October 2022

Investment Conditions and Outlook

Executive Summary

From multiple perspectives, the world remains a complicated place to invest. Inflation, war, monetary policy shifts, supply chain disruptions, natural disasters, and currency fluctuations are just some of the significant events keeping government officials, business leaders and investors on their toes. Combating inflation and the threat of a subsequent mild, moderate, or severe recession remain at the top of the worldwide list of concerns, as do the implications for future profit growth.

Analysts and investors have been trying to account for the earnings impact of tighter monetary policy, sticky inflation, and the potential for a recession. While it is still too early to declare a recession in the United States, it is less likely that the much-publicized Fed soft landing will materialize, as Jerome Powell has boxed himself into a corner with little possibility of a pivot to a less hawkish stance this year. If the United States enters a recession, evidence indicates a light recession constrained by consumer and business financial health. Of course, a more severe recession appears unavoidable in the eurozone, where rising energy prices are wreaking havoc on the economy.

While it’s difficult to find positive news in the media, a few sources of comfort include the fact that market sentiment is extremely negative and consumer spending and employment is steady. With investor sentiment at record lows, markets are already pricing (if not overpricing) adverse economic news. Because U.S. equities are already in a bear market (S&P 500 down 24% YTD), poorer economic data and slower profit growth are probably already priced in while business balance sheets and profit margins still remain fine. Therefore, we do not see a rationale weight of the evidence reason to alter from our current (partially defensive) position. Owning quality holdings that are supported by solid talent and the ability to weather storms and take advantage of opportunities is our best answer to clients and all investors. We will continue to favor domestic large-cap stocks with an emphasis on quality. Stocks continue to trade at a discount to long-term averages and have the potential to outperform when forward-looking. Portfolio construction concentrating on defensive holdings might give some respite in pursuing long-term financial goals.

We feel now is the time for intermediate and long-term investors to put fortitude to the test and stick to their long-term wealth plan. The entire thesis of our comprehensive wealth management and investment approach is to be able to help clients successfully navigate through such challenging times. Simply put, building, and maintaining a strong balance sheet, cash flow, portfolio, and overall financial strength position (via our 35 Essential Strengths®) in combination with a prudent and disciplined investment approach, is our answer to successfully weathering such storms and being in position to take advantage of the opportunities that ultimately can come from such times.

The Janiczek Team

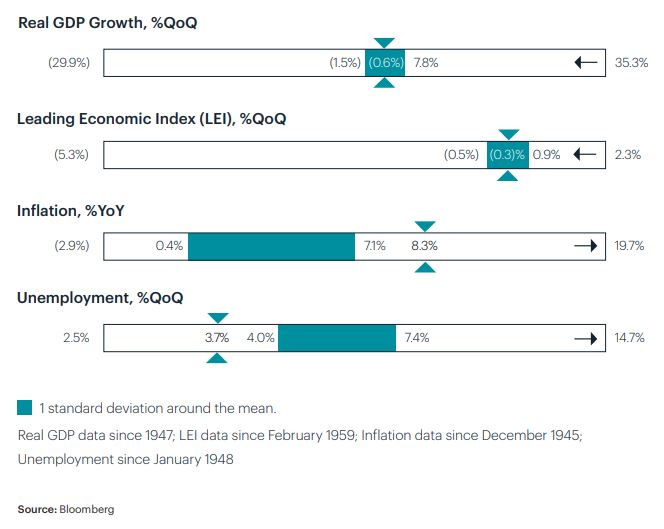

Economic Conditions and Key Takeaways

- The global economy is in a sustained slowdown due to hawkish monetary policy and high inflation.

- Inflation continues to dominate macroeconomic issues for global markets with almost 80% of major central banks raising their rates.

- Different sectors of the economy will react independently to tighter monetary policy and will not see immediate slowing, meaning inflation should run above long-term average well into next year.

- Labor market remains hot, but we would expect to see unemployment increase as economy continues to slow.

- Surging mortgage rates has led to double digit declines in home sales and mortgage applications continuing to decline.

Economic Conditions

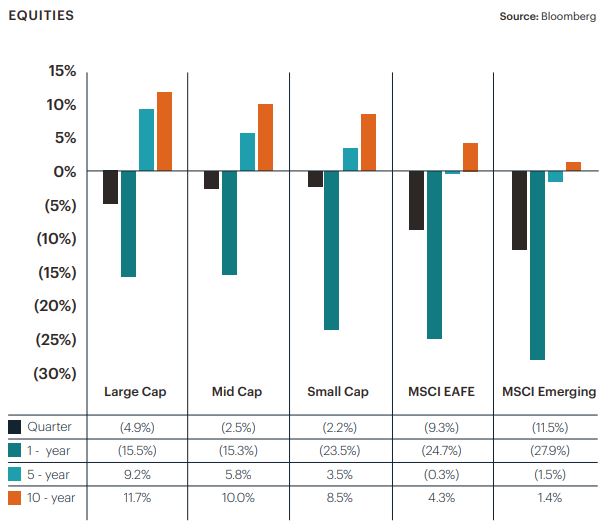

Equity Performance and Key Takeaways

- On a global scale, there has not been much reprieve from repricing of stocks, with the U.S. outperforming the rest of world on a relative basis.

- Energy sector continues to be the only positive performer year to date as the war in Ukraine continues to stress supply.

- International developed equities, although underperforming U.S. this year, remain attractive due to better valuation and ability to benefit from a weakening U.S. dollar as Fed becomes less hawkish.

- Historically, cooling inflation from high levels has been associated with positive returns in equites and bonds.

- Emerging market equities could recover if there is significant China stimulus.

- A year-end rally is still on the table as part of a countertrend rally from deeply oversold levels driven by a reversal from extreme pessimism

Equity Performance

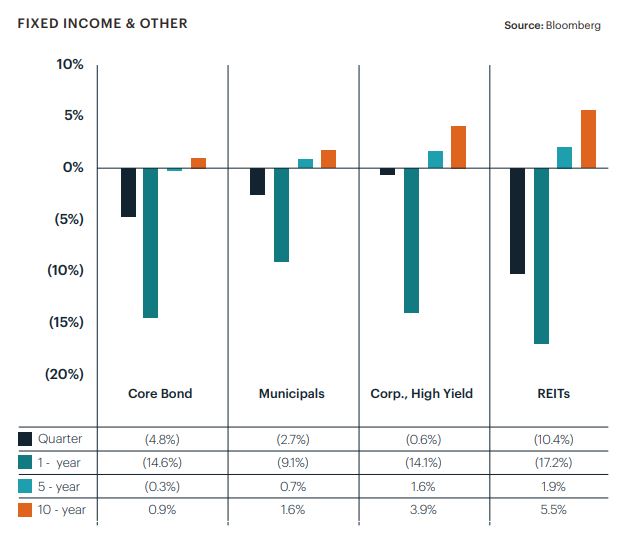

Fixed Income Performance & Key Takeaways

- Another quarter of headwinds for fixed income investors as the Fed continues to tighten monetary policy to combat continued inflationary pressures.

- High yield credit as spreads continue to widen and will remain neutral until signs of a U.S. recession are less likely.

- Government bonds are looking more attractive as risk of further sell off is limited if inflation begins to cool.

- As default rates have not yet increased (see if that remains case as ARM loans adjust), MBS continue to offer an interesting fixed income opportunity.

- We would expect the yield curve to flatten into Q4 and give us the ability to slowly increase core bond duration.

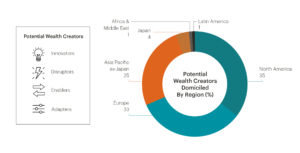

Chart of the Quarter

Decelerating GDP growth mixed with increasing rates and peak profits imply the future return of equities will come under pressure. Looking ahead we anticipate companies who can innovate, disrupt, enable, and adapt that will be well positioned to thrive into the future. While we now favor U.S. markets, the rest of the globe looks quite appealing in the long run, especially with the dollar weakening (at some point) for disruptive companies to experience outsized growth. In a world of limited wealth creation, we will remain focused on segments of the market that can be potential wealth creators of the future.

Wealth & Tax Management Key Takeaways

- The Inflation Reduction Act of 2022 was passed in Washington DC this past quarter, much of which will have little direct impact on our clients.

- This Act is of interest to our clients enrolled in Medicare, as it seeks to reform Medicare’s prescription drug pricing, now giving Medicare the ability to negotiate the price of certain prescription drugs and putting in place a limit of $2,000 on annual out-of-pocket prescription drug costs starting in 2025.

- On the tax front, the Act earmarks $80 billion to ramp up IRS tax enforcement over the next 10 years, much of which is speculated to be aimed at high-net-worth and high earning taxpayers, meaning proper tax planning for our clients is going to be more important than ever.

- For our clients enrolled in Medicare, open enrollment begins October 15th and ends December 7th, presenting the opportunity to switch plans for 2023.

- End-of-year tax planning season is quickly approaching, meaning we will be helping clients on a case-by-case basis to analyze year-to-date withholdings to prevent underpayment penalties, to ensure retirement plan contributions are maximized, to optimize Roth IRA conversions, to ensure Required Minimum Distributions (RMDs) are taken, and to assess charitable giving opportunities, to name a few focus items.

Wealth and Tax Management Chart of the Quarter

The Value of An Advisor in Turbulent Markets

Over twenty years ago, Vanguard began studying the value that financial advisors provide to clients versus those who self-manage their portfolios. Vanguard concluded that advisors can add up to, or even exceed, 3% in net additional returns for their clients over time, primarily by keeping clients invested in the market during turbulent times with a disciplined and systematic approach to portfolio management, unencumbered by emotion. Why is staying in the market during turbulent times so important? See the chart below. Missing the 10 best market days over the past 10 years would have cost an investor over $200,000 in lost returns, keeping in mind that the average intra year drop of the market during that same time period was over 11%!

Janiczek Wealth Management – At a Glance

To learn more about Janiczek Wealth Management, click here.

Important Disclosures

The content herein is to be used for informational purposes only. Neither Janiczek Wealth Management or its owners and employees represent or warrant the accuracy or completeness of the information contained in this report. In no event will Janiczek Wealth Management or its owners or employees be liable for any damages that may result from the use of or reliance on these materials.

Past performance may not be indicative of future results. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy (including the investments and/or investment strategies recommended and/or undertaken by Janiczek® Wealth Management (“Janiczek®”), or any non-investment related services, will be profitable, equal any historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Janiczek® is neither a law firm nor accounting firm, and no portion of its services should be construed as legal or accounting advice. Moreover, you should not assume that any discussion or information contained in this document serves as the receipt of, or as a substitute for, personalized investment advice from Janiczek®. Please remember that it remains your responsibility to advise Janiczek®, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/ evaluating/ revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. A copy of our current written disclosure Brochure discussing our advisory services and fees is available upon request. The scope of the services to be provided depends upon the needs of the client and the terms of the engagement.

TM & Copyright Janiczek Wealth Management. All rights reserved. Do not reproduce or redistribute in any form without prior written permission. Strength Based Wealth Management® 35 Essential Strengths®, The Stages of Financial Freedom®, Wealth Optimization Plan™, Wealth Optimization Dashboard™, Lifestyle Protection Analysis™, Elastic Limit Wealth Threshold™, Flourish! Activators™, FLOURISH!™ and Flourish! Based Retirement Planning™ are all trademarks of Wealth with Ease, LLC. For details, call 303-721-7000.