October 2020

Investment Conditions & Outlook

Executive Summary

The global equity markets remain in the early recovery phase of the business cycle that started in the second quarter of this year following the short lived COVID-19 recession. The aftermath of the recession can still be felt, but we are pleased with the economic and market recovery we have experienced thus far. This is now two quarters in a row with strong gains across global equites, led by the U.S.

To support the continued recovery, we expect an extended period of low-inflation and low interest rate environment: one that typically favors stocks over bonds. But after such a rapid recovery and with the threat of COVID-19 pandemic interruptions persisting, and election related concerns front and center, an equity market pullback would not be surprising. Accordingly, we continue to believe defensive and/or hedged equity positions – like the ones we engineered into most of our portfolios – have their place at this time.

We currently see the markets as primed for a rotation from tech/growth leadership and into cyclical/value stocks. This also implies a rotation from heavily valued U.S. stocks into international developed and emerging markets, but we presently own more U.S. securities than benchmark weights, for defensive purposes.

While elevated economic and market risks persist, we believe positive COVID-19 vaccine and anti-viral developments, dovish central banks, and stimulus-minded politicians can continue to positively influence the recovery, with noted exceptions and risks prudently curbing our enthusiasm at this time.

See inside for more details on the conditions that support this commentary.

Investment Committee

Janiczek Wealth Management

Economic Conditions and Top Takeaways

Key points

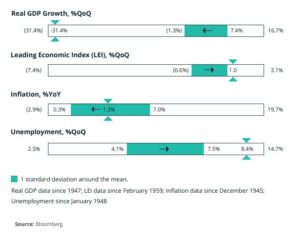

- Global economic conditions have improved substantially from the short but ugly COVID-19 pandemic induced global recession. Our Global Recession Watch indicator moved from a high risk range all summer long to the low-risk range just a few weeks ago. This is not an all clear sign, but a healthy development.

- During the quarter we saw inflation rise 1.3% in the 12-month period. Inflation has averaged 1.6% over the past decade, giving the Fed plenty of room to leave Fed funds rate unchanged at historic lows – tailwind for equities.

- Current ultra-low borrowing cost makes high levels of debt for governments more sustainable as interest paid on debt is lower than the growth rate trend of nominal GDP.

- Unemployment continued to improve during the quarter, supporting the economic recovery.

- The main risks are mostly unchanged from last quarter: an extended second or third wave of COVID that causes renewed lockdowns and disruptions, and the wild card of the November U.S. elections.

Equity Performance and Top Takeaways

Key points

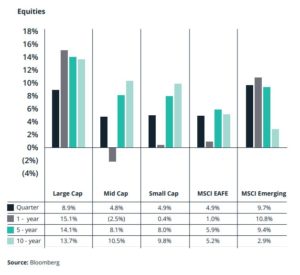

- The third quarter saw continued strength in global equity returns from March lows. Emerging Markets outperformed the rest of the world in 3Q20. We are very pleased with our Emerging Market holdings and managers.

- Rebounding global indices have brought 1-year numbers back into the positive, except for Mid Cap stocks sporting a minor loss.

- We have seen the return of the S&P 500 dominated by top 5 tech companies that makes up 25% of index. This condition requires special attention as valuation indicators are quite different between the top 5 stocks (arguably expensive) and the other 500 (arguably fair valued).

- We continue to favor U.S. to International equities due to more defensive posture of our portfolios but see upside potential in our International exposures as they continue to be undervalued when compared to U.S. counterparts.

- China’s early exit from the lockdown and stimulus measures should continue to support a recovery.

- The upcoming election is a noted wild card that we have and will continue to factor into investment allocations at an appropriate level. The market is pricing in various risk/reward considerations of elections at all times and if/when markets underreact or overreact, we seek to take advantage of such opportunities. This election cycle we’ve done a lot to prepare for the possibility of increased taxation in the future and will be reviewing with clients how “active tax management” will increasingly play a role in our value-added portfolio management approach into the future.

Fixed Income Performance and Top Takeaways

Key Points

- Investment grade, municipal and high yield bonds had another stellar quarter fueled by decrease in interest rates and low inflation. We continue to be very pleased with our bond holdings across the board.

- High yield continued to outperform, bouncing back from March lows. Spreads continue to narrow, only adequately compensating investors for the likely rise in default rates following the recession.

- Government bonds remain a safe haven for investors but are becoming expensive. Low inflation anddovish central banks should limit a rise in bond yields going forward

- Real estate investment trusts (REITs), which we do not explicitly own, sold off heavily in March due to concerns about the implications of social distancing. We feel sentiment is overly bearish and the asset class could offer good value post recovery. This said, we do not presently plan to explicitly allocate funds to this asset class at this time and typically prefer private real estate deals for high net worth clientele open to the pros and cons of such holdings.

- We continue to favor high quality corporate bonds and municipal bonds. The possibility of increased taxation could increase the demand for municipal bonds if a significant change in tax policy occurs in 2021 and beyond.

EBI (Evidence Based Investing) Perspective Advantage of the Quarter

Key points

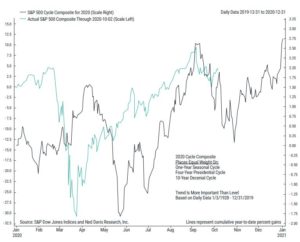

- Here is exactly what we said in January 2020 when we posted the below S&P Cycle Composite without any actual results shown for the year: “Equity markets are historically choppy the first half of an election year and strong the second half of the year when uncertainty diminishes. This chart, weighted 1/3rd by the Four-Year Presidential Cycle, 1/3 by the One-Year Seasonal Cycle and 1/3 by the 10-Year Decennial Cycle illustrates what the trend for the year may look like for equities. When we overlay this chart onto what actually unfolds in 2020, we have one more important input to help us assess risks and opportunities – including potential over-reactions and under-reactions to other timely inputs.”

- The below chart now includes the overlay of actual S&P 500 Composite data through 10/02/2020. This illustrates how the COVID-19 pandemic crisis abruptly interrupted the normal trend (as one would expect) in March. However, it also illustrates how various economic stimulus actions and perceived investor buying opportunities methodically put the trend back on track through the summer.

- Looking ahead, uncertainty around the election and other seasonal factors tends to be a drag on the market (trend is more important than level) a short while until election and seasonal uncertainty is exhausted and then trends upwards again.

- Please note: this chart is not our forecast nor is it a market timing tool. It simply is a useful reference point to assess potential over or under reactions to other inputs. In January 2021, we will repeat the process for 2021 and utilize it as one of many reference points as we continually assess new threats and opportunities.

- Regardless of who wins the elections, we believe tax-smart investing and tax-smart wealth management will play an even more significant role in the years ahead. In fact, after the election results are in, a variety of legal, moral and ethical tax strategies should be considered by all clients. We have invested considerable time and money into resources to help clients engage in more tax-smart investing and more tax-savvy proactive planning. More to come on these opportunities in the months ahead.

Janiczek Wealth Management Updates/Reminders

- Mortgage rates have declined to historic lows. We continue to encourage and help clients refinance real estate debt, often with rates 1% or more lower than what they had locked in from previous low points. This is allowing us to help clients improve non-discretionary expense ratios and debt to equity ratios to well within our standards. Make sure to take advantage of this superb refinance environment while this extraordinary refinancing window is open.

- Required Minimum Distributions (RMDs) are not required in 2020. The CARES Act was passed into law allowing individuals to forego taking RMDs this year if they do not need the distribution. While the deadline has passed to re-deposit distributions (deadline was August 31st), clients can still opt out of taking any remaining withdrawals through the end of the year to reduce their ordinary income tax bill. We have helped many clients subject to RMD reduce their 2020 tax liability by utilizing this special tax code.

- Qualified Charitable Gifting (QCDs) for individuals over 70 ½ is still an option. Even though RMDs are not required this year, one can still choose to make a gift from their IRA through the QCD strategy (up to $100,000) without incurring any tax. There are different factors to consider on whether it makes sense to make a QCD gift from an IRA in 2020 or defer until 2021 when QCDs have the effect of reducing taxable income. This may still be a great option for those very charitably inclined who are still subject to the standard deduction and do not itemize on their tax return.

- Roth Conversions in 2020 can make more sense. With the probability of ordinary income tax rates increasing in the future, now might be the time to consider a Roth Conversion before year end. We have several clients that have taken advantage of this technique and can even combine the strategy with a Charitable Lead Trust (CLT) or other combinations of advanced tax strategies to put you into an improved situation going forward. Contact us ASAP if interested as time is running short.

- Active Tax Management is a value add that we regularly provide as part of our disciplined portfolio management process. This year in particular, moves we made throughout the year have been designed for asset allocation, security selection and active tax management purposes. Late this year, we may decide to trim some highly appreciated holdings that have grown beyond preferred levels and do so, ideally, with little tax cost impact because of active tax management actions we took earlier in the year.

- Proactive 2021 Tax Planning is here. We continue to invest in the best technologies and support to help us help you save taxes (in legally, ethically and morally fine ways). High on our list for upcoming Clarity Sessions is putting these tools and techniques to work for you better than ever. Stay tuned, “tax alpha” is an important KPI (Key Performance Indicator) to manage and we are pleased with our continuous investments and efforts to help clients in this way.

Janiczek Wealth Management – At a Glance

To learn more about Janiczek Wealth Management, click here.

Important Disclosures

The content herein is to be used for informational purposes only. Neither Janiczek Wealth Management or its owners and employees represent or warrant the accuracy or completeness of the information contained in this report. In no event will Janiczek Wealth Management or its owners or employees be liable for any damages that may result from the use of or reliance on these materials.

Past performance may not be indicative of future results. Different types of investments involve varying degrees of risk. Therefore, it should not be assumed that future performance of any specific investment or investment strategy (including the investments and/or investment strategies recommended and/or undertaken by Janiczek® Wealth Management (“Janiczek®”), or any non-investment related services, will be profitable, equal any historical performance level(s), be suitable for your portfolio or individual situation, or prove successful. Janiczek® is neither a law firm nor accounting firm, and no portion of its services should be construed as legal or accounting advice. Moreover, you should not assume that any discussion or information contained in this document serves as the receipt of, or as a substitute for, personalized investment advice from Janiczek®. Please remember that it remains your responsibility to advise Janiczek®, in writing, if there are any changes in your personal/financial situation or investment objectives for the purpose of reviewing/ evaluating/ revising our previous recommendations and/or services, or if you would like to impose, add, or to modify any reasonable restrictions to our investment advisory services. A copy of our current written disclosure Brochure discussing our advisory services and fees is available upon request. The scope of the services to be provided depends upon the needs of the client and the terms of the engagement.

TM & Copyright Janiczek Wealth Management. All rights reserved. Do not reproduce or redistribute in any form without prior written permission. Strength Based Wealth Management® 35 Essential Strengths®, The Stages of Financial Freedom®, Wealth Optimization Plan™, Wealth Optimization Dashboard™, Lifestyle Protection Analysis™, Elastic Limit Wealth Threshold™, Flourish! Activators™, FLOURISH!™ and Flourish! Based Retirement Planning™ are all trademarks of Wealth with Ease, LLC. For details, call 303-721-7000.