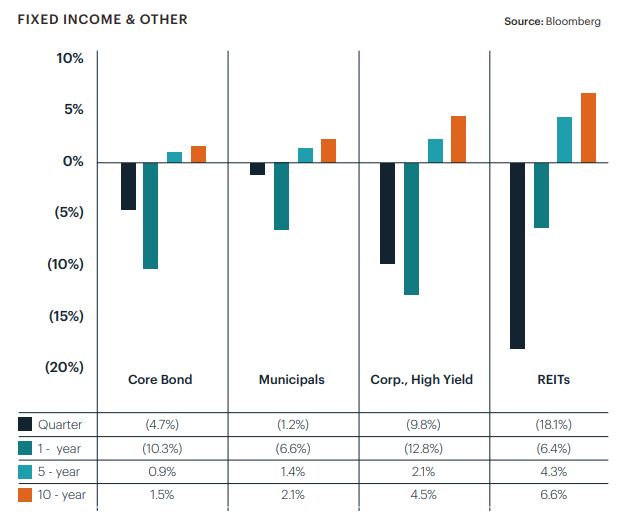

Fixed Income Performance & Key Takeaways

- Tough quarter for bonds as interest rates continued to climb with municipals outperforming relative core and high yield.

- Publicly traded REITs continued to see selling pressure along with the general equity market reinforcing why we favor less liquid real estate investments.

- We see a potential to increase duration over the coming quarter in response to markets pricing in rate hike pain, particularly if recession risks increase and yields are pushed lower.

- We continue to favor lower duration in the short term as Fed continues raising the fed fund rates to help slow inflation.

- In the second half of the year, we expect to see the yield curve flatten and the Fed continue to hike short-term rates, but we believe the bulk of hiking is behind us

Fixed Income Performance

Chart of the Quarter

The Power of the Consumer

As the world returns to pre-Covid normal, what is in store for the markets? Different sectors and regions are going to vary at what pace “normal” returns. This continues to add uncertainty and market volatility. The runway for a soft Fed landing continues to narrow, and consumer sentiment remains extremely pessimistic. This uncertainty around the markets and Fed policy could lead the U.S. economy into a mild recession. The one bright spot is the power of the consumer. As you can see in the chart above, even as consumer sentiment continues to fall with uncertainty, the U.S. consumer continues to spend. This trend could continue this year and help the U.S. to avoid a recession or keep it mild if we fall into one.

Wealth & Tax Management Key Takeaways

- The recent market decline has created significant income tax planning opportunities for many of our clients.

- For our clients with traditional IRAs who are planning on doing a Roth conversion in 2022, now is an excellent time to convert in-kind shares from your IRA to your Roth IRA at depressed prices.

- For our clients with taxable investment accounts, we’ve been proactively looking for opportunities to “harvest losses” that can then be used to offset capital gains and a small portion of your ordinary income this year and in future years.

- Given these recent tax planning opportunities and our expectation of significant changes to both the federal income and estate tax codes in the next four years, we are expanding our tax planning capabilities with the addition of new team members (in house and outsourced) and software upgrades.

Wealth and Tax Management Chart of the Quarter

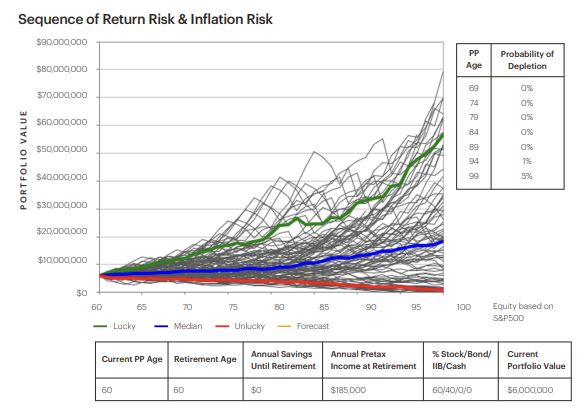

Lifestyle Protection Analysis Example

One of the best ways to “tune out” the noise surrounding current market conditions is to revisit your Wealth Optimization Plan (WOP). Specifically, the Lifestyle Protection Analysis (LPA) within your WOP stress tests your current portfolio and projected cashflow against the sequence of returns and real inflation of past markets. Updating your LPA can give you the peace of mind that you are on the right financial path or equip you with the timely information you need to make necessary adjustments. We’re happy to update your WOP/LPA now or as part of one of your upcoming regularly scheduled Clarity Session.

Janiczek Wealth Management – At a Glance

To learn more about Janiczek Wealth Management, click here.

Important Disclosures

The content herein is to be used for informational purposes only. Neither Janiczek Wealth Management or its owners and employees represent or warrant the accuracy or completeness of the information contained in this report. In no event will Janiczek Wealth Management or its owners or employees be liable for any damages that may result from the use of or reliance on these materials.

Past performance may not be indicative of future results. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy (including the investments and/or investment strategies recommended and/or undertaken by Janiczek® Wealth Management (“Janiczek®”), or any non-investment related services, will be profitable, equal any historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Janiczek® is neither a law firm nor accounting firm, and no portion of its services should be construed as legal or accounting advice. Moreover, you should not assume that any discussion or information contained in this document serves as the receipt of, or as a substitute for, personalized investment advice from Janiczek®. Please remember that it remains your responsibility to advise Janiczek®, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/ evaluating/ revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. A copy of our current written disclosure Brochure discussing our advisory services and fees is available upon request. The scope of the services to be provided depends upon the needs of the client and the terms of the engagement.

TM & Copyright Janiczek Wealth Management. All rights reserved. Do not reproduce or redistribute in any form without prior written permission. Strength Based Wealth Management® 35 Essential Strengths®, The Stages of Financial Freedom®, Wealth Optimization Plan™, Wealth Optimization Dashboard™, Lifestyle Protection Analysis™, Elastic Limit Wealth Threshold™, Flourish! Activators™, FLOURISH!™ and Flourish! Based Retirement Planning™ are all trademarks of Wealth with Ease, LLC. For details, call 303-721-7000.