The idea of identifying a sustainable withdrawal rate in retirement is nothing new, yet the topic is getting more and more attention in recent times. I challenge you to type “retirement 4 percent withdrawal rule” into your preferred internet search engine. You will likely be surprised by the sheer number of results. Also, a quick scan of those results would lead you to believe that the 4 Percent Rule is no longer a valid concept in planning for retirement.

The idea of identifying a sustainable withdrawal rate in retirement is nothing new, yet the topic is getting more and more attention in recent times. I challenge you to type “retirement 4 percent withdrawal rule” into your preferred internet search engine. You will likely be surprised by the sheer number of results. Also, a quick scan of those results would lead you to believe that the 4 Percent Rule is no longer a valid concept in planning for retirement.

To clarify, the 4 Percent Rule refers to the idea that retirees should not outlive their retirement portfolio as long as they limit their initial withdrawal to 4% or less of their portfolio accumulation. Withdrawals in subsequent years would then adjust with inflation.

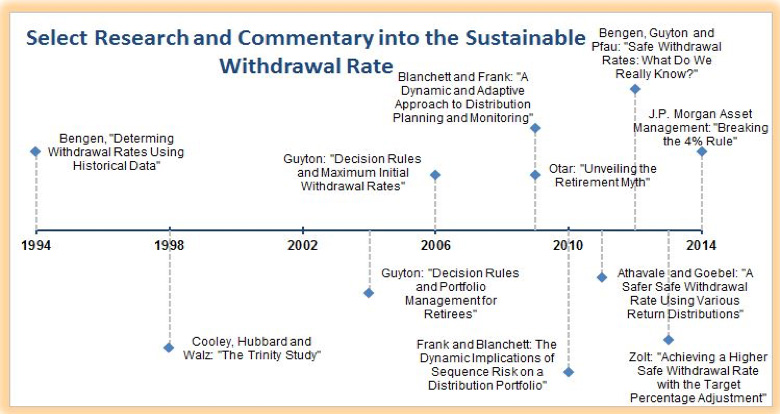

The 4% rule was first put forward by William Bengen in 1994, and as you can see in the following timeline, the volume and pace of subsequent research has picked up as time goes by. Each of the subsequent research articles and white papers put a slightly different twist on the 4% rule as it applied to retirees under changing market and economic conditions.

In actuality, the 4% rule has been a widely used proxy for a sustainable initial withdrawal rate by many in the financial planning community. We here at Janiczek Wealth Management have long guided our clients to a “3.9% or less” withdrawal rate. However, we also back up that rule of thumb with more robust scenario analysis that takes into account the actual market performance and inflationary cycles back to the year 1900. We believe that this approach provides our clients with greater confidence as to the retirement lifestyle they can maintain.