Our clients have experienced great success in their lives. They have amassed a certain amount of wealth, which often leads to them being so financially secure and independent that they can live entirely off their assets without relying on earned income. Furthermore, our clients frequently wish to leave legacies that will last generations or fund charities that do good in the world. Capital preservation is paramount to our portfolios.

For a 30- to 40-year period beginning in the early 1980s, the legacy 60/40 portfolio welcomed the fixed income tailwind and diversification effect, but we acknowledge that fixed income as an asset class faces challenges in future returns. It’s anyone’s guess when and how much interest rates will reverse. Higher-than-average inflation in the future might easily result in a continuous loss of purchasing power for investors who are not equipped to deal with this challenge. This combination of rising inflation and rising interest rates is a lose-lose situation for current bond holders. This is generating a lot of market volatility and unpredictability.

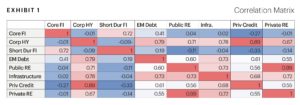

In many ways, fixed income remains a viable asset class. Still, the idea of painting with only two brushes, the Harry Markowitz efficient frontier of just equities and bonds in a portfolio, now appears to be a naïve approach. Alternative asset classes provide investors with distinct return and risk profiles in exchange for liquidity, known as the illiquidity premium. Investors who accept the illiquidity premium have the potential opportunity to experience lower volatility than public asset classes, higher yields than traditional fixed income, and a negative correlation with traditional fixed income assets (Exhibit 1).

Alternative asset classes with illiquidity premium characteristics include: 1) direct lending, 2) core transportation, 3) infrastructure, and 4) global real estate. Here at Janiczek Wealth Management, our broader approach to optimizing public market assets (stocks, bonds, ETFs, etc.) and private market assets (such as those described above) enables us to advise clients on such things in a comprehensive manner. We also consider public and private aspirational assets (private business ownership, venture capital, angel investing, and cryptocurrencies). But let’s take a closer look at the four private investment options we believe are worthwhile possibilities for high and ultra-high net worth clients prepared to use more brushes.

Direct Lending

A transaction in which investors offer credit to borrowers outside the typical banking system is known as direct lending. Investors have access to directly originated senior secured loans to private-equity U.S. middle-market firms, as well as the opportunity to engage in junior capital investments.

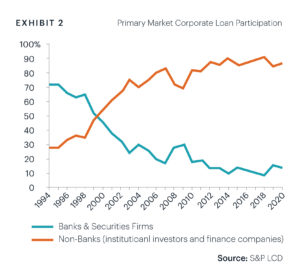

Direct lending assets under management in the United States increased by more than 800% in the decade following the Great Financial Crisis (GFC)1. The consolidation of regional banks, as well as the Dodd-Frank Wall Street Reform and Consumer Protection Act, reduced banks’ ability and willingness to originate and hold loans to middle-market companies, particularly those with riskier credit profiles. Exhibit 2 illustrates the impact: U.S. banks contributed only 10% of the leveraged loan primary market in 2020.

Because the borrowers do not have access to bank loans, middle-market loans provide lenders with greater rates and robust lender/investor protections through covenants and structuring. Furthermore, the performance of private loans is not always well correlated with that of other types of assets or with the business cycle in general.

Core Transportation

Core transportation, or core real assets in general, are high-quality, long-lived physical assets that can deliver consistent cash flows under long-term contracts. They combine the income production of a safe, fixed-income-like return stream with the greater returns that come from owning specialized assets in industries with high barriers to entry. Core real assets, in the hands of the right manager, provide high levels of income and absolute return with little correlation to stock markets and inflation protection.

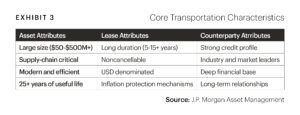

These large, real assets are crucial to the global economy. Managers can get access to global supply chains by leasing cargo ships, cargo aircraft, and other assets to high credit-quality counterparties for lengthy periods of time. Contractual revenue from long-term leases is supported by the counterparty’s balance sheet and can be the key generator of incredibly robust returns from a credit standpoint. Exhibit 3 illustrates the various appealing qualities of core transportation, in addition to long-term leases.

According to J.P. Morgan’s 2022 Long-Term Capital Market Assumptions (LTCMAs), core transportation offers a forecasted long-term return of 7.4%4. The majority of this return is realized through net cash income.

Managers must diversify investment activity across many subsectors to truly profit from a transportation strategy. COVID-19’s issues posed obstacles for global airlines, but maritime assets remained robust. A disciplined approach to portfolio construction and diversification enables managers to navigate such shocks with little or no influence on the performance of a strategy.

Infrastructure

Infrastructure refers to the underlying and fundamental assets and systems that provide essential functions for an economy’s well-being. Infrastructure poses a political risk, but it also lends itself to monopolistic tendencies. Regulated assets may be particularly appealing investments under the correct management since price control mitigates downside risk if costs rise.

To keep up with projected global demand, the McKinsey Global Institute predicts that $69 trillion would need to be spent on critical infrastructure by 20355. Due to political pressure to reduce taxes and balance budgets, infrastructure investment has steadily shifted from the public to the private sector in the developed world. With the ever-increasing demand for infrastructure assets and the ever-decreasing ability of governments to fund them, macroeconomic variables point to this trend continuing for the foreseeable future.

Being a highly capital-intensive long-life asset with an immovable physical component, infrastructure assets have potentially attractive investment characteristics: they provide essential ‘backbone’ service to the community. Also, they have a sustainable competitive advantage resulting in very low demand elasticity.

Global Real Estate

Private equity (direct ownership), publicly-traded equity (indirect ownership claim), private debt (direct mortgage financing), and publicly traded debt (securitized mortgages) are the four primary types of real estate investments. Publicly traded equity real estate instruments allow investors to participate in the returns from investment real estate while also providing improved liquidity; nevertheless, these securities can be influenced by the stock market, and returns can be erratic.

Investors can pay the illiquidity premium for favorable characteristics by investing in private equity real estate (direct ownership of real estate):

- Income and growth potential

- Volatility management

- Diversification

- Inflation protection of principal

Furthermore, non-listed REITs provide investors with unique tax advantages: ordinary distributions are taxed at a 20% rate (Exhibit 5), and return on capital is achieved through depreciation and amortization.

Economic factors such as urbanization, a growing middle-class population, an aging population, and technological advancements can support real estate strategies.

Conclusion

Traditional portfolios with two brushes (stocks and bonds) have served investors well, but they may no longer be adequate in assisting investors in achieving their most important financial goals. It has become vital to provide asset allocation strategies beyond the two-brush approach, allowing our customers to possibly benefit from a more robust and sustainable portfolio. Maintaining a long-term strategic asset allocation in a multi-brush strategy, in our opinion, is the best method to preserve capital and avoid unnecessary flights to safety.

Footnotes

1Preqin

2TIAA CREF Center for Farmland Research, Standard & Poor’s, Federal Reserve, MSCI, Commodity Research Bureau, Consumer Price Index.

3Variant Investments

4 J.P. Morgan Asset Management, 2022 Long-Term Capital Market Assumptions

5 McKinsey Global Institute, October 2017 “Bridging global infrastructure gaps.”