Investors can see the fears that are looming over the markets. Inflation has reached levels not seen since 1981, the Fed is prepared for the most aggressive monetary policy tightening since 1994, earnings growth is slowing, and the Russia/Ukraine situation has driven commodity prices to all-time highs.

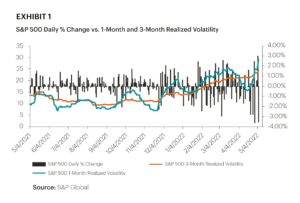

As a result of these negative headwinds, the S&P 500 is down more days than it is up this year (56% down days versus 44% up days), and volatility has grown significantly (Exhibit 1). With a shaky start to the year, the first quarter of 2022 was the third worst in S&P 500 ever. The drop in equity market prices clearly shows what investors are doing, but is it warranted? Since its start, the S&P 500 has had an average intra-year decline of 14%. As of this writing, the S&P 500 is down 13.3% for the year, which is still less than the average intra-year fall.

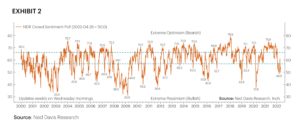

The sentiment chart below from Ned Davis Research demonstrates the fast shift to extreme pessimism. We are not yet at the depths seen in December of 2018 or the Covid crisis in March of 2020, but if the momentum continues, we might approach those levels, and we know how the markets behaved after hitting those lows. We wouldn’t be shocked to see a short-term market rally if we used the same logic in the current defensive market environment.

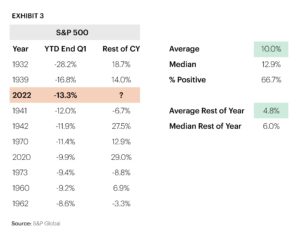

When we compare the first quarter performance of the S&P 500 to comparable historic lows, one can potentially see the stage being set for a significant market comeback for the remainder of the calendar year. The S&P 500’s first quarter was the third worst in its history. When looking at the top ten worst starts, the average return for the remainder of the year is 10%. When looking at the average rest of year return of the S&P 500, an investor would get slightly under 5% on average. From here, we may see a return that is twice as high as the average for the remainder of the year.

Bond’s performance paints a similarly bleak picture. Markets have pulled the Fed Funds rate hikes forward. In the first quarter of 2022, US equities (S&P 500 Index) and US bonds (Bloomberg US Aggregate Bond Index) were negative. This was the first quarter since the first quarter of 2018, when both stocks and bonds declined. In the past 46 years (since 1976), equities and bonds had negative returns in 19 quarters (out of 185). According to BNY Mellon’s Quarterly Return scatter plot, this has happened 10% of the time in the past. Further investigation revealed that stocks gained around 69% of the time, while bonds gained 77% of the time. Since 1976, equities, bonds, or both have produced quarterly profits almost 90% of the time.

These historical statistics support the role of bonds in a portfolio. Bonds tend to get beaten down in the face of aggressive monetary policy shifts, but they have also shown to be a long-term stabilizer to equity market volatility.

Moreover, despite the current bond market downturn, expected bond returns are still higher than in the past. Rising interest rates hurt the bond market in the near term but also result in greater long-term returns for fixed income. According to bond yield data from Robert Shiller’s database, the correlation of starting yields to forward returns for US government bonds over the next five years is 0.9. This correlation is a good predictor of returns on high-quality bonds. The iShares Aggregate Bond ETF (AGG) presently has a yield to maturity of 3.51%. This is not a very high yield compared to historical yields, but it is significantly higher than it was during the pandemic.

Current S&P 500 valuations remain appealing, and one-year S&P returns might be positive. According to Bloomberg, consensus earnings for the S&P 500 remained stable at $228 per share in the first quarter. The price-to-earnings ratio is about 18.1 times consensus 2022 earnings, much lower than the 25.9 multiple on pre-pandemic 2019 earnings. Profit margins are strong, with firms typically able to pass on increasing input costs to consumers.

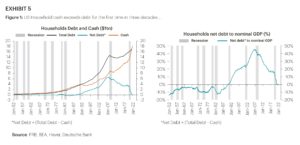

When we look at the global economy, we find that robust consumer spending and wage growth are helping to balance a large portion of the recent price inflation. We anticipate ongoing but slower growth in the United States and developed foreign markets (the Russia/Ukraine crisis may influence the developed growth outlook). In terms of consumers, household balance sheets have been improving since the Great Financial Crisis. As seen in Exhibit 5, households now have more cash than debt on their balance sheets for the first time in three decades.

Trying to time the markets is a dangerous game with potentially disastrous consequences. Market volatility is typical, and it should not deter investors from sticking to their long-term investing strategy. It is critical to remain invested and to stay the course. Investors who miss some of the best market days may miss out on critical opportunities to grow their portfolios. Seven of the best ten days occurred within two weeks of the 10 ten worst market days. During times of increased volatility and market uncertainty, we rely on the knowledge that maintaining a diverse portfolio of high-quality assets works. A diversified portfolio of stocks, bonds, and other uncorrelated assets has shown to be a winner despite worldwide pandemics, wars, and other market headwinds.

If you are interested in learning more about our comprehensive wealth, tax, and investment management services, please contact Cathy Wegner, Director of New Client Engagements, 303-339-4480 or cwegner@janiczek.com.