- Things That Matter

- Things You Can Control

- What You Should FOCUS On

![]()

Whether you need to tap them or not, its good to take inventory of the total amount of liquid cash reserve levels you have in place and how many months’ worth of current expenditures they represent. Review your checking, saving, money market, CD and Treasury Bill holdings and make a complete list of current balances, totaling them all up. What is the total current amount?

Now, Add up your current spending level across three categories:

- Non-discretionary Expenses (mortgage, rent, electric, utilities, groceries, etc.)

- Discretionary (entertainment, hobbies, clothing, etc.)

- Extraordinary (home projects, major repairs, major purchases, etc.)

Identify how many months of expenditures your cash reserve levels amount to. Then compare the amounts to this guideline:

- If your earned income is very consistent (including during this COVID-19 pandemic) and covers your expenses and more, your liquid reserves should amount to at least 3 months to 6 months of expenditures – plus any amounts for expected extraordinary expenditures over the next 18-months.

- If your earned income is sporadic (especially during this COVID-19 pandemic) and may not cover your entire expenses in a given month or quarter, your liquid reserves should amount to at least 6 to 12 months of expenditures – plus any amounts for expected extraordinary expenses over the next 18-months.

- If you are retired or unemployed (no earned income), your liquid reserves should amount to 12 months or more of expenditures – plus any amounts expected for extraordinary expenses over the next 18-months.

If you meet or exceed these standards, take note and consider these resources a good solid foundation of resources available to insulate you from distressed situations. If you don’t meet or exceed these standards, take note and consider your elevated clarity a newly acquired level of insight that will help you take action to increase your reserve level when you can. Whether you gained confidence or gained direction and motivation, either way you made progress.

Take note and move on to next steps for other considerations.

![]()

What’s the status of your earned income right now? List all sources and predictable amounts and calculate your coverage ratio (the percent of your current expenses your net income, after income taxes, covers your current monthly spend rate (100 means it’s just enough to cover all expenses (no deficit, no surplus), 200 means you meet all of your expenditures and save an equal amount, 50 means your earned income meets half of your expense level and the rest needs to come from other sources).

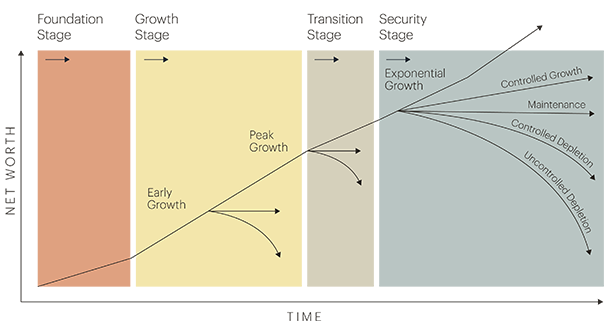

Answer these additional questions if you are employed or wanting to be employed (if you are not fully retired): What Stage of Financial Freedom are you in (see illustration)? Foundation? Early Growth? Peak Growth? Security Stage? How many years until you potentially want to transition into the Security Stage (reach the financial ability to stop your earned income and continue to maintain your desired stand of living?)? Are you maximizing your earned income now or under paid or employed? Note: Steps 11 and 12 can help increase/maximize your earned income, if interested.

Stages of Financial Freedom®

Answer these additional questions if fully retired: Have you elected to fully retire your earned income sources of cash flow? If you have voluntarily elected to retire this form of cash flow in the past, does staying fully retired remain your answer now?

No judgement here, it’s simply a question to take inventory of this earned income source of cash flow and your lifestyle decisions. From full to part time gigs, to never retiring, to having to or choosing to not have earned income, it is good to take note of your decision and circumstances including priorities and goals, lifestyle preferences, health constraints, personal decisions or family circumstances. Note: Steps 11 and 12 can be used to increase cash or non-cash compensation during your working years or retirement, if you are interested.

Take note of your amount, coverage ratio and ancillary answers and move on to next steps for other considerations.

![]()

Passive income sources are assets you own that produce an income that is not directly related to your working efforts. These are assets that are working for you such as investment real estate properties and businesses you own (portion related to your investment, not your labor). If you don’t have any such passive income assets, mark zero and move on.

Just like the above earned income exercise, identify the predictable amount you will receive from passive income sources and calculate your expense coverage ratio for this revenue source. If you don’t have passive income, your coverage ratio is zero. If you do have passive income, what percentage of your monthly expenses are covered by this amount?

Additional questions about your passive income sources: What is the condition of your passive investment assets? Are they well cared for and managed assets or are they stagnating or on the decline? Can you examine them carefully to perhaps cut out waste and increase their yield? Can you invest time and energy in them to increase their value? Is your investment in these assets producing appropriate risk/reward return or should you consider selling them and putting the proceeds to better use?

Additional questions if you don’t have passive income sources: Should you consider a passive income investment? Are you aware of passive investments that are an opportunity to create more wealth and income on your balance sheet and do you have the entrepreneurial zeal and DNA (see the book Entrepreneurial Leap by Gino Wickman) to lead, manage or invest in such ventures? Are their experts or people you know, who are great passive investors, who you can team up with to add this source of cash flow and asset to your balance sheet?

Take note of your amount, coverage ratio and answers to ancillary questions and move on to the next step.

![]()

Do you have pension benefits bringing in cash flow now? Deferred compensation income? Social security? Disability income benefits? Unemployment income benefits? Annuity income streams? Other sources like this that come in the form of periodic payments that are guaranteed by some stable entity? If so, add up and as described in the above earned income section, define your expense coverage ratio from these Benefits Income sources.

Question: Are there any benefit plans you can/should tap that you are not?

Take note of your amount and coverage ratio and move on.

![]()

We put this item in special related to the current crisis and special programs put in place by the government. Have you reviewed the Care Act and determined if you qualify for any special benefits? Read, study and investigate this program and any others that may come out and note the resource amount, timing and duration as a resource.

Question: Are there any special benefit programs to tap that apply to you or a business you own or manage?

![]()

Both your stocks and bonds may have a 2%, 3% or more dividend or coupon yield paying such income into your investment accounts, providing a source of cash that does not require you selling any holding. Regardless of whether you tap this dividend/interest yield, add it up and identify your expense coverage ratio for this source.

Questions: How does your dividend/interest yield compare to benchmark portfolios and/or best practice portfolios? Are you chasing yield and causing other potential portfolio problems? Are you too growth oriented and not including enough dividend payers? Great questions to ponder and utilize to optimize this cash flow source. We can help you examine your portfolio in numerous ways regarding your dividend yield.

Take note of your amount and dividend yield. Then move on to next sections.

![]()

After cash reserve levels, it can make sense to have a category of fixed income instruments that are highly liquid, have very modest interest rate and default risk and serve as an added source of liquidity if/when needed. Do you have investment holdings that fall into this category? Add them up and identify how many months’ worth of expenses they represent. It’s not uncommon, in our portfolios, for us to have an additional 3-months to 6-months of expenses worth of such holdings as an additional dry powder resource on hand.

Note your amount and how many months’ worth of expenses they represent and move on to next step.

![]()

Do you have a bond portfolio as a part of your mix of semi-liquid and/or retirement holdings? Which of these are A-Rated or higher (Government-backed, AAA, AA, A)? What percent of your portfolio is in this category? How many months of your expenses do these holdings represent? What is the maturity and duration level of this portfolio? Are these bonds managed in regard to ongoing credit-risk checks (for upgrades or downgrades, default rates, etc.)?

After your cash reserves and short-term/low duration bonds this is likely your next level of assets based upon quality/predictability. Get clear about these working assets with a proper diagnostic. This is an additional area where our investment team can examine your holdings and comment on strengths and weaknesses.

Take note of key observations regarding this portion of your assets and move on to the next section.

![]()

Wide-moat equity holdings are considered quality stocks in organizations built to last. With proper professional assistance, you can get clear about the proportion of your portfolio assets that fall into a very solid group that has staying power, earning power, brand appeal, talent, market share, balance sheets, financing options, disruption-resistant entry barriers and good innovative management to continue to stay relevant and valuable. Owning such gems is a form of balance sheet diversification that could be more stable and could offer more upside value in terms of the predictability of future income streams.

What amount and portion of your investment portfolio falls into the wide moat category? Take note and move on.

![]()

Compile your complete balance sheet of all types of assets (including above) and all types of liabilities. Utilize our unique balance sheet organizer to calculate your:

- Net Liquid Assets (Liquid reserves less Credit Card Debt)

- Net Semi-Liquid Assets (Semi-liquid investment assets less short-term loans)

- Net Retirement Assets (Retirement account assets less loans from such accounts)

- Net Personal Assets (Personal Assets (like your home(s) less mortgages/loans on such assets)

- Net Non-liquid Assets (Investment Properties, Businesses, etc. less any liabilities associated with them, including tax reserves for unrealized capital gains)

Get professional input as well. Balance sheet mistakes are the root of many larger problems. We have a variety of balance sheet tests and ratio standards we use in our process to optimize balance sheets. Contact us to gain this insight and value via our wealth management services. Balance sheet pruning routines are an essential element of ongoing wealth mastery.

![]()

Now that you have a wonderful inventory of the resources at your disposal, take a fresh look at it all and ask yourself which of these resources you can take from a lower level of productivity to a higher level of productivity?

Frankly, this is where we could come in to also assess and offer our input on your opportunities to better manage and optimize all aspects of your balance sheet, cash flow, portfolio and financial well-being. Consider a professional second-opinion review to help you identify opportunities you may not see.

Additional opportunities: If you are employed or own a business, we have exercises beyond the scope of this exercise that are designed to help you identify the opportunity to take resources from lower levels of productivity to higher levels of productivity in such circumstances. In fact, if you serve an employer/boss or a customer, it is healthy to ask that same question: how can you help them move from a lower level of productivity to a higher level of productivity? Adding such value is what creates wealth creation and income opportunities in the first place.

Here in Step #11 is where you can begin to consolidate all of your insights, observations and ideas from the first ten steps into a prioritized list of actions ordered by likely impact increasing your confidence and results. This is both an art and science that we typically do for our clients (we serve high and ultra-high net worth delegators). However, if you are seeking to do this on your own at this time, create your list and prioritize it by what increases your confidence, results and well-being the most.

With your summarized list in hand, move on to Step # 12, which is icing on the cake.

![]()

Here’s a preview of a powerful technique featured in our founder’s new to be released book (2021), Flourish! How to Prosper with the Greatest Ease.

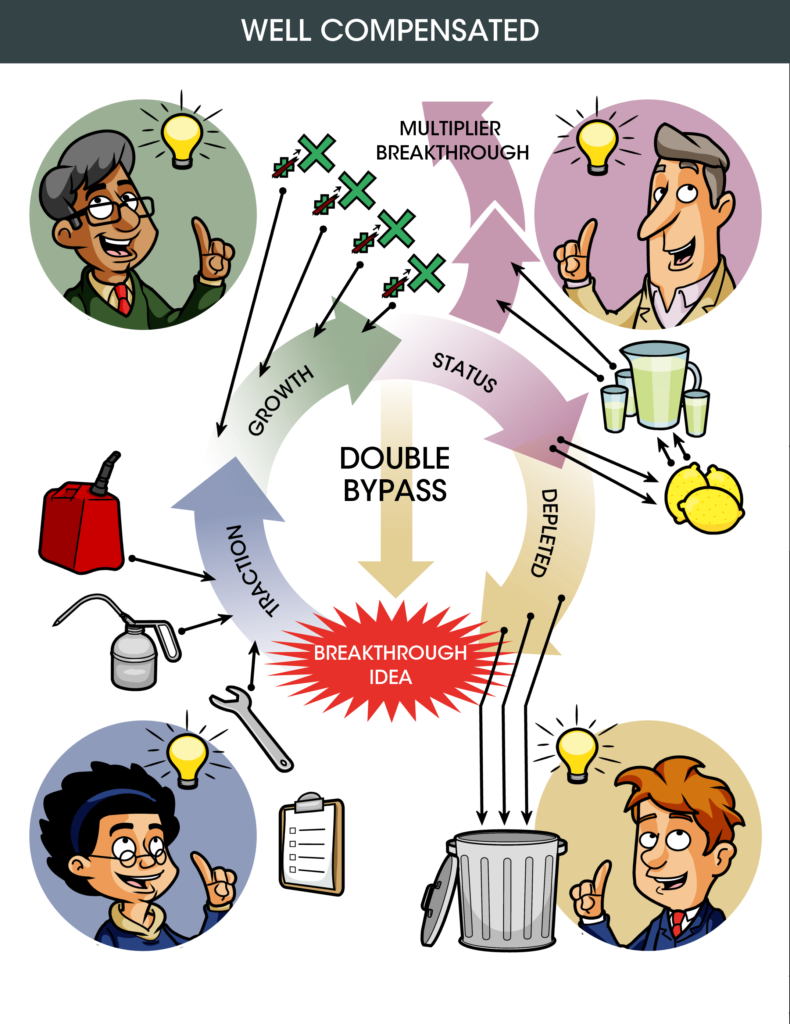

Economist Joseph Schumpeter (1883 – 1950) coined the term “creative destruction” to explain the free market’s rather messy way of bringing in innovative new products and services and phasing out old products and services with less desirable features and benefits.

To understand creative destruction, consider the Creative Destruction Lifecycle illustration below. It shows how all industries and organizations go through a cycle that begins with the Traction Stage (when a product or service is seeking to gain traction as an innovative new offering), then the Growth Stage (when the idea takes off and multiplies), then the Status Stage (when it matures, gets bogged down by status, bureaucracy, and regulation), and finally the Depleted Stage (when a product or organization is lacking so much that it can no longer sustain itself in its present form.

Copyright 2020 Joseph J. Janiczek. All rights reserved. Used with permission from to be released book: Flourish! How to Prosper with the Greatest Ease. Call 303-721-7000 for details.

To begin, take inventory at this unique time with any and all disruptions that the COVID-19 pandemic has placed on your career, your role, your employer/business, your industry, and become super aware of what is bogged down in the Status Stage, what is really on its way out in the Depleted Stage, what new breakthrough ideas to operate differently are emerging in the Traction Stage and what can be multiplied in the Growth Stage. As the illustration depicts, rather than fight these forces, utilize their power to innovate, such as:

- Taking inventory of promising innovations and developments in the Traction Stage and helping them succeed.

- Identifying what already has traction and can be duplicated over and over in the Growth Stage. Put yourself in the position to multiply the results achieved by these winners.

- Take inventory of the relatively worn out and/or outdated aspects of your organization that are in the Status Stage. Here, you can focus on how you can transform them into bright, fresh strengths that get on a new growth curve.

- Finally, take note of what is truly in the Depleted Stage. How can you cleanse yourself and your organization of this distracting thorn so you and others can focus time, attention, and resources on the fruitful initiatives in the other stages?

Your aim is to position yourself where your talents, abilities and interests can best help the organization navigate the Creative Destruction Lifecyle. Doing so maximizes your contribution. Maximize your contribution and, with smart actions we can help you with on the wealth creation side of things, your compensation can be maximized as well. Cash flow confidence is at its peak when you can add so much value that your abilities are in high demand in the right places, naturally attracting maximum reward.

Take note of insights and opportunities to increase your contributions and your compensation. One of the very reasons you want to have proper cash flow reserves and cash flow diversity is to be able to focus more time on such value and wealth creation techniques.

Take note of the Traction Stage, Growth Stage, Status Stage and Depletion Stage projects you (or others) can be a champion of and write them down. Which of these are you most interested and fascinated in pursuing? Which will be most well received by those around you? Which is best timed for you (or others) to address in the next 90-days? Who is the best team/family member (or service provider) to champion the project? What’s the best result you are after for the project? What’s the deadline?

Now, move on to the conclusion of this process where you consider and filter all of your ideas from each step down to the three that are most important to tackle first.