July 2020

Investment Conditions & Outlook

Executive Summary

Despite concerns the COVID-19 pandemic remains as a yet-to-be conquered health and economic threat, financial markets continued their historic rebound in 2Q 2020.

In fact, the fastest 30% drawdown in the history of global markets in the first quarter of the year has now been followed by the largest 50-day advance in market history in the second quarter!

We don’t think investors have it wrong, but we are expecting a more volatile ride in the coming months. The unprecedented global monetary and fiscal stimulus have given investors a sense of confidence. As the investment saying goes, “don’t fight the Fed.” However, a more prudent look at the current status of the health and economic crisis and of market valuations (some hefty, some cheap) leaves room for both caution and opportunity.

Here are some highlights of what’s included within this report:

- An overview of the robust recovery in financial markets since late-March lows.

- 6 Truths about COVID-19 investing risks and how to navigate these cautionary conditions.

- 6 Macro Indicators we’re watching and their current “Favor Stocks” or “Favor Bonds” readings.

- The all-weather holdings/allocations we’re holding onto (with success) and the holdings/ themes we’ve recently added for defensive or offensive purposes going forward.

Up ahead (second half of year) are elections, potential pandemic second waves, and potential news of promising antivirals and vaccines. Also ahead is pent up demand, new recognized efficiencies/multipliers and an ongoing release of life enhancing and wealth creating innovations. The aim is to be postured for the good, the bad and the ugly. This is what investing from a position of strength is all about.

Investment Committee

Janiczek Wealth Management

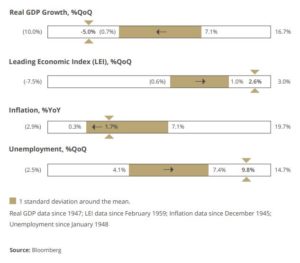

Economic Conditions and Top Takeaways

Key points

- U.S. economy had a solid foundation heading into COVID crisis and exogenous shocks, such as pandemics,

typically do not end business cycles (supports our overweight to U.S. equities versus benchmark). - The speed and magnitude of global monetary and fiscal policy response has been unprecedented and should

provide the foundation necessary to return to economic strength. - As the U.S. economy begins to see restrictions lifted across all 50 states, optimism is finally starting to come

back to the economy. - Unemployment spiked from historic lows to historic highs during the quarter, but now are trending back

down. Hiccups in the reopening of economies (due to more virus outbreaks) could lead to more economic

risks. Conversely, successful reopening’s with ample virus containment can lead to more economic upside

opportunities. - With a dovish fed, we expect interest rates to remain low helping to increase consumer confidence and

keeping housing market strong. - The 4-Year Election Cycle along with election polls and election final results adds another wild card dimension

to investing this year. The markets will price in pro and con expectations related to economic policy as

election polls (potentially unreliable) and results become known.

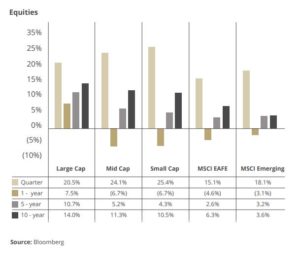

Equity Performance and Top Takeaways

Key points

- Exceptional double-digit performance across all large cap, mid cap, small cap, developed international and emerging market international stock indexes during 2Q 2020, as stock prices bounced off panic-sell lows reached in late March (late first quarter).

- U.S. stocks significantly outperformed international stocks. Our portfolios benefited by this trend as we purposely over-weighted U.S. stocks over international stocks in our portfolio designs.

- Mid Cap and Small Cap stocks outperformed Large Cap stocks in the quarter. Valuations of Small Caps are arguably much better than Large Caps. It will be interesting to see if Small Caps consistently outperform Large Caps in the next decade ahead due to this and other factors.

- As COVID-19 cases rise, many COVID-Impacted industries have declined. We are using six virus “truths” to evaluate the ability of industries to rebound: 1) Coronavirus is mainly transmitted by breathing someone’s air. 2) Poor ventilation increases the spread. 3) Wearing masks helps reduce the spread. 4) The virus is rarely transmitted by surface contact. 5) The virus is not going away soon. 6) A vaccine is not likely (and or widely distributed) until the second half of next year and beyond.

- Extend the above six factors out further and indoor (versus outdoor), poor ventilation (versus good), many people (versus few), no masks (versus wearing masks), close contact (versus distanced), and extended contact (versus brief) are the factors. In short, it will be a tough/longer road back for Airlines, Cruise Lines, Office REITs, and Indoor Entertainment industries because of these conditions.

- COVID-19 has accelerated some pre-existing trends like remote working, expanded geographic market footprint and faster/easier sales/service cycles via video conferencing, for example. This can/will help propel certain companies/industries going forward.

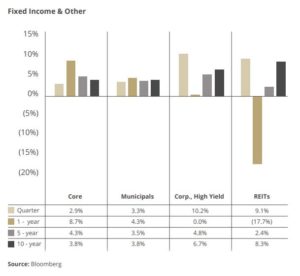

Fixed Income Performance and Top Takeaways

Key Points

- Investment Grade Corporate Bonds, Investment Grade Municipal Bonds and Corporate High Yield Bonds all bounced back with excellent performance in the quarter. Remarkably, high yield bonds substantially outperformed investment grade bonds during the quarter.

- Investors with decent bond portfolio exposures in 2020, of 35% to 50% or more, were likely to be pleasantly surprised by the diversification impact of such quality fixed income holdings during the pandemic. This remains an important lesson for ongoing prudent portfolio design.

- The disruption in fixed income pricing, due to record volume, supply/demand and spread issues during the pandemic panic period (mid/late March) was alleviated by rapid action by the Fed and Treasury. This action fueled robust fixed income returns. So did the continued flight to safety (heavy bond fund inflows).

- Tightening spreads in high yield and credit have continued to narrow and only adequately compensating investors for the likely rise in default rates in the coming months.

- Low inflation and dovish central banks should keep interest rates low during the recovery from lockdowns.

- We continue to favor investment grade corporate bonds instead of stretching for higher yields in the below investment grade credit markets.

- REITs rebounded in the quarter but are down significantly for the year as threats to real estate income flows and prices, particularly for hotel, retail and office space real estate, persist.

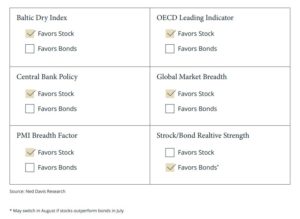

EBI (Evidence Based Investing) Perspective Advantage of the Quarter

Key points

- While threats of a second or even future third wave of the pandemic persist, we no doubt are seeing signs of an economic rebound as state after state, and country after country, open up more parts of the economy and pent up demand relieves itself.

- Presently, of six macro indicators we watch, five have turned to favor stocks over bonds. Not long ago, only two of the six favored stocks over bonds.

- For instance, the Baltic Dry Index recently turned positive for stocks as it recently registered its highest reading in history. While the coronavirus has continued to whipsaw this indicator, this shipping rate indicator now favors stocks (is bullish for equities/economic recovery).

- The Central Bank Policy is another macro indicator. Global short-term rates are in a downtrend.

- PMI Breadth is a third macro indicator we watch. This indicator now favors stocks as the four-week change in countries with expanding manufacturing entered positive territory for the first time since March.

- The OECD (Organization for Economic Cooperation and Development) Leading Indicator suffered its worst monthover-month decline in its history during May. It recently returned to positive territory for the first time since March.

- The Global Market Breadth indicator is showing over 85% of global markets trading above there 50-day moving average. It remains favorable for stocks.

- Finally, the Stock/Bond Relative Strength indicator, which has a heavier weighting than the other five, is the only indicator favoring bonds. If stocks rally relative to bonds in July, this indicator could turn favorable to stocks in August.

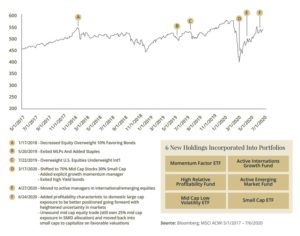

Overview of Select Portfolio Management Moves Made

- As stated in prior commentaries, we have been acting to de-risk portfolios from overweight equity and more aggressive equity or equity-like positions for the last 2-years plus. Simply put, we knew the bull market that began in March of 2009 (11+ years ago) was long in the tooth and we simply wanted more portfolio downside protection in the event of a correction.

- All-weather holdings and allocations we built well before and held onto throughout the pandemic have been Investment Grade bonds, Investment Grade Municipal Bonds, S&P 500 Stocks and Wide Moat, Heavy Dividend Paying Stocks. Not all dividend payers are created equal and we believe focusing high quality businesses will be additive to our portfolios in a slow growth environment.

- As the pandemic crisis unfolded, we acted to reduce small cap stock exposure (buying mid cap stocks with proceeds) and eliminate high yield bonds (increasing cash reserves in the process). This action was designed to own stronger balance sheet assets during the most uncertain time period of the pandemic crisis.

- While we liked owning index funds in many categories during the robust bull market run since 2009, we acted decisively to sell several index holdings and add active managers with high “active share” characteristics, “boots on the ground” and/or “factors” we like. Simply put, we believe this is a time to be more active and recent active versus index statistics are in support of this pivot.

- We are extremely excited about each of the new active holdings within portfolios and we think clients will be pleased with this exceptional line up (and the performance of these holdings year-to-date). Within this updated mix includes a Momentum Factor ETF, a Relative Profitability Factor fund, a Mid Cap Low Volatility ETF, an Emerging Market fund and a new Developed Market International fund.

- Call us at 303-721-7000 if you have any questions about these moves. We have solid due diligence and rationale behind each move/pick.

BONUS: Wealth Management Updates/Tips

- The Coronavirus Aid, Relief, and Economic Security (CARES) Act was recently put into law with several measures designed to stimulate the economy. One provision of the Act allows retirees and inherited IRA beneficiaries to forego taking Required Minimum Distributions (RMD) for tax year 2020 from IRA’s or other defined contribution plans.

- RMD amounts are calculated based on a life expectancy table from the IRS and the value of a retirement account as of 12/31 of the previous year. Those subject to RMD include original account owners who turned at least 70 ½ in 2019, those who turned age 72 under the SECURE Act in 2020, as well as inherited IRA beneficiaries of any age.

- If your retirement account encountered a decline in 2020, mainly due to the pandemic, a withdrawal could be a much larger percentage of your account. A new provision allows you to keep (or even return) funds in retirement accounts, potentially recapturing market losses when the economy rebounds. We highly recommend considering this tax reduction action.

- Regardless of when a retiree took their RMD in 2020, under new guidance from the IRS (Notice 2020-51), they can re-contribute the amount back into their retirement account as long as it is completed by August 31st, 2020.

- Unfortunately, a retiree can’t reverse the tax withholding of an IRA distribution. Those funds will stay with the IRS until the client files their 2020 taxes and will be factored into whether a refund will occur. When repaying/depositing back into one’s IRA account, the client can return the full gross amount of the RMD or the net amount they received.

- Contact your Janiczek Wealth Management team via email or call us at 303-721-7000 to review and discuss your situation in more detail.

Janiczek Wealth Management – At a Glance

To learn more about Janiczek Wealth Management, click here.

Important Disclosures

The content herein is to be used for informational purposes only. Neither Janiczek Wealth Management or its owners and employees represent or warrant the accuracy or completeness of the information contained in this report. In no event will Janiczek Wealth Management or its owners or employees be liable for any damages that may result from the use of or reliance on these materials.

Sources: Barron’s March 2020, 2019, 2018, 2017, 2016, 2015, 2014; Financial Times June 2017, 2015; AdvisoryHQ March 2018, 2017, 2016; Mutual Funds magazine January 2001; Worth magazine July 2002, January 2004, October 2004, October 2008. Please Note: Rankings and/or recognition by unaffiliated rating services and/or publications should not be construed by a client or prospective client as a guarantee that he/she will experience a certain level of results if Janiczek is engaged, or continues to be engaged, to provide investment advisory services, nor should it be construed as a current or past endorsement of Janiczek by any of its clients. Rankings published by magazines, and others, generally base their selections exclusively on information prepared and/or submitted by the recognized adviser. Rankings are generally limited to participating advisers.

Past performance may not be indicative of future results. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy (including the investments and/ or investment strategies recommended and/or undertaken by Janiczek® Wealth Management (“Janiczek®”), or any non-investment related services, will be profitable, equal any historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Janiczek® is neither a law firm nor accounting firm, and no portion of its services should be construed as legal or accounting advice. Moreover, you should not assume that any discussion or information contained in this document serves as the receipt of, or as a substitute for, personalized investment advice from Janiczek®. Please remember that it remains your responsibility to advise Janiczek®, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/ revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. A copy of our current written disclosure Brochure discussing our advisory services and fees is available upon request. The scope of the services to be provided depends upon the needs of the client and the terms of the engagement.

TM & Copyright Janiczek Wealth Management. All rights reserved. Do not reproduce or redistribute in any form without prior written permission. Strength Based Wealth Management® 35 Essential Strengths®, The Stages of Financial Freedom®, Wealth Optimization Plan™, Wealth Optimization Dashboard™, Lifestyle Protection Analysis™, Elastic Limit Wealth Threshold™, Flourish! Activators™, FLOURISH!™ and Flourish! Based Retirement Planning™ are all trademarks of Wealth with Ease, LLC. For details, call 303-721-7000.