The 1031 exchange has been a popular real estate investment tool for investors who wish to defer capital gains on the sale of real estate. As of late, the 1031 exchange has come under attack by the Treasury’s Green Book. The current proposal imposes a $500,000 per person limit on the aggregate amount of gain deferral for each year.

Furthermore, while the 1031 exchange is an effective tax mitigation strategy, the 1031 exchange fails to meet the goals of all investors. To be fair, some investors only want the benefits – stable income, tax benefits, and potential appreciation – and none of the responsibility of managing their real estate property. By not taking the 1031 exchange route, an investor is dealt with the option of selling the property and paying taxes on any deprecation recapture.

With these two points in mind, let us introduce the 721 exchange.

A section 721 exchange, or otherwise known as an “UPREIT”, allows an investor to exchange property held for investment or business purposes for shares in a Real Estate Investment Trust (REIT) or Operating Partnership which can remain in the Operating Partnership or eventually be transferred, tax-free, to a REIT.

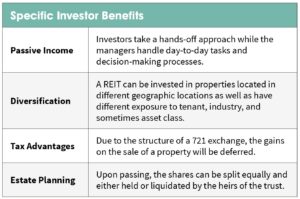

Investor Benefits

The 721 exchange offers benefits in four key areas in your financial picture.

As a real estate property owner, an individual needs to perform daily management efforts to keep cash flows consistent. Selling the property and acquiring shares of a REIT, which are passive in nature, allows investors to collect passive income.

On top of no longer managing your property, REITs can provide a plethora of diversification benefits. A REIT’s investment universe is vast. Investment properties can range in various exposure to geographic locations, tenants, and industry.

With the Treasury’s Green Book in mind, tax and estate planning strategies are becoming a topic of interest. The 721 exchange empowers investors to use 100% of the gains on a sale to purchase shares of a REIT – deferring all capital gains tax to a later date.

Furthermore, physical real estate often presents hurdles when selling, and it can lead to conflicts in the division of assets. Conversely, the 721 exchange will allow an investor to receive all the benefits during their lifetime; upon passing, the heirs will receive divisible REIT shares. These shares can be held or liquidated.

So, if you liked 1031s, you are loving 721s. However, investors cannot entirely throw out the 1031 exchange.

REITs have specific acquisition criteria, and, likely, a property does not meet the REIT criteria. There is a solution: combine a 1031 exchange with a 721 exchange. This combination will allow an investor to acquire a fractional interest in institutional-grade property that meets the criteria of the REIT.

The investor needs to hold this fractional investment for enough time (typically around 12-24 months) to keep the 1031 exchange intact. The good news is that the investment may pay dividends throughout this period. After this point, the fractional investment is eligible to be contributed to the REIT in exchange for operating partnership units. These units are exchangeable for direct ownership of shares in the REIT.

Something to Note

Though the 721 exchange presents many planning opportunities, the REIT shares are not exchangeable in a 1031 exchange. A completed 721 exchange is the end of the road for deferral of capital gains tax. If REIT shares are sold, or the REIT sells a portion of the portfolio and returns capital to the investors, the investors will be required to recognize any capital gain or loss when they file their taxes.

Janiczek Wealth Management is keeping abreast of the legislature developments coming out of Washington D.C., and we will continue to find planning and investment opportunities to fit our client’s needs. If you are interested in learning more about our comprehensive wealth and investment management services, please contact Cathy Wegner, Director of New Client Engagements, 303-339-4480 or cwegner@janiczek.com.

The content herein is to be used for informational purposes only. Neither Janiczek Wealth Management or its owners and employees represent or warrant the accuracy or completeness of the information contained in this report. In no event will Janiczek Wealth Management or its owners or employees be liable for any damages that may result from the use of or reliance on these materials. Janiczek is neither a law firm nor an accounting firm, and no portion of its services should be construed as legal or accounting advice. We recommend that anyone reading this material consult their CPA and estate planning attorney regarding these matters. Moreover, you should not assume that any discussion or information contained in any Janiczek published work, whether in digital form or otherwise, serves as the receipt of, or as a substitute for, personalized investment or financial advice from Janiczek.