Our January 2022 commentary anticipated positive returns with more volatility for the following year. So far, the latter is accurate. Higher interest rates and inflation were the most likely explanations for this implied volatility, but geopolitical developments in Ukraine have now entered the equation. Looking at the news headlines might help investors find pundit ‘answers’ that match their narrative: 16 European Stocks That Might Just Withstand the Russia-Ukraine Crisis1, Wall Street ends sharply lower as Ukraine crisis sows fear2, and The invasion of Ukraine changed everything for Wall Street3. Nobody in the media can predict what will happen. It is wise to mute them as best as possible.

In the short run, it’s difficult to see an easy way out of the current geopolitical nightmare. The outcome is not predetermined, and the situation evolves rapidly, but we can look to the data to provide some context.

Economic Perspective

Looking just at direct economic concerns, the Russian invasion should be minimal. The Russian economy accounts for just approximately 1.7% of global GDP, while Ukraine accounts for about 0.2% of global GDP4. Furthermore, US exports to Russia were just $8.9 billion in 2020, accounting for 0.4% of total US exports, and mainly comprised of capital goods, financial services, and industrial supplies and materials. Russia’s imports were $18.2 billion, or 0.6% of total US imports, primarily concentrated in industrial supplies and materials. Because of the modest amount of US trade with Russia, the impact on the US economy is negligible.

The source of worry is the indirect consequences of Russia’s role as a major energy provider to the world, particularly to Europe. The United States’ exposure is still considerably limited because the country imports no natural gas from Russia and is a net exporter of natural gas to the rest of the world. The United States presently imports oil from Russia, although the amount is minor compared to other suppliers. According to the American Fuel and Petrochemical Manufacturers (AFPM) trade association, the United States imported 209,000 barrels per day (BPD) of crude oil and 500,000 BPD of other petroleum products from Russia in 2021. Russia crude accounts for just 3% of US oil imports and around 1% of total crude oil processed by US refineries5.

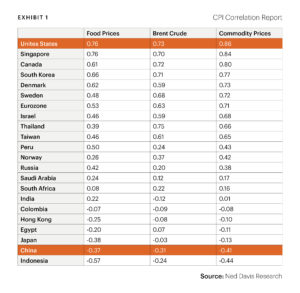

The most significant impact we anticipate seeing is on inflation. According to Ned Davis Research, there is a correlation between commodity prices and CPI in most of the world’s economies. It is shown in Exhibit 1. The February inflation rate will not be updated until the March 10th CPI release. The January inflation rate of 7.5%, on the other hand, was the highest since 1982. Higher energy prices accounted for a large portion of the rate increase. Many analysts projected that the energy price would begin to fall as spring approached and supply chain issues eased. However, the war adds an element that likely sustains higher energy prices for a longer time and probably keeps inflation more elevated than it should be.

shown in Exhibit 1. The February inflation rate will not be updated until the March 10th CPI release. The January inflation rate of 7.5%, on the other hand, was the highest since 1982. Higher energy prices accounted for a large portion of the rate increase. Many analysts projected that the energy price would begin to fall as spring approached and supply chain issues eased. However, the war adds an element that likely sustains higher energy prices for a longer time and probably keeps inflation more elevated than it should be.

Capital Markets Perspective

Looking at major global equity markets, the S&P 500 was down 2.66% in February and 8.68% year to date. International and emerging market equities were also down, but they are still ahead of US markets year to date. As represented by the iShares MSCI Russia ETF (ERUS), Russia is down roughly 81% so far this year. Trading has also been halted.

Russia has been proposed to be removed from the MSCI indices. Russia’s withdrawal is relatively painless because they account for only 1-2% of traded world equities. Russia is weighted at 3.24% in the MSCI emerging market index. Janiczek portfolios were underweight the emerging market space entering 2022.

Markets have grown even shakier due to Russia’s invasion of Ukraine. While global uncertainty might cause markets to fall, historically, there have been temporary drops until investors can re-forecast their expectations. Exhibit 2 demonstrates this.  The average total return six months after the event is 5%, and the average total return one year later is 9%. Furthermore, looking back at 54 crisis episodes since 1907, Ned Davis Research found that the Dow fell by an average of -7.1% throughout the crisis period6.

The average total return six months after the event is 5%, and the average total return one year later is 9%. Furthermore, looking back at 54 crisis episodes since 1907, Ned Davis Research found that the Dow fell by an average of -7.1% throughout the crisis period6.

The point of showing this is not to indicate that we should try to time the market but rather to show that the uncertainty of the related event often induces market dislocation. Market dislocations usually resolve if that uncertainty is addressed, and market participants can make estimates using revised assumptions.

Closing Remarks

First and foremost, we wish for the best for the Ukrainian people and a swift and peaceful end to the hostilities.

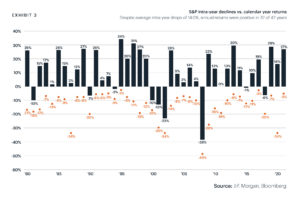

Exhibit 3, a client favorite from our Q1 ’22 Clarity Sessions, compares S&P intra-year declines against calendar year returns. The important thing is not to extrapolate and jump to conclusions.  The markets are off to a poor start this year, but every year from 1980 to the present has seen some degree of drawdown on an intra-year basis. What you’ll notice is that 32 of the 42 years ended the year in positive territory. With that said, we recommend to our clients that they keep these three points in mind:

The markets are off to a poor start this year, but every year from 1980 to the present has seen some degree of drawdown on an intra-year basis. What you’ll notice is that 32 of the 42 years ended the year in positive territory. With that said, we recommend to our clients that they keep these three points in mind:

- Stay true to the high standards of excellence built into our Strength Based Wealth Management system; they are intended to help you weather storms and capitalize on opportunities that arise as a result of such frightening times.

- Let our Evidence Based Investing, which includes rebalancing procedures and factor tilts, work for you. These strategies are intended to withstand such volatility and capitalize on opportunities that arise as a result of it.

- Participate in a semi-annual Clarity Session with us. This is when we provide our most recent thoughts on strengths, weaknesses, opportunities, and threats, as well as how we can collaborate and act in unison based on your specific circumstances.

Footnotes

1 https://www.barrons.com/articles/european-stocks-russia-ukraine-crisis-51646037107

2 https://www.reuters.com/business/futures-fall-russia-ukraine-crisis-escalates-2022-03-01/

3 https://www.cnn.com/2022/02/27/investing/stocks-week-ahead/index.html

4 https://www.imf.org/en/Publications/WEO/weo-database/2021/October/weo-report

5 https://www.afpm.org/newsroom/blog/oil-and-petroleum-imports-russia-explained

6 Ned Davis Research, March 2022, Crisis Events, DJIA Declines And Subsequent Performance