January 2023

Investment Conditions & Outlook

Executive Summary

For most investors, 2022 will be remembered as a year they want to forget. Investors worldwide, and across nearly all sectors, experienced double digit declines in both stock and bond investments as the Fed continued to tighten monetary policy to combat inflation.

On the positive side, our portfolios were well positioned for what we anticipated was going to be a more volatile year resulting in out-performance of both stock and bond investments. We anticipated rising rates early in the year and moved to underweight duration which helped to contain fixed income losses. We shifted our equity allocation to an overweight in well capitalized companies paying strong dividends in the value space which helped contain equity losses. Holding cash reserves and a variety of alternative strategies also helped. We booked tax losses where it made sense to increase the tax alpha of our portfolios moving forward. While the markets continue to recover and adjust to a new normal, the path forward is at least clearer. Over the last decade, much of what investors have come to expect has changed. The Fed is no longer our friend, and it will remain hawkish until inflation is under control. Money will no longer be cheap, and interest rates may remain a headwind for many asset classes. Time will tell how long these forces endure, but they will keep us and all investors vigilant.

We enter the new year with a benchmark neutral allocation to equities. We continue to prefer owning well capitalized U.S. companies that pay healthy dividends. Our portfolios remain underweight growth stocks as the interest rate path remains uncertain. Our growing interest and attention are on undervalued small-cap stocks and non-U.S. stock earnings with potential out-performance given the possibility of a softer dollar. Bonds of varying maturities and credit ratings appear appealing. They should again provide a portfolio with stability and income to counteract the volatility of the equity market.

A recession in 2023 is widely anticipated and arguably already priced into the market (most models indicate a mild recession as a result of strong economic backdrop). If a recession does come to fruition, most bull markets begin coming out of a recession. On the inflation front, there is solid evidence that goods inflation has peaked and will continue to fall, while sticky services inflation may remain higher for longer. Jerome Powell remains committed to battling inflation, and the adage “don’t fight the Fed” remains wise advice.

These are the types of challenging periods investors should expect to experience and the conditions where one’s long-term resolve can get tested. It is precisely why we so strongly believe in coupling our Evidence Based Investing (EBI) approach with our Strength Based Wealth Management (SBWM) discipline. While we can’t control the markets, we can put the odds of success in our clients favor by staying disciplined, prepared, and nimble. This includes controlling what we can control when it comes to client portfolio design, cash flows, reserves, balance sheets, taxes, expense ratios, distribution rates, and behaviors. As always, our Janiczek Wealth Management team will be working closely with you to navigate conditions as we do our best to address your short-term and long-term needs and objectives.

The Janiczek Team

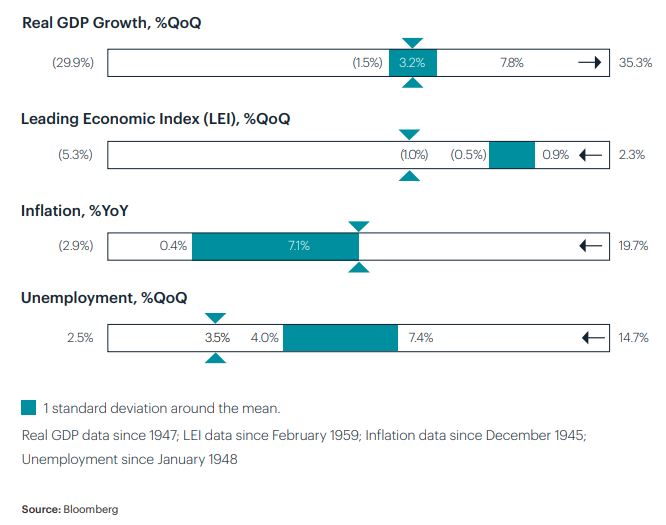

Economic Conditions and Key Takeaways

- Inflation in the United States appears to have peaked in June, with CPI providing solid cause to anticipate we are on a declining path for 2023 (but still above central bank targets).

- While the shift to higher inflation and rates feels different, it is a return to normalcy after a decade of deflation and ultra-low rates that followed the financial crisis.

- Economic growth will remain low in 2023 against tighter monetary policy and higher inflation.

- The chances of a recession in 2023 remain high. However, we still believe it will be a moderate recession based on a resilient labor market, slowing inflation, and the ability for interest rates to move lower.

- Low unemployment and strong wage growth continue to defy the slowing economy story and will be key indicators of the severity of a recession.

Economic Conditions

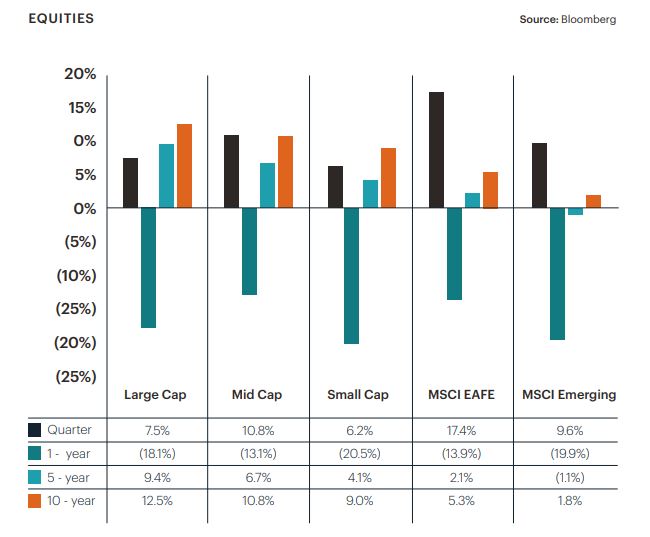

Equity Performance and Key Takeaways

- We expect volatility in the equity markets given the ongoing tug-of-war between Fed messaging and market expectations.

- As markets focus on higher for longer rates, we expect to see companies with stable earnings, strong balance sheets, and stable dividends faring well in this environment.

- The weakening of the U.S. dollar in 2023 could lead to opportunities in international markets and relative outperformance.

- Emerging markets offer attractive risk/return opportunities if China adds stimulus and loosens COVID restrictions.

- As we await an eventual economic recovery, the long-term investor can take advantage of low valuations and a disciplined investment approach.

Equity Performance

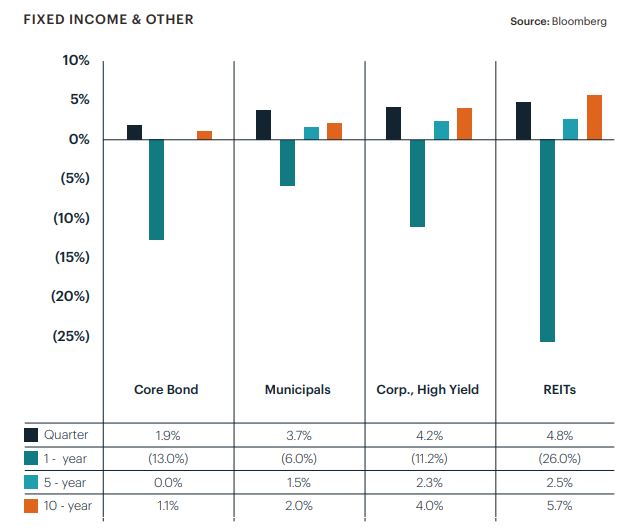

Fixed Income Performance & Key Takeaways

- Bonds are positioned to make a comeback after experiencing the worst year of returns in 2022.

- Bonds, starting the year with historically high yields, should look more attractive as inflation and rates begin to normalize.

- Look for us to transition from low-duration short-term bonds to core bonds as the year progresses, and rate hikes become a thing of the past.

- Risk for bond investors is a renewed phase of volatility in rates due to higher-than-expected inflation.

- Money market funds continue to offer tactical opportunities as yields remain attractive.

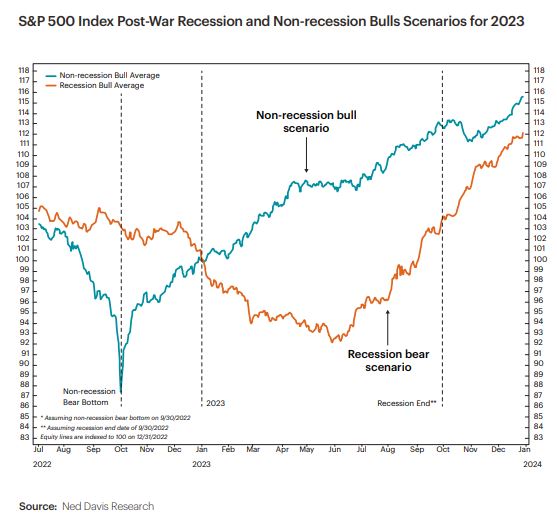

Chart of the Quarter

Historical data can tell us about what has occurred, but it can only provide a foundation for what may happen in the future. It is worth noting two phenomena related to the stock market and recessions. First, bear markets have never ended before the start of a recession, and the stock market tends to lead the economy out of a recession. This information is essential when we examine the Chart of the Month. The orange and blue lines in the diagram above represent two average composites of opposing possibilities. The blue line indicates that if the Fed succeeds in achieving a soft landing, 2023 might be the year of a post-recession bull rally. In other words, the 2022 low is the cycle low.

In comparison, the orange line represents recession bear markets. According to Ned Davis Research, a recession will finish by September 30, 2023, corresponding to markets falling before the recession and leading out of it. Although no crystal ball can forecast the coming twelve months, a volatile first half of the year followed by a potential second half rebound cannot be ruled out

Wealth & Tax Management Key Takeaways

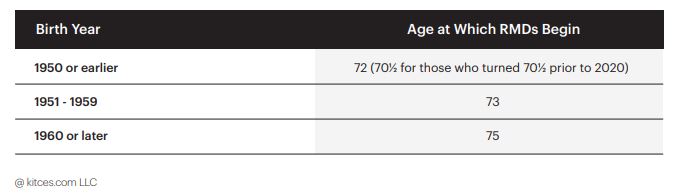

The last days of 2022 saw significant changes to the retirement planning landscape as the SECURE Act 2.0 was signed into law in Washington D.C. as part of the end-of-year 2023 Omnibus Spending Bill. While the SECURE Act 2.0 changes and adds more than 90 retirement related provisions, 6 are most relevant to our clients:

- The age when Required Minimum Distributions (RMDs) must begin from qualified retirement accounts increases from 72 to 73 starting in

2023, increasing again to 75 in 2033. - Starting in 2024, RMDs will no longer be required from Roth accounts in employer retirement plans.

- The annual limit of $100,000 for Qualified Charitable Distributions (QCDs) from individual retirement plans will now be increased annually for inflation, and the type of charities that can receive a one-time QCD is expanded to include charitable remainder unitrusts, charitable remainder annuity trusts, and charitable gift annuities, with certain limitations.

- Employers will be able to provide employees the option of receiving vested matching contributions to Roth accounts within an employer plan, previously all matching contributions were made on a pre-tax basis.

- Starting January 1, 2025, individuals ages 60 to 63 will be able to make higher catch-up contributions (up to $10,000) to their employer retirement plan. Important caveat: starting in 2024, if you have wages more than $145,000 in the prior calendar year, all catch-up contributions to employer retirement plans at age 50 or older will need to be made to a Roth account in after tax dollars – this is a significant change for high income savers.

- 529 plan assets held in a 529 plan that has been open for at least 15 years can now be rolled over into a Roth IRA in the name of the same beneficiary, subject to annual Roth contribution limits/requirements and an aggregate lifetime limit of $35,000.

We’ll be addressing these changes and any planning opportunities they create for your specific situation in our upcoming Clarity Sessions. In the meantime, please reach out to your Janiczek Team with any questions you may have.

Wealth and Tax Management Chart of the Quarter

SECURE Act 2.0 Phased-In Timeline For RMD Beginning Ages

Janiczek Wealth Management – At a Glance

To learn more about Janiczek Wealth Management, click here.

Important Disclosures

Past performance may not be indicative of future results. Different types of investments involve varying degrees of risk. Therefore, there can be no assurance that the future performance of any specific investment or investment strategy (including the investments and/or investment strategies recommended and/or undertaken by Janiczek Wealth Management [“Janiczek”]), will be profitable, equal any historical performance level(s), or prove successful. The account performance information reflects the reinvestment of dividends (to the extent applicable), is net of applicable transaction fees, and is net of Janiczek’s investment management fee (if debited directly from the account). Account information has been compiled solely by Janiczek, has not been independently verified, and does not reflect the impact of taxes on non-qualified accounts. In preparing this report, Janiczek has relied upon information provided by the account custodian. Please defer to formal tax documents received from the account custodian for cost basis and tax reporting purposes. Please remember to contact Janiczek, in writing, if there are any changes in your personal/ financial situation or investment objectives for the purpose of reviewing/evaluating/revising our previous recommendations and/or services, or if you want to impose, add, or modify any reasonable restrictions to our investment advisory services. Janiczek shall continue to rely on the accuracy of information that you have provided. Please Note: Unless you advise, in writing, to the contrary, we will assume that there are no restrictions on our services, other than to manage the account in accordance with your designated investment objective. Please Also Note: This Report is provided for information purposes only and is not an official statement from the account custodian or any product sponsor. Please compare this Report with account statements received from the account custodian. The account custodian does not verify the accuracy of the advisory fee calculation. Please advise us if you have not been receiving monthly statements from the account custodian. A copy of our current written disclosure Brochure discussing our advisory services and fees continues to remain available upon request or at www.janiczek.com.

Historical performance results for investment indices, benchmarks, and/or categories have been provided for general informational/comparison purposes only, and generally do not reflect the deduction of transaction and/or custodial charges, the deduction of an investment management fee, nor the impact of taxes, the incurrence of which would have the effect of decreasing historical performance results. It should not be assumed that your Janiczek account holdings correspond directly to any comparative indices or categories. Please Also Note: (1) performance results do not reflect the impact of taxes; (2) comparative benchmarks/indices may be more or less volatile than your Janiczek accounts; and, (3) a description of each comparative benchmark/index is available upon request.

ANY QUESTIONS: Janiczek Wealth Management’s Chief Compliance Officer remains available to address any questions regarding this Report.

Please Note: Unsupervised/Unmanaged Assets – Janiczek does not maintain any investment monitoring or performance responsibility for unmanaged or unsupervised assets and/or accounts. The client and/or its other investment professionals retain exclusive responsibility for the monitoring and performance of such assets and/or accounts. These assets are included for reporting purposes only.

Please Note: Private/Alternative Investment Funds- The value(s) for all private investment funds owned by the client reflect the most recent valuation provided by the fund sponsor. However, if subsequent to purchase, the fund has not provided an updated valuation, the valuation shall reflect the initial purchase price. If subsequent to purchase, the fund provides an updated valuation, then the statement will reflect that updated value. The updated value will continue to be reflected on this report until the fund provides a further updated value. As result of the valuation process, if the valuation reflects initial purchase price or an updated value subsequent to purchase price, the current value(s) of an investor’s fund holding could be significantly more or less than the value reflected on this report. Unless otherwise indicated, the client’s advisory fee shall be based upon the value reflected on this report. Please Also Note: If the private fund is a private equity or real estate fund, the value reflected on this report will generally reflect the most recent “fair-value” determined by the fund sponsor, fund CPA or independent valuation service, rather than market value as used for all non-private fund liquid investment assets (i.e. mutual funds, ETFs, individual equity and fixed income securities, etc.).

TM & Copyright Janiczek Wealth Management. All rights reserved. Do not reproduce or redistribute in any form without prior written permission. Strength Based Wealth Management® 35 Essential Strengths®, The Stages of Financial Freedom®, Wealth Optimization Plan™, Wealth Optimization Dashboard™, Lifestyle Protection Analysis™, Elastic Limit Wealth Threshold™, Flourish! Activators™, FLOURISH!™ and Flourish! Based Retirement Planning™ are all trademarks of Wealth with Ease, LLC. For details, call 303-721-7000.