April 2020

Investment Conditions & Outlook

Executive Summary

The global economy started the year stronger than we have seen in decades. Fresh off upbeat fourth quarter earnings, improved business sentiment and a freshly completed U.S./China (phase 1) trade deal. However, valuations and optimism in stocks were pretty high, causing us to maintain a disciplined stock/ bond mix (neutral weighting) and to de-risk underlying holdings for more downside protection in the event of a correction. What a difference a few months can make. The first quarter of 2020 will go down in history with a formidable black swan event (the COVID-19 pandemic) – and the stock market suffered its worst first quarter on record as social-distancing actions, to help mitigate the spread of the pandemic, wreaked havoc with unprecedented economic uncertainty, fear, layoffs (potentially short term) and disruption. Our message to clients, based upon years of proactive actions regarding the merits of “Investing from a Position of Strength,” is clear: 1) Weather the storm, 2) Prudently adapt where needed and 3) Don’t miss out on the significant deep-discount opportunities and robust rebound when it occurs. As always, our aim, with this report, is to give you a very brief but accurate lay of the land so that we can collaborate with you to successfully navigate this harsh storm and be in a good solid place with you when it subsides.

The Janiczek Team

Economic Conditions and Top Takeaways

Key points

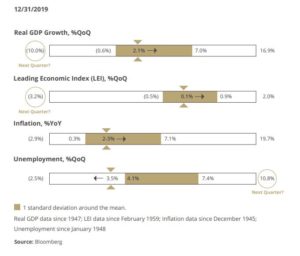

- As noted on the economic indicators below, all aspects of the economy were on solid ground coming into the COVID-19 pandemic crisis.

- The very actions to “flatten the curve” of the pandemic (a good thing) have broad and deep economic implications (a challenge) and this will severely impact the world economy during the second quarter and at least partially impact the economy into the third quarter of 2020.

- Investors are seeking to assess if a “V” recovery (rapid), “U” recovery (gradually building), “W” recovery (double dip/recovery) or “L” recovery (slow/ugly) is in our future. Nobody knows for certain, but governments, medical/pharma/biotech/health institutions, and businesses are doing their best to contain the crisis and orchestrate a robust recovery.

- Fiscal stimulus (upwards of $6 Trillion in the U.S.) has quickly been implemented into law and policy has been well received by investors. Further stimulus plans are also being considered, clearly telegraphing a “whatever it takes” response to this crisis.

- As this COVID-19 pandemic is ultimately controlled and innovations in testing, mitigating (antivirals) and/or preventing (vaccines) the virus ultimately come to market, the economy and financial markets will bounce back.

- We expect casualties (particularly in the most impacted industries) but also anticipate a gradual but everincreasing move back to most “business as usual” economic activities.

Equity Performance and Top Takeaways

Key points

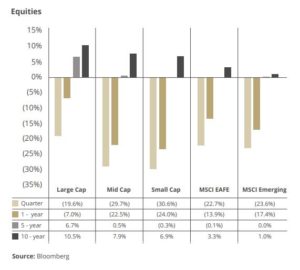

- Large-Cap U.S. stocks fared much better than Mid-Caps, Small-Caps and International Developed Stocks. Fortunately, when we de-risked portfolios in 2019, we over-weighted U.S. Large Cap stocks (and underweighted Global stocks), including overweighting the Consumer Staples sector, which was one of the best performing sectors.

- As the crisis unfolded, we quickly acted to reduce our Small Cap exposure, in portfolios where we held them, shifting holdings to Low Volatility Mid Cap and Large Cap Momentum strategies for more defensive purposes.

- Most of our portfolios are presently ~ 5% to ~ 10% underweight equities for defensive purposes and we plan to remain so until our bottom watch indicators flash a buy signal.

- Emerging Market stocks, ironically, held up relatively well during the crisis.

- Frankly, there were no places to hide in the equity markets. All 11 GICS sectors finished the quarter with double digit losses. The energy sector suffered its worst quarter since 1972, falling over 50%.

- We believe the market has already priced in significant economic damage. Accordingly, rebalancing portfolios at or near favorable panic prices is advisable for long term investors, particularly when/if signs of a four-step bottoming process are flashing a buy signal.

Fixed Income Performance and Top Takeaways

Key Points

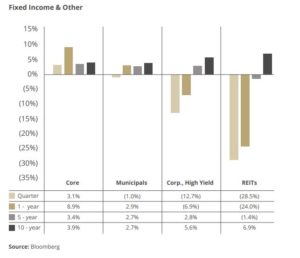

- Fortunately, our portfolios are constructed with a number of high-quality investment grade fixed income instruments which have greatly reduced overall portfolio volatility during this crisis. The level of this volatility control is proportionate with each client’s individually selected stock/bond mix.

- The flight to quality boosted treasuries (long term Treasury Notes appreciated as much as 20%).

- Early in the crisis, supply and demand inconsistencies caused dealers to slightly discount investment grade corporate bond and municipal bond prices. However, the Fed and Treasury quickly stepped in to guarantee liquidity and the bond markets rapidly recovered from this temporary anomaly.

- High Yield bonds depreciated in value due to the threat of increased default. As another precautionary step, we sold out of our small position in High Yield bonds and placed sale proceeds in cash for defensive purposes and to be ready for a potential rebalance move.

- The Fed has provided a backstop for investment grade issuers, increasing the incentive to keep investment grade status. We continue to favor financially strong investment grade issuers.

Evidence Based Investing (EBI) Perspective Advantage of the Quarter

Key Points

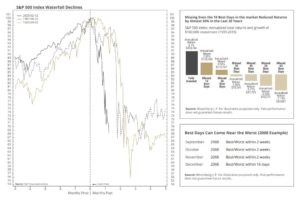

- The rapid decline in stock values in March 2020 is called a waterfall decline. In 18 days, the decline was the fastest on record from a record high to a bear market. The left portion of the chart below illustrates just how fast and steep this decline was compared to waterfall declines in 1929 and 1987.

- In the 18 times the S&P 500 has dropped 15% or more in one quarter, it has climbed the next quarter 67% of the time by a median of 5.8%. One year later, the median gain is 17.3%.

- An historic assessment of waterfall declines and bear markets in general reveals a prevalent four-step bottoming process: 1) Oversold selling climax; 2) Rally (bounce(s)); 3) Retest (70% of the time with lower lows) but with less total volume, less downside volume, fewer stocks making new lows and fewer stocks below their moving averages) and 4) Breadth Thrusts (broad increases across stock types/classes).

- Note that the market can bounce from step 2 to 3 several times, but if several breadth thrust indicators fire bullish signals, we will seriously consider a partial or full rebalance move (increase equities back towards or to full target weight from present underweight levels).

- It is certainly possible that the sell climax low was already hit on March 23 (S&P 500 = 2213). In reviewing numerous valuation analysis and assessments by other respected analysts, when the S&P 500 bounced back up to 2600, we assessed what possible downside retests may look like. Whether it is a -5% retest (to 2470), a -10% retest (to 2340) or a dire -17% retest (to 2158 or lower), it is too speculative for long-term investors, in our expert opinion, to attempt short term market timing moves and potentially miss out on robust rebound days (see right side of chart below). Rather, the long-term investors focus should be to 1) weather the storm, 2) adapt/tweak where needed, 3) rebalance when/if bottoming signals (and virus containment possibilities) flash a buy and 4) don’t miss out on significant deep-discount opportunities and a robust rebound when it occurs (which can be at any time).

- Out of caution for the unknowns and the high possibility of a variety of negative news (arguably already priced in, but not for panic sellers) on several fronts, we have elected to wait to rebalance until our bottom watch indicators flash buys and, hopefully, more news about virus containment, cures and economic revival hits the news cycles. If we miss out on rebalancing due to too small/short a window, we still participate in the recovery at a fine level. Given risk/reward dynamics and the typical profile of our clients, we believe this is the best approach at this time. Let us know if you would like to discuss or implement a different approach.

Below, we outline the key components of the current plan, and we will continue to monitor developments. In the quarter ahead, we will be working closely with clients who elect to act on specific tax planning tactics before year-end.

Janiczek Wealth Management Updates/Reminders

- We are pleased to announce that, earlier in the quarter, we were honored to be named to the Barron’s Top Advisors list (7th year in a row) and the Forbes Top Advisors list. This adds to our long list of accolades earned in the last two decades*

- We released the all new www.janiczek.com website, complete with numerous resources on building optimal levels of financial strength, agility, flexibility and endurance, plus numerous smart investing resources.

- We published three retirement guides, all available at www.janiczek.com: 1) How to Properly Prepare for Retirement, 2) How to Properly Transition to Retirement, 3) Now Retired, Now What? Each guide provides best practice tips on maximizing freedom of time, money, relationship and purpose.

- Much of this quarter has been dominated by actions to respond to quickly changing economic and investment conditions related to the COVID-19 pandemic. Our team has been focused on broad actions (to help all clients) and specific needs on a client by client basis. Let us know if you have any special needs to address and stay safe. All any of us can do is to make the most of the circumstances.

* see important disclosures at back of document.

Janiczek Wealth Management – At a Glance

To learn more about Janiczek Wealth Management, click here.

Important Disclosures

The content herein is to be used for informational purposes only. Neither Janiczek Wealth Management or its owners and employees represent or warrant the accuracy or completeness of the information contained in this report. In no event will Janiczek Wealth Management or its owners or employees be liable for any damages that may result from the use of or reliance on these materials.

Sources: Barron’s March 2020, 2019, 2018, 2017, 2016, 2015, 2014; Financial Times June 2017, 2015; AdvisoryHQ March 2018, 2017, 2016; Mutual Funds magazine January 2001; Worth magazine July 2002, January 2004, October 2004, October 2008. Please Note: Rankings and/or recognition by unaffiliated rating services and/or publications should not be construed by a client or prospective client as a guarantee that he/she will experience a certain level of results if Janiczek is engaged, or continues to be engaged, to provide investment advisory services, nor should it be construed as a current or past endorsement of Janiczek by any of its clients. Rankings published by magazines, and others, generally base their selections exclusively on information prepared and/or submitted by the recognized adviser. Rankings are generally limited to participating advisers.

Past performance may not be indicative of future results. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy (including the investments and/ or investment strategies recommended and/or undertaken by Janiczek® Wealth Management (“Janiczek®”), or any non-investment related services, will be profitable, equal any historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Janiczek® is neither a law firm nor accounting firm, and no portion of its services should be construed as legal or accounting advice. Moreover, you should not assume that any discussion or information contained in this document serves as the receipt of, or as a substitute for, personalized investment advice from Janiczek®. Please remember that it remains your responsibility to advise Janiczek®, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/evaluating/ revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. A copy of our current written disclosure Brochure discussing our advisory services and fees is available upon request. The scope of the services to be provided depends upon the needs of the client and the terms of the engagement.

TM & Copyright Janiczek Wealth Management. All rights reserved. Do not reproduce or redistribute in any form without prior written permission. Strength Based Wealth Management® 35 Essential Strengths®, The Stages of Financial Freedom®, Wealth Optimization Plan™, Wealth Optimization Dashboard™, Lifestyle Protection Analysis™, Elastic Limit Wealth Threshold™, Flourish! Activators™, FLOURISH!™ and Flourish! Based Retirement Planning™ are all trademarks of Wealth with Ease, LLC. For details, call 303-721-7000.