Determining a sustainable withdrawal rate in retirement is, of course, not a new concept. Many are aware of the “4% Rule,” but a quick Google search would lead you to assume it is no longer a viable strategy in retirement planning.

Allow us to provide a brief review of this rule for those who are unfamiliar with it. The 4 % Rule states that retirees should not outlive their retirement account if they limit their first withdrawal to 4% of their portfolio or less. Withdrawals in following years would subsequently be adjusted to account for inflation.

William Bengen proposed the 4 % rule in 1994, and the amount and pace of subsequent research has risen over time. Each subsequent study, article and white paper approached the 4 percent rule in a slightly different way.

Janiczek Wealth Management has successfully assisted hundreds of clients in withdrawing funds from their portfolios to pursue life’s next opportunity. Janiczek has long advised a withdrawal rate of “3.9 percent or less” to our clients.

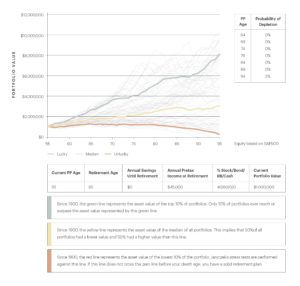

We use a robust scenario analysis to analyze the possibility of success of this claim, taking into account real market performance and inflationary cycles dating back to 1900. We do not, however, use historical average rates of return (more to come on this). Instead, we think about what would have happened if you had retired in 1900, 1901, 1902, and so on. The frequency with which your strategy would have worked in the past is then computed. The graphic on the right displays the result and offers more information about what you’re looking at.

While Janiczek Wealth Management acknowledges that previous performance is no guarantee of future performance, establishing a retirement plan that incorporates black swan events from the past can better prepare you for a successful retirement.

As Mark Twain said, “History never repeats itself, but it does often rhyme.”

A Monte Carlo simulation, a popular industry tool, relies on an assumed distribution curve of random events. While the outcome is subject to varying degrees of randomness, you must nevertheless estimate the average growth rate. Assuming average growth and then adding randomness does not provide a realistic model for long-term market behavior since it causes the model to “forget” about black swan events.

Assume your retirement plan has withstood the worst effects of inflation, the Great Depression, and every other financial catastrophe that the United States has faced since 1900. In that case, it will most likely survive whatever happens between now and the day you no longer require your money. Janiczek believes that employing this method provides our clients with the most confidence in their ability to maintain their retirement lifestyle.

If you are interested in a second opinion regarding your financial picture during the next phase in life, please contact Cathy Wegner, Director of New Client Engagements, at 303-339-4480 or cwegner@janiczek.com.