July 2023

Investment Conditions & Outlook

Executive Summary

As we wrap up the first half of the year, we remain impressed with the economic resiliency and subsequent retracement of global stocks. Much like last quarter the equity market bounce has remained narrow and led by a single sector. The technology sector continued to be the significant driver of market performance. Companies involved in areas such as cloud computing, e-commerce, digital payments, and artificial intelligence attracted considerable investor attention and valuation expansion. However, regulatory scrutiny and concerns over valuation levels impact our view on this sector going forward.

If the strength of the recovery had been broad based, with many stocks making gains, it would be easier to call this a new bull market. But the opposite remains true. Historically, early cycle bull markets tend to be led by economically sensitive segments of the market, mainly small and micro-cap companies. The weakness in these segments this year does not support a new bull market. It could also be that a new bull market, albeit one that does not look like past bull markets, is quietly underway and we must wait to see how it plays out. We remain at target/neutral equity allocations emphasizing factors, such as profitability and strong balance sheets, we believe can be more resilient and less volatile should the economy slip into a mild (or more severe) recession later this year or in 2024.

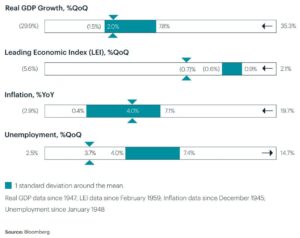

The Fed and the continued fight to get inflation back to the long-term target of 2% remain front and center. Until recently, the consensus among investors was the Fed had raised rates for the final time this cycle with some even expecting rate cuts. That outlook changed after the recent rhetoric from Jerome Powell indicating a continued hawkish stance and markets should expect additional rate hikes. Ultimately, whether the Fed hikes or continues to pause comes down to inflation and employment. Inflation continues to move in the right direction. Even so, inflation in most parts of the world still exceeds the long-term goal of the Fed, potentially signaling that inflation has become structurally higher. And the employment picture continues to show resiliency in the labor market.

With discussions of a pending recession in the U.S. being commonplace, it continues to look like the U.S. could avoid a substantial broad-based recession. We anticipate some weakness from the lag of aggressive monetary policy in the second half of this year but anticipate economic activity could remain resilient. This could lead to a stronger growth outlook in 2024 as the economy continues to recover. There is still the possibility of a downside scenario in which global growth is hit harder than expected with a recession ensuing first in the U.S. then cascading to other global economies.

We continue to see wary market participants sitting on the sideline on high levels of cash and cash equivalents. This level of cash should be reassuring for investors as this dry powder could (and should) flow back into markets at some point. While we continue to hold cash in our portfolios due to current yield, we do not want to overlook attractive opportunities. We continue to see opportunities in emerging and some developed markets given the attractive valuations, looser monetary policy (mainly China) and a weaker dollar.

As we move into the second half of 2023 the balance of current economic forces appear to be tilted against capital markets. This could cause heightened volatility but provide attractive entry points for long term investors. Persistent inflation and central bank tightening continue to pose risks. In uncertain environments, owning a diversified portfolio offering different characteristics and styles can help weather the storm. Thus, we believe our mix of equities, fixed income instruments, cash, and, where appropriate, alternatives, positions our clients well for the remainder of 2023 and into 2024.

The Janiczek Team

Economic Conditions and Key Takeaways

- Inflation remains well above the Fed’s long-term target rate of 2% and maintained a stance of further rate hikes if inflation does not continue to track lower in the near term.

- Moderating inflation will eventually lead to a policy pivot, but that time is not soon.

- Economic resilience has driven S&P to banner start of the year despite dependency on the technology sector with concerning valuations.

- Commodities and related sectors have underperformed so far this year.

Economic Conditions

Equity Performance and Key Takeaways

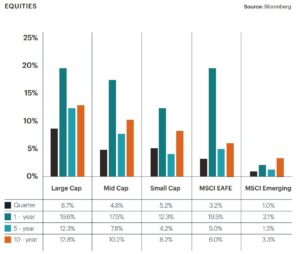

- Mega-cap and growth stocks have, in 2023, led the way lifting U.S. over international equities and large over small.

- Earnings expectations and valuations don’t, in our opinion, fully reflect the current risk of recession, leading us to continue to hold some defensive sectors that can under perform concentrated mega cap growth sectors like technology over shorter periods of time. Last year the opposite was true.

- With the assumption that the Fed will hold rates higher for longer, big tech names could suffer, paving the way for small cap stocks.

- Participation in the recent rally was mostly limited to growth sectors, but breadth has started to broaden, and we could see a leadership rotation in the second half of year that could once again favor a more defensive allocation.

- Emerging markets stocks look attractive as the rate cycle looks to have peaked and the dollar continues to look weaker relative to other currencies.

Fixed Income Performance & Key Takeaways

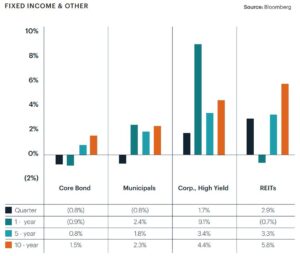

- Fixed income continues to offer attractive “income” after yields have surged globally.

- Short-term bonds continue to look attractive for current income and offer the ability to preserve capital as the Fed continues their regime to fight inflation.

- Central banks are unlikely to come to the rescue with rate cuts we have seen historically in recessions; our current assumption is rates will stay higher for longer, supporting our strategy of not overextending bond duration.

- We continue to exclude high yield as an recommended holding due to tight spreads and the expectation of tighter credit and financial conditions moving forward.

Chart of The Quarter

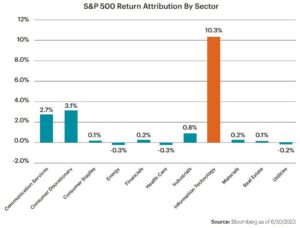

When looking at sector specific returns it is easy to see the commanding performance attribution from the technology sector. In June we experienced a rally in valuations against a backdrop of slowing or declining earnings. The price to earnings ratio is well above the historic mean and with chances of a recession on the horizon, the risk of missed earnings could lead to a retracement in the in the mega cap names. More specifically, 80% of the S&P return this year is from just 10 stocks. This leaves other sectors ripe for a leadership change in the second half of the year.

Wealth & Tax Management Key Takeaways

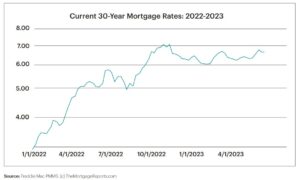

Over the past sixteen months, it has become increasingly difficult to finance a home purchase via traditional bank mortgage avenues. Not only have interest rates risen sharply during this period (see the chart), but underwriting standards have tightened due to the recent turmoil in the regional banking sector. Not surprising, we’ve had several clients ask how they can help their adult children or grandchildren in this more difficult lending environment, while being as tax efficient as possible. We typically recommend two approaches, or a combination of both:

- Gifting Approach – A married couple can give $34,000 ($17,000 each) to a child without any gift/estate tax consequences in 2023. Anything over that amount and a gift tax return must be filed and they start to erode their federal gift/estate tax exemption of just under $26 million in 2023. For our married clients with estates under this $26 million threshold, this is of no tax consequence to them, it is more of an administrative/filing matter. Clients will typically gift whatever down payment amount is needed to allow their child to qualify for a traditional mortgage on their own. Added income tax benefit can be gained by gifting highly appreciated securities in-kind to a child in a low tax bracket who can then sell the securities with no or lower capital gains tax, and then use the cash to make the down payment.

- “Bank of Mom and Dad” Approach – As long as a mortgage is properly recorded with the city/county where the property is located and the child pays interest at or above the published Applicable Federal Rate (AFR) at the time of origination, mom/dad can be the lender to the child. The child gets to deduct the interest payments for income tax purposes like a traditional mortgage and the interest payments received by mom/dad are taxable as ordinary income to them. This can be an attractive option for our clients whose child may not qualify for a traditional mortgage at today’s higher interest rates. We can help you decide which approach or combination of approaches is best for your family in close coordination with your CPA/tax preparer and your estate planning attorney.

Wealth and Tax Management Chart of the Quarter

Traditional 30-year fixed mortgage rates ended the quarter averaging 6.71%, an increase of 3.6% from where they were at the beginning of 2022. In contrast, the Applicable Federal Rate (AFR) for intra-family loans of more than 9 years was at 3.79% at the end of the quarter, significantly less than the 6.71% average rate for 30-year fixed mortgages.

Janiczek Wealth Management – At a Glance

To learn more about Janiczek Wealth Management, click here.

Find Important Disclosures here.