January 2020

2020 Investment Conditions & Outlook

Cautious optimism in the face of a steady Fed, increased global economic growth, stretched equity valuations and elevated geopolitical uncertainty around elections, disputes and trade wars.

“Approaching investing with a conscientious, explicit and judicious use of current best evidence can be a relief. This is why we manage portfolios via a highly disciplined approach called Evidence Based Investing (EBI).”

“EBI seeks to filter through noise, information, hype, and emotion in order to make reasoned investment decisions void of as much Investor Behavior Penalty as possible.”

Kyle W. Kersting, CFA, CAIA

Managing Director of Investments,

Janiczek Wealth Management

Executive Summary

2019: A Banner Year for Stocks & Bonds

We enter 2020 with stocks and bonds ending both a banner year and a banner decade. Easy monetary policies, continued economic growth, continued corporate profitability and strong employment and consumer spending led to the strongest cross-asset class gains since 2009.

All nine Russell style boxes posted 20%+ gains. All seven major regions and 10 of 11 sectors gained at least 18%. 82% of all central banks’ last moves were cuts, with the Fed cutting rates three times, helping bond total returns as well.

2020: A Mix of Reasons to be Cautiously Optimistic

We remain bullish on equity markets, albeit cautiously so. The economy is still adapting to lower tax rates and accommodative policies. High employment and consumer spending levels continue to point to global economic growth. We expect interest rates to remain low, within a modest trading range, and banks are flush with cash to finance qualified buyers.

But we are not expecting a knockout year. Stretched equity valuations and elevated geopolitical risks have compelled us to take positions that can participate in upside moves, but can have better downside protection should a correction emerge.

Here’s key highlights from points made inside this report:

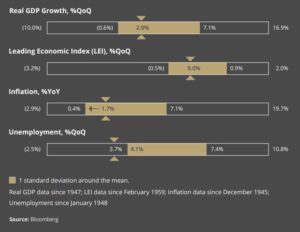

- Global real GDP growth in 2020 is projected to be 3.3%, up from a projected 3.0% in 2019.

- Four cycles should drive the stock market in 2020: economic, earnings, Fed and election.

- There exists a high bar for Fed action. Thus, Fed likely to remain on hold over intermediate term.

Reasons to Remain Cautiously Optimistic in 2020

Key points

- Although we are entering 2020 on solid ground, several issues are at critical junctures that could alter the way the year unfolds. Stretched equity valuations and the unknowable impact of the trade war, geopolitical influences and our own election continue to be wildcards that could cause us to revise our assumptions.

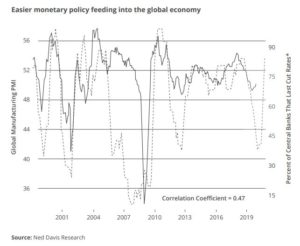

- Global real GDP growth in 2020 is projected to be 3.3%, up from a projected 3.0% in 2019. This modest increase supports the global equity markets through the new year. We expect global monetary policy to remain accommodative with the Fed on hold after 3 rate cuts and the European Central Bank engaging in quantitative easing, with the possibility of more stimulus to come. The lessening fear of a hard Brexit from the European Union supports a continued recovery of the Eurozone through 2020.

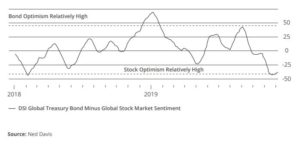

- The fear of missing out (FOMO) has resulted in investors favoring equities over bonds. This optimism towards equities and pessimism towards bonds can be interpreted as concerning. This economic optimism has yet to be confirmed and could lead to a pullback from currently

stretched valuations.

Four Key Cycles to Watch in 2020

Key Points

Four key cycles could set the backdrop for the S&P 500 to post back-to-back double-digit gains for the first time since 2013-14, if geopolitical or another wildcard does not interfere with the trajectory.

U.S. Economy: We believe the economy will avoid a recession

- Real GDP growth to slow (to 1.8%) given uncertainties, but will avoid recession

- Capex and manufacturing activity set to stabilize, and consumer spending will continue

- Inflation to remain muted due to pace of job creation and historically low unemployment

Earnings: Earnings growth remains near 2019 levels

- Modest growth similar to the past year of 6.0%

- Neither pending impeachment nor coming election should seriously impact corporate earnings

- Real GDP growth should remain positive for the year with stabilizing global growth

Fed: Remains dovish 2020

- Yields range bound to modestly higher could lead to headwind for fixed income

- Fed to remain on hold for intermediate term

- Favor credit and corporate bonds while spreads remain tight

Election:

- Impeachment or not, there will still be a Presidential election in November 2020

- Markets historically are choppy the first half of an election year and strong in the second half of the year when uncertainty diminishes (see chart which 1/3rd is weighted by Four-Year Presidential Cycle)

- Markets could experience short lived sell-off if it predicts the election of candidates seeking significant tax and regulatory changes that can negatively impact current economic trajectory

“When we overlay this chart onto what actually unfolds in 2020, we have one more important input to help us assess risks and opportunities – including potential over-reactions and under reactions to other timely inputs.”

Joseph J. Janiczek, MSFS, CHFC

CEO

Janiczek® Wealth Management

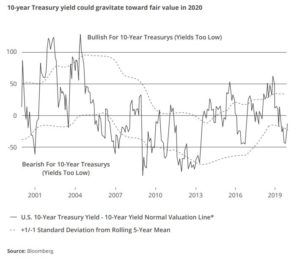

Bond Yields to Remain Flat to Modestly Higher

- 10-year Treasury yield could gravitate toward fair value in 2020 (see chart) resulting in potential short-term headwind for fixed income

- Fed should remain on hold for intermediate term and low inflation will make any rate hikes difficult to justify

- Global liquidity at favorable rates will support purchasing of risky assets resulting in uptick of yields

- Strong gains from equities will support rebalancing of portfolios into fixed income assets helping to keep yields range bound

- Conditions for corporate credit generally remain favorable even with rich valuations and tight spreads

Our Bullish Case for Equities

Key Points

- We expect U.S. equities to be supported by positive earnings growth and benefit from continued de-escalation in trade policy

- Volatility should be expected during an election year, but we still believe stocks can benefit from a trade deal and strong U.S. economy

- Eurozone stocks could close valuation gap with domestic peers given positive progress on Brexit

- Emerging markets could benefit from further progress made between the U.S. and China

Economic Landscape is Solid, Albeit Continued Slow Growth

Key Points

- U.S. real GDP growth to slow to 1.8%, from 2.0%

- The all-important U.S. consumer will likely provide continued support given steady wage growth and a paused Fed

- We continue to view odds of a recession being relatively low for 2020

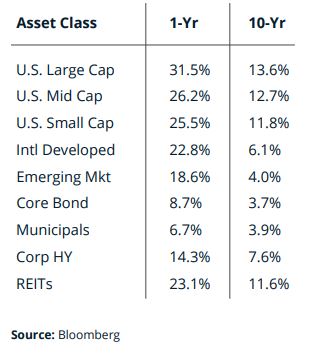

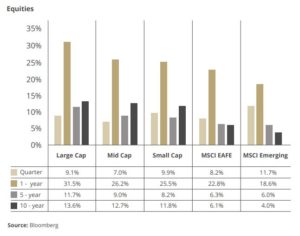

A Broader Look at Equity Market Performance Highlights Key Trends Over the Last Year and Decade

Key Points

- In the last year, the S&P 500 posted its biggest gain since 2013 and second-best year since 2000

- A year ago, investors were pricing in policy mistakes (all the unsubtantiated rate hikes in 2018) teeing up 2019 for the impressive turnaround

- 10 out of 11 sectors gained at least 18% in 2019, Energy (7.6%) was the exception

- Overweighting U.S. over International Developed and Emerging Markets has paid off for the last decade with signs (note EM latest Quarter) this trend may shift in the year ahead

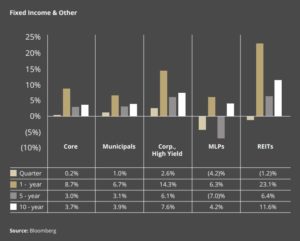

A Broader Look at Fixed Income Performance Shows the Impact of the Fed and Worldwide Central Banks’ Pivot in 2019

Key Points

- The U.S. bond market had its best year in 17 years

- Boasting double-digit gains, corporate bonds had the best sector returns

- The U.S. fixed income market beat other major fixed income markets (not shown) in both local currencies and U.S. dollar terms

- MLPs, which boast high single to low double-digit yields, continued their volatile ways (we exited our small position halfway in year when they were up for the year substantially)

- REITs, which are in the S&P 500 as an equity sector, advanced nicely in 2019 and boast impressive decade-long double-digit performance

How to Lever Our Clarity Sessions & Advanced Portfolio Monitoring & Trading Systems in 2020

Key Points

- We encourage all clients to fully participate in Clarity Sessions with us in 2020 with all visual tools and aids available. In 2019, we received an average rating of 9.86 (scale of 1 lowest to 10 highest) from clients regarding the quality of our Clarity Sessions.

- In 2019, we upgraded all conference rooms and board rooms to “Zoom Rooms” so clients located anywhere in the world could see us and various graphs, charts and dashboards helpful in understanding strengths, weaknesses, opportunities and threats and what to do about them. Our team proactively schedules these sessions with clients semi-annually.

- Our Advanced Portfolio Monitoring & Trading System gives us instant access to monitor, service and trade client accounts on a single client basis as well as an all client basis. Various tactical trades and tilts we made in 2019 were executed in minutes across all clients.

Janiczek Wealth Management – At a Glance

To learn more about Janiczek Wealth Management, click here.